S-ar putea să vă placă și

- Robo Advisory 2Document8 paginiRobo Advisory 2Ankur Pandey0% (1)

- FUNDSYS Robo-Advice Case StudyDocument2 paginiFUNDSYS Robo-Advice Case StudyAnneka Sophia de LeonÎncă nu există evaluări

- CB Insights - Fintech Report Q1 2021Document80 paginiCB Insights - Fintech Report Q1 2021rahulÎncă nu există evaluări

- Robo AdvisorsDocument77 paginiRobo AdvisorsSofia GaganiÎncă nu există evaluări

- Is Robo-Advisory Revolutionising The Investment LandscapeDocument17 paginiIs Robo-Advisory Revolutionising The Investment LandscapeKnow IT-Whats happening MARKETÎncă nu există evaluări

- Robo-Advisors: Exploring and Leveraging The Competition: February 2020Document18 paginiRobo-Advisors: Exploring and Leveraging The Competition: February 2020AkashzPhoenixÎncă nu există evaluări

- Robo Advisors Investing Through MachinesDocument4 paginiRobo Advisors Investing Through MachinesKnow IT-Whats happening MARKETÎncă nu există evaluări

- March of The Robo-AdvisorsDocument37 paginiMarch of The Robo-AdvisorsAnkur PandeyÎncă nu există evaluări

- Top-10 Trends in Wealth Management: 2019: What You Need To KnowDocument27 paginiTop-10 Trends in Wealth Management: 2019: What You Need To KnowanjuÎncă nu există evaluări

- Introduction To Artificial Intelligence 2021 NSDocument43 paginiIntroduction To Artificial Intelligence 2021 NSFitriana Zahirah TÎncă nu există evaluări

- Robo Advisory FintecDocument12 paginiRobo Advisory FintecUtkarsh SharmaÎncă nu există evaluări

- 100 Marketing ANSWERsDocument35 pagini100 Marketing ANSWERsAshu SinghÎncă nu există evaluări

- Robo AdvisorsDocument13 paginiRobo AdvisorsSRISHTI NARANGÎncă nu există evaluări

- Case Study: Defense Electronics, Inc.Document7 paginiCase Study: Defense Electronics, Inc.Farida100% (1)

- New Supplier Code of EthicDocument13 paginiNew Supplier Code of EthicFrankie NguyenÎncă nu există evaluări

- Business Analysis in The Blockchain Age PDFDocument19 paginiBusiness Analysis in The Blockchain Age PDFprogisÎncă nu există evaluări

- Efficient MKT HypothesisDocument20 paginiEfficient MKT HypothesisSamrat MazumderÎncă nu există evaluări

- S 12 - Robo - AdvisingDocument24 paginiS 12 - Robo - AdvisingAninda DuttaÎncă nu există evaluări

- I Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and EarnedDocument8 paginiI Used Acorns, Robinhood, and Stash For 2 Years. This Is What I Learned and Earnedbarakasake300Încă nu există evaluări

- Accenture CFO Research Global PDFDocument47 paginiAccenture CFO Research Global PDFDeepak SharmaÎncă nu există evaluări

- Ebook: Financial Advice With Robo Advisors (English)Document25 paginiEbook: Financial Advice With Robo Advisors (English)BBVA Innovation CenterÎncă nu există evaluări

- Investment Banking, Equity Research, Valuation Interview Handpicked Questions and AnswerDocument17 paginiInvestment Banking, Equity Research, Valuation Interview Handpicked Questions and AnswerStudy FreakÎncă nu există evaluări

- Corporate Professionals Sum of Parts ValuationDocument4 paginiCorporate Professionals Sum of Parts ValuationCorporate Professionals100% (1)

- Case Study BDODocument2 paginiCase Study BDOSaumya GoelÎncă nu există evaluări

- Boston University Student Research: Zipcar, IncDocument28 paginiBoston University Student Research: Zipcar, Incforeverjessx3Încă nu există evaluări

- (ICBD) : Introducing Integrated Component Based Development Lifecycle and ModelDocument13 pagini(ICBD) : Introducing Integrated Component Based Development Lifecycle and ModelijseaÎncă nu există evaluări

- Fintech in Asean 2021Document49 paginiFintech in Asean 2021dl1983Încă nu există evaluări

- EBIT vs. EBITDA vs. Net Income Valuation Metrics and MultiplesDocument3 paginiEBIT vs. EBITDA vs. Net Income Valuation Metrics and MultiplesSanjay Rathi100% (1)

- Return On EquityDocument7 paginiReturn On EquityTumwine Kahweza ProsperÎncă nu există evaluări

