S-ar putea să vă placă și

- LSL Acad Scotland HPI News Release May 12Document10 paginiLSL Acad Scotland HPI News Release May 12Stephen EmersonÎncă nu există evaluări

- IB Economics 1Document3 paginiIB Economics 1Igor NechaevÎncă nu există evaluări

- University of Gloucestershire: MBA-1 (GROUP-D)Document13 paginiUniversity of Gloucestershire: MBA-1 (GROUP-D)Nikunj PatelÎncă nu există evaluări

- August 2011 REBGV Statistics PackageDocument7 paginiAugust 2011 REBGV Statistics PackageMike StewartÎncă nu există evaluări

- Uk Residential Market Update: Another Multi-Speed YearDocument2 paginiUk Residential Market Update: Another Multi-Speed Yearrudy_wadhera4933Încă nu există evaluări

- Housing Snapshot - October 2011Document11 paginiHousing Snapshot - October 2011economicdelusionÎncă nu există evaluări

- 2018 01 15 News Release RLDocument26 pagini2018 01 15 News Release RLapi-125614979Încă nu există evaluări

- VancovDocument7 paginiVancovSteve LadurantayeÎncă nu există evaluări

- BBAC304 AssessmentDocument17 paginiBBAC304 Assessmentsherryy619Încă nu există evaluări

- 09 11 10 Final PoP ReleaseDocument2 pagini09 11 10 Final PoP Releaseapi-26178658Încă nu există evaluări

- Home Economic Report Oct 21Document2 paginiHome Economic Report Oct 21Adam WahedÎncă nu există evaluări

- Quarterly Review NOV11Document22 paginiQuarterly Review NOV11ftforee2Încă nu există evaluări

- Spotlight Key Themes For Uk Real Estate 2016Document6 paginiSpotlight Key Themes For Uk Real Estate 2016mannantawaÎncă nu există evaluări

- Freddie Mac August 2012 Economic OutlookDocument5 paginiFreddie Mac August 2012 Economic OutlookTamara InzunzaÎncă nu există evaluări

- Metropolitan Denver Real Estate Statistics AS OF JULY 31, 2011Document10 paginiMetropolitan Denver Real Estate Statistics AS OF JULY 31, 2011Michael KozlowskiÎncă nu există evaluări

- RP Data-Rismark Home Value IndexDocument4 paginiRP Data-Rismark Home Value IndexABC News OnlineÎncă nu există evaluări

- Newhome 8-23-11Document1 paginăNewhome 8-23-11Jessica Kister-LombardoÎncă nu există evaluări

- Australian Housing Chartbook July 2012Document13 paginiAustralian Housing Chartbook July 2012scribdooÎncă nu există evaluări

- Are Indias Cities in A Housing BubbleDocument9 paginiAre Indias Cities in A Housing BubbleAshwinBhandurgeÎncă nu există evaluări

- February 2010Document3 paginiFebruary 2010Steve LadurantayeÎncă nu există evaluări

- Olympic Glow Hides Economic Gloom: Residential Market UpdateDocument2 paginiOlympic Glow Hides Economic Gloom: Residential Market Updateapi-159978715Încă nu există evaluări

- REBGV Stats Package, August 2013Document9 paginiREBGV Stats Package, August 2013Victor SongÎncă nu există evaluări

- New Home Sales July 2011Document1 paginăNew Home Sales July 2011Jessica Kister-LombardoÎncă nu există evaluări

- Residential Newsletter 050510Document1 paginăResidential Newsletter 050510jwd780Încă nu există evaluări

- Victoria Real Estate Board Statistics Package August 2017Document4 paginiVictoria Real Estate Board Statistics Package August 2017Alexa HuffmanÎncă nu există evaluări

- Imla The New Normalprospects For 2020 and 2021 1Document25 paginiImla The New Normalprospects For 2020 and 2021 1Aminul IslamÎncă nu există evaluări

- Southall Property Market ReportDocument50 paginiSouthall Property Market ReportLaDy YeOnÎncă nu există evaluări

- FEL Newsletter October 2009Document4 paginiFEL Newsletter October 2009FirstEquityLtdÎncă nu există evaluări

- 49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014Document17 pagini49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014girishrajsÎncă nu există evaluări

- RP Data Rismark Home Value Index 1 May 2013 FINALDocument3 paginiRP Data Rismark Home Value Index 1 May 2013 FINALleithvanonselenÎncă nu există evaluări

- Move Smartly Report - Aug 2023Document24 paginiMove Smartly Report - Aug 2023subzerohÎncă nu există evaluări

- CREA July 30 2010 ForecastDocument3 paginiCREA July 30 2010 ForecastMike FotiouÎncă nu există evaluări

