S-ar putea să vă placă și

- Actuarial Finance: Derivatives, Quantitative Models and Risk ManagementDe la EverandActuarial Finance: Derivatives, Quantitative Models and Risk ManagementÎncă nu există evaluări

- Series 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)De la EverandSeries 65 Exam Practice Question Workbook: 700+ Comprehensive Practice Questions (2023 Edition)Încă nu există evaluări

- PP Invt&sec 2018Document5 paginiPP Invt&sec 2018Revatee HurilÎncă nu există evaluări

- ICAI - Question BankDocument6 paginiICAI - Question Bankkunal mittalÎncă nu există evaluări

- FOI Assignment 2023Document3 paginiFOI Assignment 2023Rohan MauryaÎncă nu există evaluări

- Investment PapersDocument6 paginiInvestment PapersAbhishek JainÎncă nu există evaluări

- CFI5104201205 Investment AnalysisDocument7 paginiCFI5104201205 Investment AnalysisNelson MrewaÎncă nu există evaluări

- BF PP 2017Document4 paginiBF PP 2017Revatee HurilÎncă nu există evaluări

- Fe2305-0573 20230903121830Document9 paginiFe2305-0573 20230903121830broken swordÎncă nu există evaluări

- Fe 202009 BBCF1013Document8 paginiFe 202009 BBCF1013Wan Muhamad ShariffÎncă nu există evaluări

- Investment Planning and Portfolio ManagementDocument3 paginiInvestment Planning and Portfolio ManagementTark Raj BhattÎncă nu există evaluări

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument21 paginiPaper - 2: Strategic Financial Management Questions Security Valuationsam kapoorÎncă nu există evaluări

- TutorialsDocument28 paginiTutorialsmupiwamasimbaÎncă nu există evaluări

- Sep23 Ques-1Document5 paginiSep23 Ques-1absankey770Încă nu există evaluări

- BSF 1102 - Principles of Finance - November 2022Document6 paginiBSF 1102 - Principles of Finance - November 2022JulianÎncă nu există evaluări

- CA Final SFM RTP For May 2023Document18 paginiCA Final SFM RTP For May 2023remoratilemothekheÎncă nu există evaluări

- Portfolio Management Handout 1 - Questions PDFDocument6 paginiPortfolio Management Handout 1 - Questions PDFPriyankaÎncă nu există evaluări

- TEST Paper 1 Full TestDocument9 paginiTEST Paper 1 Full Testjohny SahaÎncă nu există evaluări

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument21 paginiPaper - 2: Strategic Financial Management Questions Security ValuationRITZ BROWNÎncă nu există evaluări

- Strategic Financial Management PDFDocument18 paginiStrategic Financial Management PDFUpkar SinghÎncă nu există evaluări

- Financial Management: Acca Revision Mock 3Document13 paginiFinancial Management: Acca Revision Mock 3krishna gopalÎncă nu există evaluări

- FFTFMDocument5 paginiFFTFMKaran NewatiaÎncă nu există evaluări

- BF PP 2016Document5 paginiBF PP 2016Revatee HurilÎncă nu există evaluări

- Acf1002 1 2006 2Document6 paginiAcf1002 1 2006 2sandhyamohunÎncă nu există evaluări

- Financial Management Assignment (2009)Document5 paginiFinancial Management Assignment (2009)sleshiÎncă nu există evaluări

- Ca Final SFM Test Paper QuestionDocument8 paginiCa Final SFM Test Paper Question1620tanyaÎncă nu există evaluări

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument25 paginiPaper - 2: Strategic Financial Management Questions Security ValuationPalisthaÎncă nu există evaluări

- PT Questions (S2021) Class ExercisesDocument19 paginiPT Questions (S2021) Class ExercisesNavhin MichealÎncă nu există evaluări

