S-ar putea să vă placă și

- Questions CH 8Document5 paginiQuestions CH 8Anonymous Jf9PYY2E8Încă nu există evaluări

- Canadian dollar's forward rate should exhibit a premiumDocument3 paginiCanadian dollar's forward rate should exhibit a premiumPhước NguyễnÎncă nu există evaluări

- The Canadian Dollar's Forward Rate Should Exhibit A DiscountDocument3 paginiThe Canadian Dollar's Forward Rate Should Exhibit A DiscountPhước NguyễnÎncă nu există evaluări

- Applying IRP and IFEDocument2 paginiApplying IRP and IFEAriel LogachoÎncă nu există evaluări

- IFE, PPP, and exchange rate forecastingDocument21 paginiIFE, PPP, and exchange rate forecastingyashpareek5100% (1)

- Int'l B & F CH 8Document3 paginiInt'l B & F CH 8Escherika WilliamsÎncă nu există evaluări

- Chapter 8 12Document21 paginiChapter 8 12adeel khÎncă nu există evaluări

- Parab (2010) Purchasing Power Parity Theory Problems PDFDocument4 paginiParab (2010) Purchasing Power Parity Theory Problems PDFAkash JainÎncă nu există evaluări

- Problemens On Foreign Exchange MarketDocument3 paginiProblemens On Foreign Exchange MarketTeffi Boyer MontoyaÎncă nu există evaluări

- TUTORIAL 6 SOLUTION GUIDE (From Chapter 8) Q4Document5 paginiTUTORIAL 6 SOLUTION GUIDE (From Chapter 8) Q4hien05Încă nu există evaluări

- Homework 7Document3 paginiHomework 7Ei AiÎncă nu există evaluări

- Homework 7 - Af455 - Umass - Fa21Document3 paginiHomework 7 - Af455 - Umass - Fa21Ei AiÎncă nu există evaluări

- TCQT Chapter 8Document3 paginiTCQT Chapter 8ngantruong.31221022155Încă nu există evaluări

- UntitledDocument5 paginiUntitledsuperorbitalÎncă nu există evaluări

- Mid-Term Test: 6: Covered Interest ArbitrageDocument5 paginiMid-Term Test: 6: Covered Interest ArbitrageTrà MyÎncă nu există evaluări

- International Parity Condition Numericals With AnsDocument8 paginiInternational Parity Condition Numericals With AnsAnjali PaneruÎncă nu există evaluări

- Exercise: Exchange Rate DeterminationDocument9 paginiExercise: Exchange Rate DeterminationRitik gargÎncă nu există evaluări

- Financial Market TextBook (Dragged)Document2 paginiFinancial Market TextBook (Dragged)Nick OoiÎncă nu există evaluări

- Chapter 8-Relationships Among Inflation, Interest Rates, and Exchange Rates QuizDocument15 paginiChapter 8-Relationships Among Inflation, Interest Rates, and Exchange Rates Quizhy_saingheng_7602609100% (1)

- Fix 336Document6 paginiFix 336Bánh BaoÎncă nu există evaluări

- GI Book 6e-170-172Document3 paginiGI Book 6e-170-172ANH PHAM QUYNHÎncă nu există evaluări

- Tutorial Questions IFMDocument15 paginiTutorial Questions IFMShareceÎncă nu există evaluări

- Instructions:: Midterm Assignment FIN 444-Summer 2020Document2 paginiInstructions:: Midterm Assignment FIN 444-Summer 2020Tãjriñ Biñte ÃlãmÎncă nu există evaluări

- Homework Chapter 15 - Currency Exchange Rates, Forex Predictions & PPP TheoryDocument7 paginiHomework Chapter 15 - Currency Exchange Rates, Forex Predictions & PPP TheorySyed Hassan Raza Jafry0% (1)

- Madura Chapter 8Document9 paginiMadura Chapter 8MasiÎncă nu există evaluări

- FINA 4360 Homework 1 International FinanceDocument3 paginiFINA 4360 Homework 1 International FinanceFeem SirivechapunÎncă nu există evaluări

- Global Exam I Fall 2012Document4 paginiGlobal Exam I Fall 2012mauricio0327Încă nu există evaluări

- IlliquidDocument3 paginiIlliquidyến lêÎncă nu există evaluări

- Question and Answer - 35Document30 paginiQuestion and Answer - 35acc-expertÎncă nu există evaluări

- Chapter 7—International Arbitrage and Interest Rate ParityDocument11 paginiChapter 7—International Arbitrage and Interest Rate ParityRim RimÎncă nu există evaluări

- CÂU HỎI TRẮC NGHIỆM CHƯƠNG 5 PPPIFE 1Document5 paginiCÂU HỎI TRẮC NGHIỆM CHƯƠNG 5 PPPIFE 1Nhi PhanÎncă nu există evaluări

