S-ar putea să vă placă și

- Notice of ClaimDocument6 paginiNotice of ClaimScott Atkinson100% (3)

- Hotis Notice of ViolationDocument4 paginiHotis Notice of ViolationScott AtkinsonÎncă nu există evaluări

- LTR - Da and Mayor - NoticeDocument1 paginăLTR - Da and Mayor - NoticeScott AtkinsonÎncă nu există evaluări

- Morse LawsuitDocument31 paginiMorse LawsuitScott AtkinsonÎncă nu există evaluări

- Letter of Support TemplateDocument1 paginăLetter of Support TemplateScott AtkinsonÎncă nu există evaluări

- Summons and ComplaintDocument8 paginiSummons and ComplaintScott AtkinsonÎncă nu există evaluări

- Cease and Desist Letter To Mayor Jeffrey Smith, Dec. 16, 2022Document2 paginiCease and Desist Letter To Mayor Jeffrey Smith, Dec. 16, 2022NewzjunkyÎncă nu există evaluări

- 23rd Annual Community SurveyDocument125 pagini23rd Annual Community SurveyScott AtkinsonÎncă nu există evaluări

- Career Probationary Firefighter Dies During SCBA ConfidenceDocument43 paginiCareer Probationary Firefighter Dies During SCBA ConfidenceScott AtkinsonÎncă nu există evaluări

- 2023 St. Lawrence County Budget in Brief Executive SummaryDocument2 pagini2023 St. Lawrence County Budget in Brief Executive SummaryScott AtkinsonÎncă nu există evaluări

- Division of Human Rights Determination After Investigation 1Document16 paginiDivision of Human Rights Determination After Investigation 1Scott AtkinsonÎncă nu există evaluări

- Carri Paige Court DocumentDocument4 paginiCarri Paige Court DocumentScott Atkinson100% (1)

- Division of Human Rights Determination After Investigation 1Document16 paginiDivision of Human Rights Determination After Investigation 1Scott AtkinsonÎncă nu există evaluări

- St. Lawrence County News ReleaseDocument3 paginiSt. Lawrence County News ReleaseScott AtkinsonÎncă nu există evaluări

- 2023 Ogdensburg Preliminary BudgetDocument135 pagini2023 Ogdensburg Preliminary BudgetScott AtkinsonÎncă nu există evaluări

- Code and Safety Evaluation ReportDocument5 paginiCode and Safety Evaluation ReportScott AtkinsonÎncă nu există evaluări

- Court FilingDocument2 paginiCourt FilingScott AtkinsonÎncă nu există evaluări

- Hotis Order of RemedyDocument4 paginiHotis Order of RemedyScott AtkinsonÎncă nu există evaluări

- Lewic County 15th Report Merged With Appendix 2-25-22Document82 paginiLewic County 15th Report Merged With Appendix 2-25-22Scott AtkinsonÎncă nu există evaluări

- CitiBus Modified ScheduleDocument1 paginăCitiBus Modified ScheduleScott AtkinsonÎncă nu există evaluări

- 2021 Regional EISDocument7 pagini2021 Regional EISScott AtkinsonÎncă nu există evaluări

- Carri Paige Court DocumentDocument5 paginiCarri Paige Court DocumentScott AtkinsonÎncă nu există evaluări

- Appellate Division, Fourth Judicial Department: Supreme Court of The State of New YorkDocument14 paginiAppellate Division, Fourth Judicial Department: Supreme Court of The State of New YorkScott AtkinsonÎncă nu există evaluări

- Jefferson County Legislator Scott Gray Will Run For AssemblyDocument2 paginiJefferson County Legislator Scott Gray Will Run For AssemblyNorth Country This WeekÎncă nu există evaluări

- Public Parking Letter To The City 2-7-22Document3 paginiPublic Parking Letter To The City 2-7-22Scott AtkinsonÎncă nu există evaluări

- Final Report - Economic and Fiscal Impact of OHVs - Lewis CountyDocument34 paginiFinal Report - Economic and Fiscal Impact of OHVs - Lewis CountyScott AtkinsonÎncă nu există evaluări

- Goodwin DecisionDocument2 paginiGoodwin DecisionScott AtkinsonÎncă nu există evaluări

- Updated Quarantine and Isolation 01.04.22Document2 paginiUpdated Quarantine and Isolation 01.04.22Scott AtkinsonÎncă nu există evaluări

- Firefighters Union StatementDocument2 paginiFirefighters Union StatementScott AtkinsonÎncă nu există evaluări