- CM2ADocument5 paginiCM2AMike KanyataÎncă nu există evaluări

- Lcture 3 and 4 Risk and ReturnDocument8 paginiLcture 3 and 4 Risk and ReturnNimra Farooq ArtaniÎncă nu există evaluări

- MN5207 Acounting and Financial Management 2019Document10 paginiMN5207 Acounting and Financial Management 2019Vimuth Chanaka PereraÎncă nu există evaluări

- FNCE 10002 Sample FINAL EXAM 2 For Students - Sem 2 2019 PDFDocument3 paginiFNCE 10002 Sample FINAL EXAM 2 For Students - Sem 2 2019 PDFC A.Încă nu există evaluări

- Investment Analysis 1Document6 paginiInvestment Analysis 1Zorodzai MuteroÎncă nu există evaluări

- Actuarial Society of India: ExaminationsDocument5 paginiActuarial Society of India: ExaminationsdasÎncă nu există evaluări

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 paginiQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerAyushi GuptaÎncă nu există evaluări

- Financial Management - Practice WorkbookDocument39 paginiFinancial Management - Practice WorkbookFAIQ KHALIDÎncă nu există evaluări

- Lcture 3 and 4 Risk and ReturnDocument4 paginiLcture 3 and 4 Risk and ReturnSyeda Umaima0% (1)

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument120 paginiPaper - 2: Strategic Financial Management Questions Security ValuationKeshav SethiÎncă nu există evaluări

- Paper - 2: Strategic Financial Management Questions Security ValuationDocument21 paginiPaper - 2: Strategic Financial Management Questions Security ValuationItikaa TiwariÎncă nu există evaluări

- CF Paper Summer 2015Document4 paginiCF Paper Summer 2015Vicky ThakkarÎncă nu există evaluări

- Portfolio TheoryDocument9 paginiPortfolio TheorytoabhishekpalÎncă nu există evaluări

- B7AF100 - 2021 - OMD1 - First Sitting Exam PaperDocument12 paginiB7AF100 - 2021 - OMD1 - First Sitting Exam PaperAZLEA BINTI SYED HUSSIN (BG)Încă nu există evaluări

- f9 2018 Marjun QDocument6 paginif9 2018 Marjun QDilawar HayatÎncă nu există evaluări

- The Figures in The Margin On The Right Side Indicate Full Marks. Please Answer All Bits of A Question at One PlaceDocument7 paginiThe Figures in The Margin On The Right Side Indicate Full Marks. Please Answer All Bits of A Question at One Placemknatoo1963Încă nu există evaluări

- FM QPDocument18 paginiFM QPjpkassociates2019Încă nu există evaluări

- CH 4 - Portfolio Management (2024) - HandoutDocument21 paginiCH 4 - Portfolio Management (2024) - HandoutMayibongwe MpofuÎncă nu există evaluări

- Mba 108 CDocument5 paginiMba 108 CRohit TushirÎncă nu există evaluări

- AFIN209 2018 Semester 1 Final Exam PDFDocument6 paginiAFIN209 2018 Semester 1 Final Exam PDFGeorge MandaÎncă nu există evaluări

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 paginiQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerItikaa TiwariÎncă nu există evaluări

- Question No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswerDocument5 paginiQuestion No. 1 Is Compulsory. Attempt Any Four Questions From The Remaining Five Questions. Working Notes Should Form Part of The AnswercdÎncă nu există evaluări

- B1 Free Solving Nov 2019) - Set 4Document11 paginiB1 Free Solving Nov 2019) - Set 4paul sagudaÎncă nu există evaluări

- BSF 1102 - Principles of Finance - December 2022Document4 paginiBSF 1102 - Principles of Finance - December 2022JulianÎncă nu există evaluări

- BFI 220 Cat II - Due On 13th Nov 2023Document2 paginiBFI 220 Cat II - Due On 13th Nov 2023mahmoudfatahabukarÎncă nu există evaluări

