S-ar putea să vă placă și

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- 2020 MDCN Remita LicenseDocument1 pagină2020 MDCN Remita LicenseFavour MichaelÎncă nu există evaluări

- Summary and Conclusions: Chapter Review and Self-Test ProblemsDocument4 paginiSummary and Conclusions: Chapter Review and Self-Test ProblemsSyed Asim AliÎncă nu există evaluări

- LIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentDocument11 paginiLIC's JEEVAN RAKSHAK (UIN: 512N289V01) - : Policy DocumentSaravanan DuraiÎncă nu există evaluări

- 5th Amended Motion To VacateDocument13 pagini5th Amended Motion To Vacateajv3759Încă nu există evaluări

- Study On Customer Perception Towards E-Banking Services: A Summer Training Project ReportDocument56 paginiStudy On Customer Perception Towards E-Banking Services: A Summer Training Project ReportahenmakkÎncă nu există evaluări

- Mozambique Tourist Visa ApplicationDocument5 paginiMozambique Tourist Visa ApplicationMaria José Andrade PadillaÎncă nu există evaluări

- Insurance AwarenessDocument12 paginiInsurance Awarenessbhaskardoley30385215Încă nu există evaluări

- Doctrine of TracingDocument34 paginiDoctrine of TracingAkmal SafwanÎncă nu există evaluări

- A Project Report On Recruitment and Selection of Financial Consultant in HDFCDocument90 paginiA Project Report On Recruitment and Selection of Financial Consultant in HDFCBishnujyoti DasÎncă nu există evaluări

- Nmims SBM Mumbai Final Placement Report 2016Document8 paginiNmims SBM Mumbai Final Placement Report 2016IshaanVijaywargiyaÎncă nu există evaluări

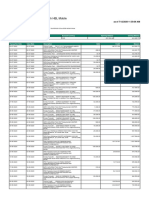

- Account Activity Generated Through HBL MobileDocument2 paginiAccount Activity Generated Through HBL MobileAðnan YasinÎncă nu există evaluări

- BlackstoneDocument2 paginiBlackstoneaidem100% (2)

- Business Plan Template Excel FreeDocument13 paginiBusiness Plan Template Excel FreeShreya More75% (8)

- FYP Risk Management HDFC SecuritiesDocument82 paginiFYP Risk Management HDFC Securitiespadmakar_rajÎncă nu există evaluări

- Mastercard Switch RulesDocument80 paginiMastercard Switch RulesBaluÎncă nu există evaluări

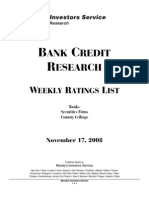

- ANK Redit Esearch: Eekly Atings ISTDocument118 paginiANK Redit Esearch: Eekly Atings ISTegutman1Încă nu există evaluări

- FY19 Global MNC Plan FinalDocument21 paginiFY19 Global MNC Plan FinalMARTHA HDEZÎncă nu există evaluări

- Introduction EbcDocument5 paginiIntroduction EbckmkesavanÎncă nu există evaluări

- RBA APU PPT - OJK 16 April 2018 PDFDocument46 paginiRBA APU PPT - OJK 16 April 2018 PDFBunnyÎncă nu există evaluări

- Happy Rewards Redemption Form BSN 2017 PDFDocument1 paginăHappy Rewards Redemption Form BSN 2017 PDFTc FaridahÎncă nu există evaluări

- Darvas Box SummaryDocument7 paginiDarvas Box SummaryVijayÎncă nu există evaluări

- Insurance Regulation, 2049 (1993) : Chapter - 1 Preliminary 1. Short Title and CommencementDocument41 paginiInsurance Regulation, 2049 (1993) : Chapter - 1 Preliminary 1. Short Title and CommencementAAnit SapkotaÎncă nu există evaluări

- Merger and Acquisition in Bank Sector in IndiaDocument63 paginiMerger and Acquisition in Bank Sector in IndiaOmkar Chavan0% (1)

- Depositry Service TinuDocument76 paginiDepositry Service TinunainakhushbooÎncă nu există evaluări

- Credit Card DetailsDocument5 paginiCredit Card DetailsSyed Farid AliÎncă nu există evaluări

- Confirmation and Acknowledgment - OfW Signing The Docs v2.0Document1 paginăConfirmation and Acknowledgment - OfW Signing The Docs v2.0Carlo Josef TabulogÎncă nu există evaluări

- RaresDocument2 paginiRaresLohanel RaresÎncă nu există evaluări

- Definition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesDocument8 paginiDefinition and Explanation:: (1) - Adjusting Entries That Convert Assets To ExpensesKae Abegail GarciaÎncă nu există evaluări

- Simply Homemade - Issue 53, 2015Document100 paginiSimply Homemade - Issue 53, 2015EverydayI100% (2)

- Agri Trade WebDocument4 paginiAgri Trade WebasdfasdfasdfÎncă nu există evaluări