- WEF New Physics of Financial ServicesDocument167 paginiWEF New Physics of Financial ServicesKaren L YoungÎncă nu există evaluări

- Artificial Intelligence Applied To Stock Market Trading A ReviewDocument20 paginiArtificial Intelligence Applied To Stock Market Trading A ReviewAbdellatif Soklabi100% (1)

- Week Beginning Sunday January 1, 2012: Sunday Monday Tuesday Wednesday Thursday Friday SaturdayDocument2 paginiWeek Beginning Sunday January 1, 2012: Sunday Monday Tuesday Wednesday Thursday Friday SaturdayJack JacintoÎncă nu există evaluări

- Arbitrage ProjectDocument96 paginiArbitrage Projectyogesh_bhargavÎncă nu există evaluări

- Wealth FrontDocument4 paginiWealth FrontSiddharth JastiÎncă nu există evaluări

- Valeant Pharmaceuticals JPM Presentation 01-10-2017Document26 paginiValeant Pharmaceuticals JPM Presentation 01-10-2017medtechyÎncă nu există evaluări

- World Fintech Report 2017Document48 paginiWorld Fintech Report 2017morellimarc100% (2)

- Loan PredictionDocument37 paginiLoan PredictionManashi DebbarmaÎncă nu există evaluări

- Efficient Market Hypothesis SlidesDocument41 paginiEfficient Market Hypothesis SlidesDeep Shikhar100% (1)

- Future Trends in Insurance - Trevor RorbyeDocument23 paginiFuture Trends in Insurance - Trevor Rorbyekwtam338Încă nu există evaluări

- Case Study 3 - Pleasure CraftDocument8 paginiCase Study 3 - Pleasure Craftspectrum_480% (1)

- Nuveen - A Good Time For Private DebtDocument3 paginiNuveen - A Good Time For Private Debtramachandra rao sambangiÎncă nu există evaluări

- Banking On Data Analytics? Think FastDocument10 paginiBanking On Data Analytics? Think Fastmazofeifa@jacks.co.crÎncă nu există evaluări

- 2009 Deutsche Bank Alternative Investment SurveyDocument90 pagini2009 Deutsche Bank Alternative Investment SurveyDealBook100% (20)

- Ow To Build A Robo Advisor: Ebook For Wealth ManagersDocument15 paginiOw To Build A Robo Advisor: Ebook For Wealth ManagersAkashzPhoenixÎncă nu există evaluări

- Pitching For Venture CapitalDocument25 paginiPitching For Venture Capitalecell_iimkÎncă nu există evaluări

- Catalytic First Loss CapitalDocument36 paginiCatalytic First Loss Capitalblanche21100% (1)

- Capco - Partnering With Robo Advisors - BlogDocument3 paginiCapco - Partnering With Robo Advisors - BlogAkashzPhoenixÎncă nu există evaluări

- Weather Derivatives in IndiaDocument25 paginiWeather Derivatives in Indiaprateek0512Încă nu există evaluări

- Portfolio Management With Heuristic Optimization MaringerDocument237 paginiPortfolio Management With Heuristic Optimization MaringerArushSinghÎncă nu există evaluări

- Financial AnalysisDocument15 paginiFinancial AnalysisSitiNorhafizahDollah100% (1)

- ESG Rating Disagreement and Stock ReturnsDocument55 paginiESG Rating Disagreement and Stock ReturnsFlorian Cornelis100% (1)

- Planet Fitness: No Judgements, No Lunks: Michael A. RobertoDocument24 paginiPlanet Fitness: No Judgements, No Lunks: Michael A. RobertoDaniel DarwicheÎncă nu există evaluări

- Factors Affecting Investment Decisions Studies On Young InvestorsDocument7 paginiFactors Affecting Investment Decisions Studies On Young InvestorslaluaÎncă nu există evaluări

- Survey of Investors in Hedge Funds 2010Document6 paginiSurvey of Investors in Hedge Funds 2010http://besthedgefund.blogspot.comÎncă nu există evaluări

- Innovations in Digital Finance 2014Document24 paginiInnovations in Digital Finance 2014sangya01Încă nu există evaluări

- Orange County Case ReportDocument8 paginiOrange County Case ReportOguz AslayÎncă nu există evaluări

- CHAPTER 1 - Introduction To InvestmentDocument41 paginiCHAPTER 1 - Introduction To InvestmentSuct WadiÎncă nu există evaluări

- Dupont Analysis ApplicationDocument21 paginiDupont Analysis ApplicationGauravÎncă nu există evaluări