- If (Final) A08Document6 paginiIf (Final) A08ksybÎncă nu există evaluări

- COM 96th AIBB Solved-FBDocument29 paginiCOM 96th AIBB Solved-FBShamima AkterÎncă nu există evaluări

- IPMDocument6 paginiIPMPOOJAN DANIDHARIYAÎncă nu există evaluări

- Principles of Financial Management Practice QsDocument4 paginiPrinciples of Financial Management Practice Qs22UG1-0372 WICKRAMAARACHCHI W.A.S.M.Încă nu există evaluări

- SFM Q MTP 1 Final May22Document5 paginiSFM Q MTP 1 Final May22Divya AggarwalÎncă nu există evaluări

- Private Debt: Yield, Safety and the Emergence of Alternative LendingDe la EverandPrivate Debt: Yield, Safety and the Emergence of Alternative LendingÎncă nu există evaluări

- Chapter 1 ExosDocument5 paginiChapter 1 ExosRevatee HurilÎncă nu există evaluări

- Unemployment V/s InflationDocument3 paginiUnemployment V/s InflationRevatee HurilÎncă nu există evaluări

- Tutorial Questions Week 7Document4 paginiTutorial Questions Week 7Revatee HurilÎncă nu există evaluări

- Year FDI Net Inflows Stock Market Development As A % of GDP Stocks Traded, Total Value (% of GDP)Document1 paginăYear FDI Net Inflows Stock Market Development As A % of GDP Stocks Traded, Total Value (% of GDP)Revatee HurilÎncă nu există evaluări

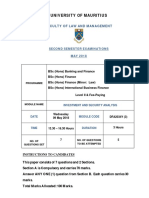

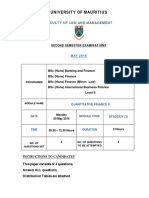

- University of Mauritius: Faculty of Law and ManagementDocument3 paginiUniversity of Mauritius: Faculty of Law and ManagementRevatee HurilÎncă nu există evaluări

- Annex 2 University of Mauritius Module Specification Sheet: 1. General InformationDocument6 paginiAnnex 2 University of Mauritius Module Specification Sheet: 1. General InformationRevatee HurilÎncă nu există evaluări

- BF PP 2017Document4 paginiBF PP 2017Revatee HurilÎncă nu există evaluări

- QF 2 PP 2017Document8 paginiQF 2 PP 2017Revatee HurilÎncă nu există evaluări

- BF PP 2016Document5 paginiBF PP 2016Revatee HurilÎncă nu există evaluări

- QF 2 PP 2016Document4 paginiQF 2 PP 2016Revatee HurilÎncă nu există evaluări

- BF PP 2012Document6 paginiBF PP 2012Revatee HurilÎncă nu există evaluări

- QF 2 PP 2015Document9 paginiQF 2 PP 2015Revatee HurilÎncă nu există evaluări

- Class Day Test BSC Finance Year 2Document5 paginiClass Day Test BSC Finance Year 2Revatee HurilÎncă nu există evaluări

- IS and LMDocument18 paginiIS and LMM Samee ArifÎncă nu există evaluări

- CapitaLand Limited SGX C31 Financials Income StatementDocument3 paginiCapitaLand Limited SGX C31 Financials Income StatementElvin TanÎncă nu există evaluări

- IFRS 9 and ECL Modeling Free ClassDocument43 paginiIFRS 9 and ECL Modeling Free ClassAbdallah Abdul JalilÎncă nu există evaluări

- International Banking & Foreign Exchange ManagementDocument12 paginiInternational Banking & Foreign Exchange ManagementrumiÎncă nu există evaluări

- Multinational Business Finance 14th Edition Eiteman Test BankDocument36 paginiMultinational Business Finance 14th Edition Eiteman Test Bankrecolletfirework.i9oe100% (23)

- Financial Analysis of - Toys "R" Us, Inc.Document30 paginiFinancial Analysis of - Toys "R" Us, Inc.Arabi AsadÎncă nu există evaluări