- Updated Safety Policy DOCCSDocument1 paginăUpdated Safety Policy DOCCSScott AtkinsonÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Template Excel Pengantar AkuntansiiDocument15 paginiTemplate Excel Pengantar AkuntansiiKim SeokjinÎncă nu există evaluări

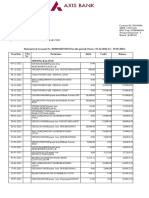

- Garima Axis Bank SDocument3 paginiGarima Axis Bank SSajan Sharma100% (1)

- DBP Vs GuarinaDocument2 paginiDBP Vs GuarinaMonalizts D.100% (1)

- ECB & Fed A Comparison A Comparison: International Summer ProgramDocument40 paginiECB & Fed A Comparison A Comparison: International Summer Programsabiha12Încă nu există evaluări

- Internal Audit For Finance SectorDocument1 paginăInternal Audit For Finance SectorSURYA SÎncă nu există evaluări

- Retail IndustryDocument3 paginiRetail IndustryakavinashkillerÎncă nu există evaluări

- UnileverDocument5 paginiUnileverKevin PratamaÎncă nu există evaluări

- TaxSaleResearch OkDocument44 paginiTaxSaleResearch OkMarlon Ferraro100% (1)

- SOLMAN-CHAPTER-14-INVESTMENTS-IN-ASSOCIATES_IA-PART-1B_2020ed (3)Document27 paginiSOLMAN-CHAPTER-14-INVESTMENTS-IN-ASSOCIATES_IA-PART-1B_2020ed (3)Meeka CalimagÎncă nu există evaluări

- Tech UnicornsDocument16 paginiTech UnicornsSatishÎncă nu există evaluări

- ICICI ProjectDocument55 paginiICICI ProjectRamana GÎncă nu există evaluări

- Bank Reconciliation (Practice Quiz)Document4 paginiBank Reconciliation (Practice Quiz)MoniqueÎncă nu există evaluări

- Power Notes: BudgetingDocument46 paginiPower Notes: BudgetingfrostyangelÎncă nu există evaluări

- PRMS FAQsDocument3 paginiPRMS FAQsfriendbceÎncă nu există evaluări

- Republic of Austria Investor Information PDFDocument48 paginiRepublic of Austria Investor Information PDFMi JpÎncă nu există evaluări

- Van Den Berghs LTD V ClarkDocument6 paginiVan Den Berghs LTD V ClarkShivanjani KumarÎncă nu există evaluări

- Ch25 Insurance OperationsDocument42 paginiCh25 Insurance OperationsTHIVIYATHINI PERUMALÎncă nu există evaluări

- Negen Capital: (Portfolio Management Service)Document5 paginiNegen Capital: (Portfolio Management Service)Sumit SagarÎncă nu există evaluări

- A Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFDocument7 paginiA Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFMegan Jane JohnsonÎncă nu există evaluări

- Uno Minda RameezDocument139 paginiUno Minda RameezRameez TkÎncă nu există evaluări

- SECP Form 6Document4 paginiSECP Form 6mirza faisalÎncă nu există evaluări

- Biz Cafe Operations Excel - Assignment - UIDDocument3 paginiBiz Cafe Operations Excel - Assignment - UIDJenna AgeebÎncă nu există evaluări

- Ruchi Soya Is One of The Largest Manufacturers of Edible Oil in India. Ruchi Soya IndustriesDocument3 paginiRuchi Soya Is One of The Largest Manufacturers of Edible Oil in India. Ruchi Soya IndustriesHarshit GuptaÎncă nu există evaluări

- ABC7Document6 paginiABC7Melissa R.100% (3)

- Buying - A - House - in - The - Netherlands ABNDocument24 paginiBuying - A - House - in - The - Netherlands ABNilkerÎncă nu există evaluări

- Risk Management Strategies G2 - 20.3 (Final)Document4 paginiRisk Management Strategies G2 - 20.3 (Final)Phuong Anh NguyenÎncă nu există evaluări

- Online BankingDocument38 paginiOnline BankingROSHNI AZAMÎncă nu există evaluări

- Updates in Financial Reporting StandardsDocument24 paginiUpdates in Financial Reporting Standardsloyd smithÎncă nu există evaluări

- PDF September Ict Notespdf - CompressDocument14 paginiPDF September Ict Notespdf - CompressSagar BhandariÎncă nu există evaluări

- Lack of Profit Loss Sharing in Islamic Banking Management and Control ImbalancesDocument27 paginiLack of Profit Loss Sharing in Islamic Banking Management and Control ImbalancesselkatibÎncă nu există evaluări