S-ar putea să vă placă și

- Prof Chowdari Prasad CV 26112018Document11 paginiProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadÎncă nu există evaluări

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocument39 pagini10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadÎncă nu există evaluări

- Second Innings September 2019Document52 paginiSecond Innings September 2019Prof Dr Chowdari PrasadÎncă nu există evaluări

- Digital Banking in India 2016Document21 paginiDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Consumer Protection Act 1986Document41 paginiConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocument15 paginiA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadÎncă nu există evaluări

- Performance of Crowd Funding in India: Issues and ChallengesDocument19 paginiPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Lean and Green Banking in India 2012Document20 paginiLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- Social Entrepreneurship2015Document45 paginiSocial Entrepreneurship2015Prof Dr Chowdari PrasadÎncă nu există evaluări

- Recent Trends of PE Funding in IndiaDocument38 paginiRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadÎncă nu există evaluări

- Profile of Banks 2010-11Document99 paginiProfile of Banks 2010-11Vishesh KumarÎncă nu există evaluări

- Tapmi Update 2013Document120 paginiTapmi Update 2013Prof Dr Chowdari PrasadÎncă nu există evaluări

- HR As A Strategic Business PartnerDocument36 paginiHR As A Strategic Business PartnerProf Dr Chowdari PrasadÎncă nu există evaluări

- Women Achievers Ebook2Document95 paginiWomen Achievers Ebook2Prof Dr Chowdari PrasadÎncă nu există evaluări

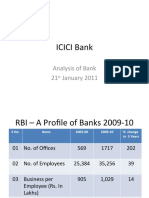

- Icici Bank: Analysis of Bank 21 January 2011Document6 paginiIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadÎncă nu există evaluări

- The Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Document11 paginiThe Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Prof Dr Chowdari PrasadÎncă nu există evaluări

- Myths of Microfinance - Global South Development Magazine JAN 2011Document42 paginiMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationÎncă nu există evaluări

- List of Books On Micro FinanceDocument32 paginiList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

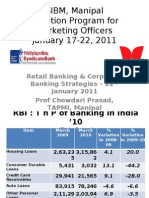

- Syndicate Institute of Bank Management, ManipalDocument67 paginiSyndicate Institute of Bank Management, ManipalProf Dr Chowdari PrasadÎncă nu există evaluări

- Sibm, RBCBDocument20 paginiSibm, RBCBProf Dr Chowdari PrasadÎncă nu există evaluări

- TAPMI ManipalDocument18 paginiTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- MFI National ConferenceDocument12 paginiMFI National ConferenceProf Dr Chowdari PrasadÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Treasury and Subsidiary Treasury RulesDocument407 paginiTreasury and Subsidiary Treasury RulesBilalNumanÎncă nu există evaluări

- The World Bank: IBRD & IDA: Working For A World Free of PovertyDocument28 paginiThe World Bank: IBRD & IDA: Working For A World Free of PovertyManish TiwariÎncă nu există evaluări

- Business Studies Class11 Chapter 4Document8 paginiBusiness Studies Class11 Chapter 4bhawnaÎncă nu există evaluări

- Robinson On "Full-Delivery" Mitigation For Wetlands and Streams.Document14 paginiRobinson On "Full-Delivery" Mitigation For Wetlands and Streams.Restoration Systems, LLCÎncă nu există evaluări

- Friday Bulletin 714Document12 paginiFriday Bulletin 714Jamia Nairobi100% (1)

- A 2 - Roles and Functions of Various Participants in Financial MarketDocument2 paginiA 2 - Roles and Functions of Various Participants in Financial MarketOsheen Singh100% (1)

- First National Bank - Google SearchDocument1 paginăFirst National Bank - Google SearchNiaaries JimÎncă nu există evaluări

- Front Office Cashier - PPTX QWDocument16 paginiFront Office Cashier - PPTX QWJen PequitÎncă nu există evaluări

- Role of Banks in Indian EconomyDocument2 paginiRole of Banks in Indian EconomyPriyanka MuppuriÎncă nu există evaluări

- QuestionsDocument40 paginiQuestionsriazahmad82Încă nu există evaluări

- Hku166 PDF EngDocument16 paginiHku166 PDF EngPaodou HuÎncă nu există evaluări

- Kepo Ah Ah Ah Ah Ah Ah AhDocument6 paginiKepo Ah Ah Ah Ah Ah Ah AhRizal Mahendra PrimadaniÎncă nu există evaluări

- Confirm LetterDocument2 paginiConfirm Letterowern kerÎncă nu există evaluări

- 1.kobank Application Form (Pls Print in Color)Document1 pagină1.kobank Application Form (Pls Print in Color)api-19759090Încă nu există evaluări

- Policy For Settlement of Claims in Respect of Deceased Account HoldersDocument52 paginiPolicy For Settlement of Claims in Respect of Deceased Account HoldersAaju KausikÎncă nu există evaluări

- Digest of G.R. No. 157314 July 29, 2005Document2 paginiDigest of G.R. No. 157314 July 29, 2005oliveÎncă nu există evaluări

- Tables: Calculators: Approved Calculators May Be Used. Stationary: Yellow Answer BookletDocument9 paginiTables: Calculators: Approved Calculators May Be Used. Stationary: Yellow Answer BookletMinh LeÎncă nu există evaluări

- E Payments in MauritiusDocument3 paginiE Payments in Mauritiuskurs23Încă nu există evaluări

- Bismillah Group ScandalDocument3 paginiBismillah Group ScandalAhmad HÎncă nu există evaluări

- Aug 2022Document24 paginiAug 2022Amar JeetÎncă nu există evaluări

- Boa Tos RFBTDocument6 paginiBoa Tos RFBTMr. CopernicusÎncă nu există evaluări

- Marquez Vs Desierto DigestDocument2 paginiMarquez Vs Desierto DigestKathleen CruzÎncă nu există evaluări

- I. Convertible Currencies With Bangko Sentral:: Run Date/timeDocument1 paginăI. Convertible Currencies With Bangko Sentral:: Run Date/timeLucito FalloriaÎncă nu există evaluări

- Daily Cash Flow Template ExcelDocument60 paginiDaily Cash Flow Template ExcelPro ResourcesÎncă nu există evaluări

- Digital CurrenciesDocument4 paginiDigital CurrenciesMoksshÎncă nu există evaluări

- Fundamentals of Partnership FirmDocument24 paginiFundamentals of Partnership FirmJyoti Sankar BairagiÎncă nu există evaluări

- Ielts 15Document15 paginiIelts 15cherry tejaÎncă nu există evaluări

- Charles Schwab Summary AgreementDocument2 paginiCharles Schwab Summary AgreementSteve Oreo100% (2)

- Customer Relationship ManagementDocument1 paginăCustomer Relationship ManagementYamini Katakam0% (1)

- Punjab and Sind Bank Services of Risk ManagementDocument12 paginiPunjab and Sind Bank Services of Risk Managementiyaps427100% (1)