- Application Form - CashVantage (Version2 2 - Dec 2014) - V7Document5 paginiApplication Form - CashVantage (Version2 2 - Dec 2014) - V7Mfairuz HassanÎncă nu există evaluări

- CH 9Document82 paginiCH 9Michael Fine100% (2)

- What Is Go Smart Digi and How Useful For Yo1 PDFDocument2 paginiWhat Is Go Smart Digi and How Useful For Yo1 PDFVirendra KumarÎncă nu există evaluări

- FULL Download Ebook PDF International Finance 5th Edition Fifth Edition PDF EbookDocument41 paginiFULL Download Ebook PDF International Finance 5th Edition Fifth Edition PDF Ebooksally.marcum863100% (38)

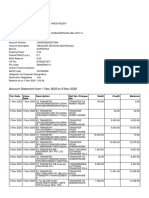

- Account Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 paginiAccount Statement From 1 Nov 2020 To 9 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancevinod reddyÎncă nu există evaluări

- Swabhimaan - Transforming Rural India Through Financial InclusionDocument2 paginiSwabhimaan - Transforming Rural India Through Financial Inclusionjohnyy2kÎncă nu există evaluări

- FRM Juice Notes 2019Document202 paginiFRM Juice Notes 2019Dipesh Memani100% (8)

- Tender Documnet ICTDocument54 paginiTender Documnet ICTMusharaf Habib100% (1)

- Annuities - A Series of Equal Payments Occurring at Equal Periods of TimeDocument5 paginiAnnuities - A Series of Equal Payments Occurring at Equal Periods of TimeMarcial MilitanteÎncă nu există evaluări

- Application Form For Agriculture Credit Rs.2lto10lDocument12 paginiApplication Form For Agriculture Credit Rs.2lto10lAnitakurmaÎncă nu există evaluări

- ACFI1003 - Lecture 7 Corporations and The Share MarketDocument43 paginiACFI1003 - Lecture 7 Corporations and The Share Market王亚琪Încă nu există evaluări

- Bravo PDFDocument11 paginiBravo PDFObu LawrenceÎncă nu există evaluări

- The National Budget of Bangladesh: A Comparative StudyDocument48 paginiThe National Budget of Bangladesh: A Comparative StudyQuazi Aritra Reyan80% (25)

- Rural Bank Case StudyDocument37 paginiRural Bank Case StudyRusselle Guste IgnacioÎncă nu există evaluări

- OpTransactionHistoryUX522 02 2024Document7 paginiOpTransactionHistoryUX522 02 2024piyush882676Încă nu există evaluări

- VAT Invoice - 2023-02-28 - 00000006062065-2302-9647607Document2 paginiVAT Invoice - 2023-02-28 - 00000006062065-2302-9647607falparslan5265Încă nu există evaluări

- Coffey V Ripple Labs ComplaintDocument32 paginiCoffey V Ripple Labs ComplaintShaurya MalwaÎncă nu există evaluări

- Why Invest in Africa?Document18 paginiWhy Invest in Africa?akiicÎncă nu există evaluări

- The Future of MoneyDocument4 paginiThe Future of MoneyChipwalter100% (1)

- Natural English Collocations PDFDocument97 paginiNatural English Collocations PDFOana Adriana Stroe0% (1)

- 04 Task Performance 1Document4 pagini04 Task Performance 1Kim JessiÎncă nu există evaluări

- Practice SumsDocument9 paginiPractice SumsThanuja BhaskarÎncă nu există evaluări

- 2022 - 02 - 03 Revision in Rates of NSSDocument10 pagini2022 - 02 - 03 Revision in Rates of NSSKhawaja Burhan0% (2)

- EMsq YCfz FT It ZZBWDocument7 paginiEMsq YCfz FT It ZZBWRaju BhaiÎncă nu există evaluări