S-ar putea să vă placă și

- Bonds Payable Issued at A PremiumDocument6 paginiBonds Payable Issued at A PremiumCris Ann Marie ESPAnOLAÎncă nu există evaluări

- Module 1 Relevant CostingDocument6 paginiModule 1 Relevant CostingJohn Rey Bantay RodriguezÎncă nu există evaluări

- Finals - Takehome Quizzes Problems - WithoutDocument5 paginiFinals - Takehome Quizzes Problems - WithoutMaketh.ManÎncă nu există evaluări

- SAVANT FrameworkDocument19 paginiSAVANT Frameworkmarjorie blancoÎncă nu există evaluări

- Dealings in PropertyDocument62 paginiDealings in PropertyDonna May CacayorinÎncă nu există evaluări

- Quiz - PartnershipDocument2 paginiQuiz - PartnershipLeisleiRagoÎncă nu există evaluări

- Franchise AccountingDocument4 paginiFranchise AccountingJBÎncă nu există evaluări

- Complete First HW PartnershipDocument202 paginiComplete First HW PartnershipEsraRamosÎncă nu există evaluări

- LTCC 1Document3 paginiLTCC 1Jamie RamosÎncă nu există evaluări

- 4083 EvalDocument11 pagini4083 EvalPatrick ArazoÎncă nu există evaluări

- FIN 2 Financial Analysis and Reporting: Lyceum-Northwestern UniversityDocument7 paginiFIN 2 Financial Analysis and Reporting: Lyceum-Northwestern UniversityAmie Jane MirandaÎncă nu există evaluări

- FEU Financial AnalysisDocument18 paginiFEU Financial AnalysisRaph AngeloÎncă nu există evaluări

- Long Term Construction Contracts AssignmentDocument10 paginiLong Term Construction Contracts AssignmentAlleli Cruz100% (2)

- Scanner CAP II Financial ManagementDocument195 paginiScanner CAP II Financial ManagementEdtech NepalÎncă nu există evaluări

- Employee BenefitsDocument3 paginiEmployee BenefitsJAY AUBREY PINEDAÎncă nu există evaluări

- Chapter 10 Installment Sales AccountingDocument13 paginiChapter 10 Installment Sales AccountingFaithful FighterÎncă nu există evaluări

- 13 Financial Asset at Amortized CostDocument5 pagini13 Financial Asset at Amortized CostLara Jane Dela CruzÎncă nu există evaluări

- CHAPTER 9 Without AnswerDocument6 paginiCHAPTER 9 Without AnswerlenakaÎncă nu există evaluări

- Acco 20133 - Unit Iii & Iv - CreateDocument35 paginiAcco 20133 - Unit Iii & Iv - CreateHarvey AguilarÎncă nu există evaluări

- LTCC Exam PDF FreeDocument5 paginiLTCC Exam PDF FreeMichael Brian TorresÎncă nu există evaluări

- Empleo Intermediate Accounting 2019 Vol 1 CH 5 AnswersDocument24 paginiEmpleo Intermediate Accounting 2019 Vol 1 CH 5 AnswersBeat KarbÎncă nu există evaluări

- Chapter 1 - Accounting For PartnershipDocument13 paginiChapter 1 - Accounting For PartnershipKim EllaÎncă nu există evaluări

- CGT Drill Answers and ExplanationsDocument4 paginiCGT Drill Answers and ExplanationsMarianne Portia SumabatÎncă nu există evaluări

- BFINMAX Handout - Gross Profit Variance AnalysisDocument6 paginiBFINMAX Handout - Gross Profit Variance AnalysisDeo CoronaÎncă nu există evaluări

- Chap8 PDFDocument63 paginiChap8 PDFFathinus SyafrizalÎncă nu există evaluări

- Income Taxation Ind PracticeDocument3 paginiIncome Taxation Ind PracticeJanine Tividad100% (1)

- C8 (MC) - Cost Accounting by Carter (Part1)Document3 paginiC8 (MC) - Cost Accounting by Carter (Part1)AkiÎncă nu există evaluări

- 08 Joint ArrangementDocument3 pagini08 Joint ArrangementMelody Gumba0% (1)