- Chapter 7 Source of Finance PDFDocument30 paginiChapter 7 Source of Finance PDFtharinduÎncă nu există evaluări

- Beta Anomaly An Ex-Ante Tail RiskDocument104 paginiBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Claudia Jones Nuclear TestingDocument25 paginiClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Why The Euro Will Rival The Dollar PDFDocument25 paginiWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Conference Group For Central European History of The American Historical AssociationDocument9 paginiConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Theophilus Capital Against: Fisk Labor1Document9 paginiTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

- Karl Kautsky Republic and Social Democra PDFDocument4 paginiKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Continuity Change State of Process of Task ofDocument1 paginăContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Borel Sets PDFDocument181 paginiBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- 1st International: Djacobs November 2020Document5 pagini1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsÎncă nu există evaluări

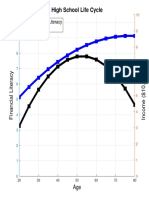

- High School Life Cycle: Financial Literacy IncomeDocument1 paginăHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Gpebook PDFDocument332 paginiGpebook PDFDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Cover FERCDocument1 paginăCover FERCDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Simple BeamerDocument25 paginiSimple BeamerDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Necessary and Sufficient Conditions For Dynamic OptimizationDocument18 paginiNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDocument8 paginiThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Teach-In: Government of The People, by The People, For The PeopleDocument24 paginiTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Bank Loan Loss ProvisioningDocument17 paginiBank Loan Loss ProvisioningDaniel Lee Eisenberg JacobsÎncă nu există evaluări

- Digital Marketing Class NotesDocument58 paginiDigital Marketing Class Notestina tanwarÎncă nu există evaluări

- Inspection and Test Plan-Geo-Technical Works C002Document3 paginiInspection and Test Plan-Geo-Technical Works C002Furqan0% (1)

- A Study On Digital Payments System & Consumer Perception: An Empirical SurveyDocument11 paginiA Study On Digital Payments System & Consumer Perception: An Empirical SurveyDeepa VishwakarmaÎncă nu există evaluări

- List of Government AgenciesDocument55 paginiList of Government AgenciesOzilac JhsÎncă nu există evaluări

- ACC201 Financial AccountingDocument47 paginiACC201 Financial AccountingG JhaÎncă nu există evaluări

- Marks of A Successful EntrepreneurDocument4 paginiMarks of A Successful Entrepreneuremilio fer villaÎncă nu există evaluări

- Little Leaf's Microgreens Price Calculator 2021Document26 paginiLittle Leaf's Microgreens Price Calculator 2021Carl RodríguezÎncă nu există evaluări

- SITXFIN003 - Student Assessment Tool Manage Finaces Within A BudgettDocument37 paginiSITXFIN003 - Student Assessment Tool Manage Finaces Within A BudgettTina100% (2)

- Report On DAReWRODocument18 paginiReport On DAReWROSaeed Agha AhmadzaiÎncă nu există evaluări

- BMN 506 - Week 2Document87 paginiBMN 506 - Week 2Shubham SrivastavaÎncă nu există evaluări

- Apeejay Institute of Management Technical Campus Rama-Mandi, Hoshiarpur Road, JalandharDocument3 paginiApeejay Institute of Management Technical Campus Rama-Mandi, Hoshiarpur Road, JalandharSahil DewanÎncă nu există evaluări

- Forex Systems: Types of Forex Trading SystemDocument35 paginiForex Systems: Types of Forex Trading SystemalypatyÎncă nu există evaluări

- Chapter 12-Bond MarketDocument48 paginiChapter 12-Bond MarketIzat MrfÎncă nu există evaluări

- Loadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Document3 paginiLoadmasters Customs Services, Inc. v. Glodel Brokerage Corporation, G.R. No. 179446, 10 January 2011, (639 SCRA 69)Christian Talisay100% (1)

- MICE Midterm ReviewerDocument15 paginiMICE Midterm Reviewergrace.gonzagaÎncă nu există evaluări

- RPW Main Report and Annex q222Document2 paginiRPW Main Report and Annex q222GalungÎncă nu există evaluări

- Blood Orange Sell SheetDocument4 paginiBlood Orange Sell SheetSunkist GrowersÎncă nu există evaluări

- UntitledDocument10 paginiUntitledmehvishÎncă nu există evaluări

- 16Document1 pagină16Babu babuÎncă nu există evaluări

- GuessDocument20 paginiGuessRohit SainiÎncă nu există evaluări

- Marketing Mix Unit QuestionsDocument4 paginiMarketing Mix Unit QuestionsAnitaÎncă nu există evaluări