- Housing and The Economy: AUTUMN 2013Document16 paginiHousing and The Economy: AUTUMN 2013faidras2Încă nu există evaluări

- RPData SeptDocument5 paginiRPData SepteconomicdelusionÎncă nu există evaluări

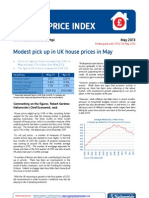

- Modest Pick Up in UK House Prices in MayDocument3 paginiModest Pick Up in UK House Prices in Mayapi-219138607Încă nu există evaluări

- January 2011 Portland Oregon Market Statistics Courtesy of Liste2Sold Andrew BeachDocument7 paginiJanuary 2011 Portland Oregon Market Statistics Courtesy of Liste2Sold Andrew BeachAndrewBeachÎncă nu există evaluări

- VietRees Newsletter 61 Week2 Month12 Year08Document10 paginiVietRees Newsletter 61 Week2 Month12 Year08internationalvr100% (1)

- Edinburgh City Index: Stock Levels Rise Ahead of Tax Rate ChangeDocument2 paginiEdinburgh City Index: Stock Levels Rise Ahead of Tax Rate ChangeBea LorinczÎncă nu există evaluări

- News Release: Prices Hold Firm As Home Buyers and Sellers Conclude 2012 From The SidelinesDocument9 paginiNews Release: Prices Hold Firm As Home Buyers and Sellers Conclude 2012 From The SidelinesUber CieloÎncă nu există evaluări

- MSR - Monthly Statistics Release - December 2011Document4 paginiMSR - Monthly Statistics Release - December 2011Bertrand FontaneauÎncă nu există evaluări

- OahuMonthlyIndicators Sept 2011Document13 paginiOahuMonthlyIndicators Sept 2011Mathew NgoÎncă nu există evaluări

- Key Points: JANUARY 2010 The Outlook For Commercial PropertyDocument7 paginiKey Points: JANUARY 2010 The Outlook For Commercial Propertysekar_smrÎncă nu există evaluări

- Consumer Price Inflation, UK: September 2022: NoticeDocument45 paginiConsumer Price Inflation, UK: September 2022: NoticeDuc-Anh NguyenÎncă nu există evaluări

- London Housing Bubble 2014Document2 paginiLondon Housing Bubble 2014harshal7788Încă nu există evaluări

- MLS Forecast News Release ENGDocument3 paginiMLS Forecast News Release ENGSteve LadurantayeÎncă nu există evaluări

- Property Report MelbourneDocument0 paginiProperty Report MelbourneMichael JordanÎncă nu există evaluări

- BNP PARIBAS REAL Uk-Economic-And-Real-Estate-Briefing-September-2022Document14 paginiBNP PARIBAS REAL Uk-Economic-And-Real-Estate-Briefing-September-2022hamza3iqbalÎncă nu există evaluări

- BCREA REPORT 2011 02 - Vancouver Real EstateDocument3 paginiBCREA REPORT 2011 02 - Vancouver Real EstateAnna AsiÎncă nu există evaluări

- Weekend Market Summary Week Ending 2014 March 2Document3 paginiWeekend Market Summary Week Ending 2014 March 2Australian Property ForumÎncă nu există evaluări

- Onsumer Atch Anada: Canadian Housing Prices - Beware of The AverageDocument4 paginiOnsumer Atch Anada: Canadian Housing Prices - Beware of The AverageSteve LadurantayeÎncă nu există evaluări

- WR May News 2010Document2 paginiWR May News 2010Wakefield Reutlinger RealtorsÎncă nu există evaluări

- Economics Coursework: Question 1: UK Housing Price PatternsDocument4 paginiEconomics Coursework: Question 1: UK Housing Price Patternsxavier bourret sicotteÎncă nu există evaluări

- June 2010Document3 paginiJune 2010Steve LadurantayeÎncă nu există evaluări

- Rightmove House Price Index: The Largest Monthly Sample of Residential Property PricesDocument7 paginiRightmove House Price Index: The Largest Monthly Sample of Residential Property PricesKris WongÎncă nu există evaluări

- ANZ Greater China Weekly Insight 2 April 2013Document13 paginiANZ Greater China Weekly Insight 2 April 2013leithvanonselenÎncă nu există evaluări

- Consumer Price Inflation, UK December 2022Document47 paginiConsumer Price Inflation, UK December 2022DandizzyÎncă nu există evaluări

- Australian Rental Market Discussion PaperDocument7 paginiAustralian Rental Market Discussion PaperBob odenkirkÎncă nu există evaluări

- Brexit: The Impact of ‘Brexit’ on the United KingdomDe la EverandBrexit: The Impact of ‘Brexit’ on the United KingdomÎncă nu există evaluări

