S-ar putea să vă placă și

- Martelino Vs AlejandroDocument1 paginăMartelino Vs AlejandroCharm AgripaÎncă nu există evaluări

- Testimonial Evidence - Riano OutlineDocument3 paginiTestimonial Evidence - Riano OutlineCharm AgripaÎncă nu există evaluări

- Fraport II Vs PHDocument15 paginiFraport II Vs PHCharm Agripa100% (1)

- PIL Bernas ReviewerDocument23 paginiPIL Bernas ReviewerCharm AgripaÎncă nu există evaluări

- VAT Casasola NotesDocument7 paginiVAT Casasola NotesCharm AgripaÎncă nu există evaluări

- Petitioner Vs Vs Respondents Antonio F. Navarrete Paul Bernard T. IraoDocument13 paginiPetitioner Vs Vs Respondents Antonio F. Navarrete Paul Bernard T. IraoCharm AgripaÎncă nu există evaluări

- Home Society Claim PDFDocument13 paginiHome Society Claim PDFCharm AgripaÎncă nu există evaluări

- DPA QuickGuidefolder Insideonly PDFDocument1 paginăDPA QuickGuidefolder Insideonly PDFCharm AgripaÎncă nu există evaluări

- Case Concerning Military and Paramilitary Activities in and Against Nicaragua PDFDocument9 paginiCase Concerning Military and Paramilitary Activities in and Against Nicaragua PDFCharm AgripaÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Kerala Budget Analysis 2022-23Document7 paginiKerala Budget Analysis 2022-23Shakti MishraÎncă nu există evaluări

- Business Taxation QuizDocument5 paginiBusiness Taxation QuizWerpa PetmaluÎncă nu există evaluări

- Jeeves InsuranceDocument1 paginăJeeves InsuranceJEEVAN BONDARÎncă nu există evaluări

- CIR Vs Procter and Gamble 1Document1 paginăCIR Vs Procter and Gamble 1JVLÎncă nu există evaluări

- May 17Document1 paginăMay 17Bhanu Pratap ChoudhuryÎncă nu există evaluări

- Concentrix Daksh Services India Private Limited Payslip For The Month of September - 2021Document1 paginăConcentrix Daksh Services India Private Limited Payslip For The Month of September - 2021Prity PandeyÎncă nu există evaluări

- Boq Comparative ChartDocument4 paginiBoq Comparative ChartinfoÎncă nu există evaluări

- Direct and Indirect TaxesDocument14 paginiDirect and Indirect Taxeskratika singhÎncă nu există evaluări

- MBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 2Document23 paginiMBA104 - Almario - Parco - Chapter 1 Part 2 Individual Assignment Online Presentation 2Jesse Rielle CarasÎncă nu există evaluări

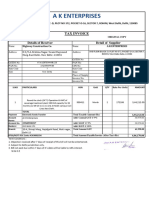

- Invoice AKE - 29 11 23Document1 paginăInvoice AKE - 29 11 23jaikant.hccÎncă nu există evaluări

- Itrv Sarath 21-22Document1 paginăItrv Sarath 21-22bindu mathaiÎncă nu există evaluări

- FIRS Circular Taxation of Non Residents in Nigeria 2021Document24 paginiFIRS Circular Taxation of Non Residents in Nigeria 2021Abdulhameed BabalolaÎncă nu există evaluări

- Cash Receipt Template 3 WordDocument1 paginăCash Receipt Template 3 WordSaqlain MalikÎncă nu există evaluări

- Zambia National Budget and Development Planning Policy (Draft)Document17 paginiZambia National Budget and Development Planning Policy (Draft)Chola Mukanga100% (2)

- UnknownDocument2 paginiUnknownSudip MondalÎncă nu există evaluări

- Computation of Total Income For ItrDocument2 paginiComputation of Total Income For Itravisinghoo7Încă nu există evaluări

- Airtech Systems (India) Pvt. LTD.: Salary Slip For The Month of October 2018Document1 paginăAirtech Systems (India) Pvt. LTD.: Salary Slip For The Month of October 2018Mohsin ShaikhÎncă nu există evaluări

- FIN AL: Form GSTR-3BDocument3 paginiFIN AL: Form GSTR-3Bprashant patilÎncă nu există evaluări

- ICT by DR.K.MALLIKARJUNA RAO PDFDocument5 paginiICT by DR.K.MALLIKARJUNA RAO PDFdr_mallikarjunaraoÎncă nu există evaluări

- Accounting Voucher DisplayDocument1 paginăAccounting Voucher DisplayAntara IndiaÎncă nu există evaluări

- Income Tax Calculation Sheet For 2020-21 VER 9.0: (Fill Colum N Only)Document8 paginiIncome Tax Calculation Sheet For 2020-21 VER 9.0: (Fill Colum N Only)Jnv MANACAMP RAIPURÎncă nu există evaluări

- Solved Curtis Is 50 Years Old and Has An Individual RetirementDocument1 paginăSolved Curtis Is 50 Years Old and Has An Individual RetirementAnbu jaromiaÎncă nu există evaluări

- Fee Structure 1Document3 paginiFee Structure 1Abhishek MitraÎncă nu există evaluări

- Courage vs. CIRDocument2 paginiCourage vs. CIRMike E Dm33% (3)

- Government of Rajasthan: Schedule of Income Tax (Budgethead 8658-00-112-00-00)Document5 paginiGovernment of Rajasthan: Schedule of Income Tax (Budgethead 8658-00-112-00-00)shane haiderÎncă nu există evaluări

- Web Kalvisolai It Form 2022 - Version - 1.1Document26 paginiWeb Kalvisolai It Form 2022 - Version - 1.1manivasagam subbianÎncă nu există evaluări

- Servlet ControllerDocument1 paginăServlet Controllermukesh sahuÎncă nu există evaluări

- Invoice IXITRS185875952789718Document1 paginăInvoice IXITRS185875952789718PatriotÎncă nu există evaluări

- Taxation During Commonwealth PeriodDocument18 paginiTaxation During Commonwealth PeriodLEIAN ROSE GAMBOA100% (2)

- Pay Slip July 2020...Document2 paginiPay Slip July 2020...laxman lucky100% (2)