- Beams9esm ch05Document5 paginiBeams9esm ch05David IroayÎncă nu există evaluări

- FINANCE LEASE-lecture and ExercisesDocument10 paginiFINANCE LEASE-lecture and ExercisesJamie CantubaÎncă nu există evaluări

- Polytechnic University of The PhilippinesDocument13 paginiPolytechnic University of The PhilippinesNathalie Padilla100% (1)

- Philippine Interpretations Committee (Pic) Questions and Answers (Q&As)Document6 paginiPhilippine Interpretations Committee (Pic) Questions and Answers (Q&As)Mary Jo Lariz OcliasoÎncă nu există evaluări

- Ch13 Current Liab and ContigenciesDocument46 paginiCh13 Current Liab and ContigenciesJane Masigan100% (1)

- Throughput Accounting F5 NotesDocument7 paginiThroughput Accounting F5 NotesSiddiqua KashifÎncă nu există evaluări

- Cost Volume Profit AnalysisDocument7 paginiCost Volume Profit Analysisrelatojr25100% (1)

- A. The Machine's Final Recorded Value Was P1,558,000Document7 paginiA. The Machine's Final Recorded Value Was P1,558,000Tawan VihokratanaÎncă nu există evaluări

- Section 19 Business Combination and Goodwill 1Document17 paginiSection 19 Business Combination and Goodwill 1AdrianneÎncă nu există evaluări

- Module 1.6 - Joint Arrangements PDFDocument3 paginiModule 1.6 - Joint Arrangements PDFMila MercadoÎncă nu există evaluări

- Conso Sale of PpeDocument6 paginiConso Sale of PpeMitch Delgado EmataÎncă nu există evaluări

- CH 15Document20 paginiCH 15grace guiuanÎncă nu există evaluări

- CH 14Document44 paginiCH 14NghiaBuiQuang100% (3)

- 1 ULO 1 To 3 Week 1 To 3 SHE Activities (AK)Document10 pagini1 ULO 1 To 3 Week 1 To 3 SHE Activities (AK)Margaux Phoenix KimilatÎncă nu există evaluări

- Handouts ConsolidationIntercompany Sale of Plant AssetsDocument3 paginiHandouts ConsolidationIntercompany Sale of Plant AssetsCPAÎncă nu există evaluări

- Sales and LeasebackDocument8 paginiSales and LeasebackHAZELMAE JEMINEZÎncă nu există evaluări

- Book Value Per Share Basic Earnings PerDocument61 paginiBook Value Per Share Basic Earnings Perayagomez100% (1)

- MICROEconimicsDocument120 paginiMICROEconimicsFerdi LlasosÎncă nu există evaluări

- Investments in Financial Instruments: Problem 1Document10 paginiInvestments in Financial Instruments: Problem 1Johanna Vidad100% (1)

- Chapter 6 - 2013 EdDocument17 paginiChapter 6 - 2013 EdJean Palada33% (6)

- Time Value of MoneyDocument52 paginiTime Value of MoneyJasmine Lailani ChulipaÎncă nu există evaluări

- MODULE 2 CVP AnalysisDocument8 paginiMODULE 2 CVP Analysissharielles /Încă nu există evaluări

- VarianceDocument2 paginiVarianceKenneth Bryan Tegerero Tegio0% (1)

- Non-Current Assets Held For SaleDocument20 paginiNon-Current Assets Held For Salerj batiyegÎncă nu există evaluări

- P 1Document27 paginiP 1Mark Lorenz SarionÎncă nu există evaluări

- Advanced Financial Accounting 1Document12 paginiAdvanced Financial Accounting 1Gemine Ailna Panganiban NuevoÎncă nu există evaluări

- Chapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Document20 paginiChapter 10 SolMan Accounting For Special Transactions 1 Millan 2018Alvin Jheii Sioco Alfonso0% (1)

- AC2401 Assurance and Auditing BibleDocument57 paginiAC2401 Assurance and Auditing BibleStreak CalmÎncă nu există evaluări

- 2019 Vol 1 CH 3 AnswersDocument13 pagini2019 Vol 1 CH 3 AnswersArkhie DavocolÎncă nu există evaluări

- 2019 Vol 1 CH 3 AnswersDocument14 pagini2019 Vol 1 CH 3 AnswersMarjorie NepomucenoÎncă nu există evaluări