- UNECE International Fire Safety Standards October 2020Document60 paginiUNECE International Fire Safety Standards October 2020Anwar MokalamÎncă nu există evaluări

- Land Act 1998 As Amended CAP 227Document77 paginiLand Act 1998 As Amended CAP 227Richard Simon KisituÎncă nu există evaluări

- Property Land Titles Deeds Preweek Pointers by Prof. Manuel Riguera PDFDocument390 paginiProperty Land Titles Deeds Preweek Pointers by Prof. Manuel Riguera PDFPax AlquizaÎncă nu există evaluări

- Plan Sanction Submission FormDocument5 paginiPlan Sanction Submission FormVetri VendanÎncă nu există evaluări

- Property Cases (Set 4) - AccessionDocument7 paginiProperty Cases (Set 4) - AccessionJewel CantileroÎncă nu există evaluări

- Midterm Sales 1Document11 paginiMidterm Sales 1Racheal SantosÎncă nu există evaluări

- Immovables by Nature Under Article 467 of The Civil CodeDocument10 paginiImmovables by Nature Under Article 467 of The Civil CodeHazel Norberte SurbidaÎncă nu există evaluări

- CES Handout SP Nov6Document87 paginiCES Handout SP Nov6Jouhara San JuanÎncă nu există evaluări

- Deed of Absolute SaleDocument3 paginiDeed of Absolute SaleKevin SerranoÎncă nu există evaluări

- Ctatan StokDocument261 paginiCtatan Stoklinarosalina5684Încă nu există evaluări

- Lesson 1.2 Introduction On Land RegistrationDocument12 paginiLesson 1.2 Introduction On Land RegistrationJannet BencureÎncă nu există evaluări

- Mckibbins PropertyDocument3 paginiMckibbins PropertyManas AÎncă nu există evaluări

- 3 Limketkai Sons Milling, Inc. vs. Court of Appeals, 255 SCRA 626, March 29, 1996Document36 pagini3 Limketkai Sons Milling, Inc. vs. Court of Appeals, 255 SCRA 626, March 29, 1996Apple BottomÎncă nu există evaluări

- Ponencias of J. Caguioa in CIVIL LAW 2022Document343 paginiPonencias of J. Caguioa in CIVIL LAW 2022Paolo Ollero100% (1)

- Family Member Lease Agreement: Page 1 of 3Document3 paginiFamily Member Lease Agreement: Page 1 of 3Guadalupe E FloresÎncă nu există evaluări

- Liye - Info Jaipur Architects List of Architects in Jaipur Anand Properties PRDocument1 paginăLiye - Info Jaipur Architects List of Architects in Jaipur Anand Properties PRaman3327100% (1)

- Tax 2 Part 3 Estate TaxDocument25 paginiTax 2 Part 3 Estate TaxShane TorrieÎncă nu există evaluări

- Doctrine of MarshallingDocument6 paginiDoctrine of MarshallingKinshuk BaruaÎncă nu există evaluări

- PLP Freeholds PDFDocument22 paginiPLP Freeholds PDFHedley Horler (scribd)Încă nu există evaluări

- Ts T Mobile 011 170818 - Filing - HoskinsrdDocument74 paginiTs T Mobile 011 170818 - Filing - HoskinsrdClaudio Alvarado ArayaÎncă nu există evaluări

- G.R. No. 229076Document6 paginiG.R. No. 229076Scrib LawÎncă nu există evaluări

- Gozamin PaperDocument37 paginiGozamin PaperDegearege AndualemÎncă nu există evaluări

- CAIRO - Q3 2014 - FINAL 2-RealestateDocument8 paginiCAIRO - Q3 2014 - FINAL 2-RealestateAli HosnyÎncă nu există evaluări

- DPC IiDocument13 paginiDPC Iishailesh latkarÎncă nu există evaluări

- Ecs Eu EU enDocument20 paginiEcs Eu EU enNata K.Încă nu există evaluări

- Listening Review 2 - TestDocument3 paginiListening Review 2 - TestNguyễn Thị Thanh ThưÎncă nu există evaluări

- Kkelson Groujp: EdmontonDocument1 paginăKkelson Groujp: EdmontonRyan PicheÎncă nu există evaluări

- Residential Rental Application: Applicant InformationDocument3 paginiResidential Rental Application: Applicant Informationapi-115282286Încă nu există evaluări

- Land Revenue Settlement: Kangra DistrictDocument70 paginiLand Revenue Settlement: Kangra DistrictAniket SharmaÎncă nu există evaluări

- Speaking Card - HouseDocument2 paginiSpeaking Card - HousePG47 Cao Phương AnhÎncă nu există evaluări