- Introduction To Hospitality 6th Edition Walker Test BankDocument6 paginiIntroduction To Hospitality 6th Edition Walker Test Bankcherylsmithckgfqpoiyt100% (18)

- Management and Cost Accounting 6Th Edition Full ChapterDocument41 paginiManagement and Cost Accounting 6Th Edition Full Chapterjohn.thier767100% (21)

- List of Table and Figures: Outline Development Plan, AgraDocument12 paginiList of Table and Figures: Outline Development Plan, AgrageetÎncă nu există evaluări

- PD MitraDocument42 paginiPD Mitraelza jiuniÎncă nu există evaluări

- 12e.MCQs.C1 For StsDocument12 pagini12e.MCQs.C1 For StsTrang HoàngÎncă nu există evaluări

- Lim Tong Lim v. Phil Fishing Gear IndustriesDocument7 paginiLim Tong Lim v. Phil Fishing Gear IndustriesEzra Dan BelarminoÎncă nu există evaluări

- Session 13 - NPDIDocument8 paginiSession 13 - NPDIPRALHAD DASÎncă nu există evaluări

- The Innovation of Grocery StoreDocument5 paginiThe Innovation of Grocery StoreNguyễn Hồng VũÎncă nu există evaluări

- Foundations of Operations Management - WK3 - Process Selection and InfluencesDocument3 paginiFoundations of Operations Management - WK3 - Process Selection and InfluencesSushobhanÎncă nu există evaluări

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)

- John D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthDe la EverandJohn D. Rockefeller on Making Money: Advice and Words of Wisdom on Building and Sharing WealthEvaluare: 4 din 5 stele4/5 (20)

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDe la EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisEvaluare: 5 din 5 stele5/5 (6)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDe la Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNEvaluare: 4.5 din 5 stele4.5/5 (3)

- Ready, Set, Growth hack:: A beginners guide to growth hacking successDe la EverandReady, Set, Growth hack:: A beginners guide to growth hacking successEvaluare: 4.5 din 5 stele4.5/5 (93)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 3.5 din 5 stele3.5/5 (8)

- The 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamDe la EverandThe 17 Indisputable Laws of Teamwork Workbook: Embrace Them and Empower Your TeamÎncă nu există evaluări

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDe la EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingEvaluare: 4.5 din 5 stele4.5/5 (17)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialEvaluare: 4.5 din 5 stele4.5/5 (32)

- Value: The Four Cornerstones of Corporate FinanceDe la EverandValue: The Four Cornerstones of Corporate FinanceEvaluare: 4.5 din 5 stele4.5/5 (18)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDe la EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursEvaluare: 4.5 din 5 stele4.5/5 (8)

- Creating Shareholder Value: A Guide For Managers And InvestorsDe la EverandCreating Shareholder Value: A Guide For Managers And InvestorsEvaluare: 4.5 din 5 stele4.5/5 (8)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- The Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsDe la EverandThe Merger & Acquisition Leader's Playbook: A Practical Guide to Integrating Organizations, Executing Strategy, and Driving New Growth after M&A or Private Equity DealsÎncă nu există evaluări

- Built, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursDe la EverandBuilt, Not Born: A Self-Made Billionaire's No-Nonsense Guide for EntrepreneursEvaluare: 5 din 5 stele5/5 (13)

- Private Equity and Venture Capital in Europe: Markets, Techniques, and DealsDe la EverandPrivate Equity and Venture Capital in Europe: Markets, Techniques, and DealsEvaluare: 5 din 5 stele5/5 (1)

- Mind over Money: The Psychology of Money and How to Use It BetterDe la EverandMind over Money: The Psychology of Money and How to Use It BetterEvaluare: 4 din 5 stele4/5 (24)

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorDe la EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorÎncă nu există evaluări

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- Product-Led Growth: How to Build a Product That Sells ItselfDe la EverandProduct-Led Growth: How to Build a Product That Sells ItselfEvaluare: 5 din 5 stele5/5 (1)

- Valley Girls: Lessons From Female Founders in the Silicon Valley and BeyondDe la EverandValley Girls: Lessons From Female Founders in the Silicon Valley and BeyondÎncă nu există evaluări

- The Value of a Whale: On the Illusions of Green CapitalismDe la EverandThe Value of a Whale: On the Illusions of Green CapitalismEvaluare: 5 din 5 stele5/5 (2)

- Finance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)De la EverandFinance Secrets of Billion-Dollar Entrepreneurs: Venture Finance Without Venture Capital (Capital Productivity, Business Start Up, Entrepreneurship, Financial Accounting)Evaluare: 4 din 5 stele4/5 (5)