- Intacc 1Document17 paginiIntacc 1Xyza Faye RegaladoÎncă nu există evaluări

- Ifrs 9 Debt Investment IllustrationDocument9 paginiIfrs 9 Debt Investment IllustrationVatchdemonÎncă nu există evaluări

- Winning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessDocument23 paginiWinning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessXander MerzaÎncă nu există evaluări

- 5 6181279385799098632Document34 pagini5 6181279385799098632Ally CapacioÎncă nu există evaluări

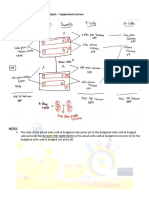

- 10 Gross Profit Variance Analysis - Supplement LectureDocument3 pagini10 Gross Profit Variance Analysis - Supplement LectureXander MerzaÎncă nu există evaluări

- OBLIGATIONS - Diagnostic ExercisesDocument37 paginiOBLIGATIONS - Diagnostic ExercisesAllanis SolisÎncă nu există evaluări

- Winning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessDocument23 paginiWinning Through Effective, Global Talent-The Changing Role of Strategic HRM in Int. BusinessXander MerzaÎncă nu există evaluări

- OBLIGATIONS - Diagnostic ExercisesDocument37 paginiOBLIGATIONS - Diagnostic ExercisesAllanis SolisÎncă nu există evaluări

- BACOSTMX - Module 1 Part 2 - Lecture - Cost Terms and ConceptsDocument58 paginiBACOSTMX - Module 1 Part 2 - Lecture - Cost Terms and ConceptsXander MerzaÎncă nu există evaluări

- CFAS Soln Man 2020 Edition 3Document3 paginiCFAS Soln Man 2020 Edition 3Xander MerzaÎncă nu există evaluări

- Propaganda MovementDocument1 paginăPropaganda MovementXander MerzaÎncă nu există evaluări

- BASTRCSX - Module 1Document67 paginiBASTRCSX - Module 1Xander MerzaÎncă nu există evaluări

- Adamson University Intermediate Accounting 1 - Cash Equivalents Prof. Judith Francisco - LunaDocument1 paginăAdamson University Intermediate Accounting 1 - Cash Equivalents Prof. Judith Francisco - LunaXander MerzaÎncă nu există evaluări

- Environmental GovernanceDocument68 paginiEnvironmental GovernanceXander MerzaÎncă nu există evaluări

- Operating Lease - Lessee: Problem 1Document2 paginiOperating Lease - Lessee: Problem 1Xander MerzaÎncă nu există evaluări

- Cash Voucher System PDFDocument2 paginiCash Voucher System PDFXander MerzaÎncă nu există evaluări

- Ias 33 Earnings Per Share SummaryDocument4 paginiIas 33 Earnings Per Share SummaryJhedz CartasÎncă nu există evaluări

- Corporation 1Document110 paginiCorporation 1Xander MerzaÎncă nu există evaluări

- Collateral For Loan Applications.: Receivable FinancingDocument3 paginiCollateral For Loan Applications.: Receivable FinancingXander MerzaÎncă nu există evaluări

- Corporation Lecture NotesDocument7 paginiCorporation Lecture NotesXander MerzaÎncă nu există evaluări

- Research Problem & Its Objectives: Elements of Chapter 1Document22 paginiResearch Problem & Its Objectives: Elements of Chapter 1Xander MerzaÎncă nu există evaluări

- Corporation 1Document110 paginiCorporation 1Xander MerzaÎncă nu există evaluări

- Review of Related LiteratureDocument13 paginiReview of Related LiteratureXander MerzaÎncă nu există evaluări

- Pas 2 InventoryDocument8 paginiPas 2 InventoryMark Lord Morales BumagatÎncă nu există evaluări

- Human RightsDocument37 paginiHuman RightsXander MerzaÎncă nu există evaluări

- 2023 Cryptoassets Blockchain SwitzerlandDocument26 pagini2023 Cryptoassets Blockchain SwitzerlandSarang PokhareÎncă nu există evaluări

- AC-215 SelfStuy GuideNYMEXDocument57 paginiAC-215 SelfStuy GuideNYMEXpravinshirnameÎncă nu există evaluări

- How To Pivot Successfully in BusinessDocument4 paginiHow To Pivot Successfully in BusinessSASI KUMAR SUNDARA RAJANÎncă nu există evaluări