- FX Cfa ProblemsDocument8 paginiFX Cfa ProblemsMỹ Trâm Trương ThịÎncă nu există evaluări

- Quantitative Questions .: 1 The Spot Rate of The New Zealand Dollar Is $.78. A Call Option On New Zealand Dollars With ADocument2 paginiQuantitative Questions .: 1 The Spot Rate of The New Zealand Dollar Is $.78. A Call Option On New Zealand Dollars With AMahiÎncă nu există evaluări

- IFM TB Ch08Document9 paginiIFM TB Ch08isgodÎncă nu există evaluări

- PPP & IfeDocument5 paginiPPP & IfeViệt Anh TrươngÎncă nu există evaluări

- If Tut 4Document7 paginiIf Tut 4Ong CHÎncă nu există evaluări

- TCQT - Revision - Problem - For - Final - Exam 2023 Part 2Document2 paginiTCQT - Revision - Problem - For - Final - Exam 2023 Part 220070095Încă nu există evaluări

- International flows assignmentDocument5 paginiInternational flows assignmenttobias stubkjærÎncă nu există evaluări

- An Investor Based in The United States Wishes To InvestDocument1 paginăAn Investor Based in The United States Wishes To InvestLet's Talk With Hassan0% (1)

- Exchange Rate TheoriesDocument21 paginiExchange Rate Theoriesalekya.nyalapelli03Încă nu există evaluări

- Chapter 4 Questions on Exchange RatesDocument3 paginiChapter 4 Questions on Exchange Rateslynette_garner_1Încă nu există evaluări

- Individual Assignemngt IFMDocument2 paginiIndividual Assignemngt IFMGETAHUN ASSEFA ALEMU50% (2)

- (Macro) Bank Soal Uas - TutorkuDocument40 pagini(Macro) Bank Soal Uas - TutorkuDella BianchiÎncă nu există evaluări

- Relationships Among Inflation, Interest Rates, and Exchange RatesDocument13 paginiRelationships Among Inflation, Interest Rates, and Exchange RatesibrahimÎncă nu există evaluări

- Chapter 1 2Document3 paginiChapter 1 2K60 Đào Phương NgânÎncă nu există evaluări

- Chapter 4Document17 paginiChapter 4celinekhalil2003Încă nu există evaluări

- Homework Assignment - 6 AnswersDocument3 paginiHomework Assignment - 6 AnswersRamonaÎncă nu există evaluări

- Chapter 4Document14 paginiChapter 4Selena JungÎncă nu există evaluări

- Assignment4 - International Parity ConditionsDocument2 paginiAssignment4 - International Parity Conditionsrainrainy1Încă nu există evaluări

- Relative Purchasing Power Parity Relative Purchasing Power ParityDocument2 paginiRelative Purchasing Power Parity Relative Purchasing Power ParityMohammad HammoudehÎncă nu există evaluări

- bài tập tổng hợp ônDocument1 paginăbài tập tổng hợp ônHà Nguyễn100% (2)

- Principles ProblemSet11Document5 paginiPrinciples ProblemSet11Bernardo BarrezuetaÎncă nu există evaluări

- CÂU HỎI TRẮC NGHIỆM XÁC ĐỊNH TỶ GIÁ HỐI ĐOÁI 1Document3 paginiCÂU HỎI TRẮC NGHIỆM XÁC ĐỊNH TỶ GIÁ HỐI ĐOÁI 1Nhi PhanÎncă nu există evaluări

- Part 1 2nd AttemptDocument16 paginiPart 1 2nd AttemptCuitlahuac TogoÎncă nu există evaluări

- 641 MCFDocument15 pagini641 MCFshahnursouravÎncă nu există evaluări

- Is The US 2012 Presidential Election Tipping Point for the fall of the Greenback?De la EverandIs The US 2012 Presidential Election Tipping Point for the fall of the Greenback?Încă nu există evaluări

- Your Money and Your Life: A Lifetime Approach to Money ManagementDe la EverandYour Money and Your Life: A Lifetime Approach to Money ManagementEvaluare: 3 din 5 stele3/5 (1)

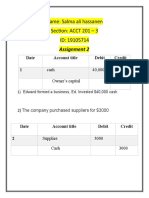

- Accounting transactions for Ed's businessDocument4 paginiAccounting transactions for Ed's businessAnonymous Jf9PYY2E8Încă nu există evaluări

- Assignment 2, Saif Salah, 19106048Document2 paginiAssignment 2, Saif Salah, 19106048Anonymous Jf9PYY2E8Încă nu există evaluări

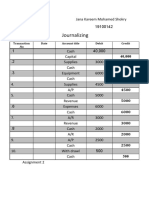

- Journalizing Transactions for Capital, Expenses, Revenue and AccountsDocument2 paginiJournalizing Transactions for Capital, Expenses, Revenue and AccountsAnonymous Jf9PYY2E8Încă nu există evaluări