- Virgin Mobile - Case StudyDocument13 paginiVirgin Mobile - Case StudyPurnendu Singh0% (1)

- Presentation On Capital MarketDocument20 paginiPresentation On Capital MarketYugesh PrajapatiÎncă nu există evaluări

- International MarketingDocument19 paginiInternational MarketingDenza Primananda AlfurqanÎncă nu există evaluări

- Harley-Davidson, Inc.: Case StudyDocument11 paginiHarley-Davidson, Inc.: Case StudyCameron O'Brien100% (1)

- Chapter 6 NotesDocument3 paginiChapter 6 NotesJay-P100% (1)

- The Real Nature of Intraday Market Behavior - Answer Key: Drill 1Document5 paginiThe Real Nature of Intraday Market Behavior - Answer Key: Drill 1Cr HtÎncă nu există evaluări

- MGT211 Introduction To Business More Than 200 MCQs For Preparation of Midterm ExamDocument21 paginiMGT211 Introduction To Business More Than 200 MCQs For Preparation of Midterm ExamBalach Malik57% (7)

- Marketing Management 6eDocument40 paginiMarketing Management 6e11 CÎncă nu există evaluări

- PuSm - Lecture 2 - Chapter 2 - Slides - OnlineDocument46 paginiPuSm - Lecture 2 - Chapter 2 - Slides - OnlineLaura FernandesÎncă nu există evaluări

- Bombay Stock ExchangeDocument32 paginiBombay Stock ExchangeAnurag Bajaj80% (5)

- Porto Free Powerpoint TemplateDocument9 paginiPorto Free Powerpoint TemplateTeneswari RadhaÎncă nu există evaluări

- Futures - Io Presentation Opening Reversals Al Brooks PDFDocument36 paginiFutures - Io Presentation Opening Reversals Al Brooks PDFAman SinhaÎncă nu există evaluări

- Tanishq: Positioning To Capture The Indian Woman's Heart: Presented By: Aboorva J A (K07003)Document10 paginiTanishq: Positioning To Capture The Indian Woman's Heart: Presented By: Aboorva J A (K07003)Prasaad TayadeÎncă nu există evaluări

- 2020 Hult Prize SCORECARD PACKAGE PDFDocument11 pagini2020 Hult Prize SCORECARD PACKAGE PDFFrancisco Javier Rosales RiveraÎncă nu există evaluări

- DellDocument4 paginiDellabdiÎncă nu există evaluări

- CH09Document86 paginiCH09Sal SCÎncă nu există evaluări

- 1 - Strategic Thinking, Profit Planning and CVP Analysis KeyDocument4 pagini1 - Strategic Thinking, Profit Planning and CVP Analysis KeyEdward Glenn BaguiÎncă nu există evaluări

- LB-Econmomics - 1st Cycle - HTTCDocument81 paginiLB-Econmomics - 1st Cycle - HTTClynsÎncă nu există evaluări

- A Project Report O1Document49 paginiA Project Report O1niraj3handeÎncă nu există evaluări

- Internship PPT (Sharekhan)Document28 paginiInternship PPT (Sharekhan)Kanika VermaÎncă nu există evaluări

- mgt211 Final Term 2009Document8 paginimgt211 Final Term 2009Prince HiraÎncă nu există evaluări

- Argentina and AustraliaDocument83 paginiArgentina and Australialectoris100% (1)

- Board Resolution and Share Holding PatternDocument2 paginiBoard Resolution and Share Holding PatternAtty. Emmanuel SandichoÎncă nu există evaluări

- Investing Principles - Financial UDocument80 paginiInvesting Principles - Financial UK4NO100% (1)

- Guidance On The Application of The 2004 Cpss-Iosco Recommendations For Central Counterparties To Otc Derivatives CcpsDocument44 paginiGuidance On The Application of The 2004 Cpss-Iosco Recommendations For Central Counterparties To Otc Derivatives CcpsChou ChantraÎncă nu există evaluări

- International Marketing Semina DurexDocument1 paginăInternational Marketing Semina DurexThanhHoàiNguyễnÎncă nu există evaluări

- Thank You For Your Valued OperationDocument1 paginăThank You For Your Valued OperationĦøÐâÎncă nu există evaluări