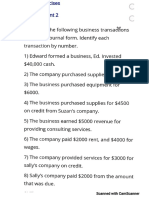

- Assignment Two: Journalize The Following Business Transactions in General Journal FormDocument2 paginiAssignment Two: Journalize The Following Business Transactions in General Journal FormAnonymous Jf9PYY2E8Încă nu există evaluări

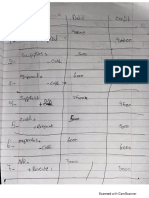

- CamScanner 04-17-2020 19.15.58Document3 paginiCamScanner 04-17-2020 19.15.58Anonymous Jf9PYY2E8Încă nu există evaluări

- Ahmed Tamer Mohamed 19106391 ACCT-201-3 Assignment 2: Date Account Debit CreditDocument1 paginăAhmed Tamer Mohamed 19106391 ACCT-201-3 Assignment 2: Date Account Debit CreditAnonymous Jf9PYY2E8Încă nu există evaluări

- Accounting Assignment Two: Name: Mariam Hesham Ahmed ID: 18100437Document1 paginăAccounting Assignment Two: Name: Mariam Hesham Ahmed ID: 18100437Anonymous Jf9PYY2E8Încă nu există evaluări

- Acc 2Document1 paginăAcc 2Anonymous Jf9PYY2E8Încă nu există evaluări

- Dr. Dina Kerema: Financial Accounting ACCT 201-3Document2 paginiDr. Dina Kerema: Financial Accounting ACCT 201-3Anonymous Jf9PYY2E8Încă nu există evaluări

- Name: K A D ID: 1710122 Course Code: ACCT-201-3: Subject: Assignment 1Document2 paginiName: K A D ID: 1710122 Course Code: ACCT-201-3: Subject: Assignment 1Anonymous Jf9PYY2E8Încă nu există evaluări

- Accounting Assignment 2 By: Hla Ahmed 19100169: General JournalDocument1 paginăAccounting Assignment 2 By: Hla Ahmed 19100169: General JournalAnonymous Jf9PYY2E8Încă nu există evaluări

- Ahmed Tamer Mohamed 19106391 ACCT-201-3 Assignment 2: Date Account Debit CreditDocument1 paginăAhmed Tamer Mohamed 19106391 ACCT-201-3 Assignment 2: Date Account Debit CreditAnonymous Jf9PYY2E8Încă nu există evaluări

- Take Home Exam GuidelinesDocument1 paginăTake Home Exam GuidelinesAnonymous Jf9PYY2E8Încă nu există evaluări

- Tutorial Excercises Week 2 Due in The Beginning of LectureDocument1 paginăTutorial Excercises Week 2 Due in The Beginning of LectureAnonymous Jf9PYY2E8Încă nu există evaluări

- CH 21 TB y PDFDocument9 paginiCH 21 TB y PDFAnonymous Jf9PYY2E8Încă nu există evaluări

- CH 21 TB y PDFDocument9 paginiCH 21 TB y PDFAnonymous Jf9PYY2E8Încă nu există evaluări

- CH 21 TB y PDFDocument9 paginiCH 21 TB y PDFAnonymous Jf9PYY2E8Încă nu există evaluări

- HW For DerivativesDocument4 paginiHW For DerivativesAnonymous Jf9PYY2E8Încă nu există evaluări

- CH 21 TB y PDFDocument9 paginiCH 21 TB y PDFAnonymous Jf9PYY2E8Încă nu există evaluări

- CH 21 TB y PDFDocument9 paginiCH 21 TB y PDFAnonymous Jf9PYY2E8Încă nu există evaluări

- CH OneDocument2 paginiCH OneAnonymous Jf9PYY2E8Încă nu există evaluări

- Does Beth's strategy support the IFEDocument11 paginiDoes Beth's strategy support the IFEAnonymous Jf9PYY2E8Încă nu există evaluări

- Tutorial 1Document3 paginiTutorial 1Anonymous Jf9PYY2E8Încă nu există evaluări

- CH 2 ExercisesDocument4 paginiCH 2 ExercisesAnonymous Jf9PYY2E80% (1)

- Test ScribdDocument1 paginăTest ScribdAnonymous Jf9PYY2E8Încă nu există evaluări

- Buy EffectDocument10 paginiBuy EffectAnonymous Jf9PYY2E8Încă nu există evaluări

- Test ScribdDocument1 paginăTest ScribdAnonymous Jf9PYY2E8Încă nu există evaluări

- Test ScribdDocument1 paginăTest ScribdAnonymous Jf9PYY2E8Încă nu există evaluări

- Duterte's 1st 100 Days: Drug War, Turning from US to ChinaDocument2 paginiDuterte's 1st 100 Days: Drug War, Turning from US to ChinaALISON RANIELLE MARCOÎncă nu există evaluări

- Organisational StructureDocument2 paginiOrganisational StructureAkshat GargÎncă nu există evaluări

- CAF608833F3F75B7Document47 paginiCAF608833F3F75B7BrahimÎncă nu există evaluări

- Republic Act No. 7638: December 9, 1992Document13 paginiRepublic Act No. 7638: December 9, 1992Clarisse TingchuyÎncă nu există evaluări

- Legal Status of Health CanadaDocument11 paginiLegal Status of Health CanadaMarc Boyer100% (2)

- Human Rights and the Death Penalty in the USDocument4 paginiHuman Rights and the Death Penalty in the USGerAkylÎncă nu există evaluări

- Juanito C. Pilar vs. Comelec G.R. NO. 115245 JULY 11, 1995: FactsDocument4 paginiJuanito C. Pilar vs. Comelec G.R. NO. 115245 JULY 11, 1995: FactsMaria Anny YanongÎncă nu există evaluări

- America's Health Insurance Plans PAC (AHIP) - 8227 - VSRDocument2 paginiAmerica's Health Insurance Plans PAC (AHIP) - 8227 - VSRZach EdwardsÎncă nu există evaluări

- Phil Hawk Vs Vivian Tan Lee DigestDocument2 paginiPhil Hawk Vs Vivian Tan Lee Digestfina_ong62590% (1)

- 0 PDFDocument1 pagină0 PDFIker Mack rodriguezÎncă nu există evaluări

- Intro To Aviation Ins (Fahamkan Je Tau)Document4 paginiIntro To Aviation Ins (Fahamkan Je Tau)Anisah NiesÎncă nu există evaluări

- Summary - Best BuyDocument4 paginiSummary - Best BuySonaliiiÎncă nu există evaluări

- APPLICATION FORM FOR Short Service Commission ExecutiveDocument1 paginăAPPLICATION FORM FOR Short Service Commission Executivemandhotra87Încă nu există evaluări

- Premachandra and Dodangoda v. Jayawickrema andDocument11 paginiPremachandra and Dodangoda v. Jayawickrema andPragash MaheswaranÎncă nu există evaluări

- 90 Cameron Granville V ChuaDocument1 pagină90 Cameron Granville V ChuaKrisha Marie CarlosÎncă nu există evaluări

- Life of Nelson Mandela, Short Biography of Nelson Mandela, Nelson Mandela Life and Times, Short Article On Nelson Mandela LifeDocument4 paginiLife of Nelson Mandela, Short Biography of Nelson Mandela, Nelson Mandela Life and Times, Short Article On Nelson Mandela LifeAmit KumarÎncă nu există evaluări

- Auguste Comte LectureDocument9 paginiAuguste Comte LectureAyinde SmithÎncă nu există evaluări

- The Medical Act of 1959Document56 paginiThe Medical Act of 1959Rogelio Junior RiveraÎncă nu există evaluări

- VAT: Value-Added Tax BasicsDocument42 paginiVAT: Value-Added Tax BasicsRobert WeightÎncă nu există evaluări

- VW - tb.26-07-07 Exhaust Heat Shield Replacement GuidelinesDocument2 paginiVW - tb.26-07-07 Exhaust Heat Shield Replacement GuidelinesMister MCÎncă nu există evaluări

- Millionaire EdgarDocument20 paginiMillionaire EdgarEdgar CemîrtanÎncă nu există evaluări

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument4 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSiraj PÎncă nu există evaluări

- Zener DiodoDocument4 paginiZener Diodoyes-caliÎncă nu există evaluări

- What is Aeronautical Product CertificationDocument12 paginiWhat is Aeronautical Product CertificationOscar RiveraÎncă nu există evaluări

- Pre-Incorporation Founders Agreement Among The Undersigned Parties, Effective (Date Signed)Document13 paginiPre-Incorporation Founders Agreement Among The Undersigned Parties, Effective (Date Signed)mishra1mayankÎncă nu există evaluări

- RPMS SY 2021-2022: Teacher Reflection Form (TRF)Document6 paginiRPMS SY 2021-2022: Teacher Reflection Form (TRF)Ma. Donna GeroleoÎncă nu există evaluări

- Spec Pro Case DoctrinesDocument4 paginiSpec Pro Case DoctrinesRalph Christian UsonÎncă nu există evaluări

- Institutions in KoreaDocument23 paginiInstitutions in Koreakinshoo shahÎncă nu există evaluări

- Far Eastern Bank (A Rural Bank) Inc. Annex A PDFDocument2 paginiFar Eastern Bank (A Rural Bank) Inc. Annex A PDFIris OmerÎncă nu există evaluări

- Apartment: TerminologyDocument19 paginiApartment: TerminologyMahlet AdugnaÎncă nu există evaluări