S-ar putea să vă placă și

- EPCA Seminar: Olefins Outlook: 9 October 2020Document13 paginiEPCA Seminar: Olefins Outlook: 9 October 2020Aswin KondapallyÎncă nu există evaluări

- FMG China Fund - PresentationDocument15 paginiFMG China Fund - PresentationSusan AllenÎncă nu există evaluări

- What Is Really Killing The Irish EconomyDocument1 paginăWhat Is Really Killing The Irish EconomyLuis Riestra Delgado100% (1)

- Gerald CorcoranDocument9 paginiGerald CorcoranMarketsWikiÎncă nu există evaluări

- Florida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 paginiFlorida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenÎncă nu există evaluări

- J.C. Parets, CMTDocument25 paginiJ.C. Parets, CMTPunit TewaniÎncă nu există evaluări

- Goldman Asia Conviction Call Catch-Up 13sep10Document11 paginiGoldman Asia Conviction Call Catch-Up 13sep10tanmartinÎncă nu există evaluări

- Florida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 paginiFlorida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenÎncă nu există evaluări

- 2014 Comparing SARIMA and Holt Winter Model For Indian Automobile SectorDocument4 pagini2014 Comparing SARIMA and Holt Winter Model For Indian Automobile SectorShiv PrasadÎncă nu există evaluări

- 23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CADocument11 pagini23) Sacramento, CA: Figure 157: Year/Year Change in Existing Home Prices - Sacramento, CAsacrealstatsÎncă nu există evaluări

- MHIFU HandoutDocument2 paginiMHIFU HandoutThunder PigÎncă nu există evaluări

- Florida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocument16 paginiFlorida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenÎncă nu există evaluări

- Research Speak - 16-04-2010Document12 paginiResearch Speak - 16-04-2010A_KinshukÎncă nu există evaluări

- Job Losses Since December 2007Document1 paginăJob Losses Since December 2007EricFruitsÎncă nu există evaluări

- Philippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsDocument12 paginiPhilippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsJofred Dela VegaÎncă nu există evaluări

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Document71 pagini"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkÎncă nu există evaluări

- Florida's October Employment Figures Released: TallahasseeDocument16 paginiFlorida's October Employment Figures Released: TallahasseeMichael AllenÎncă nu există evaluări

- Florida's November Employment Figures ReleasedDocument16 paginiFlorida's November Employment Figures ReleasedMichael AllenÎncă nu există evaluări

- AS-AD Applications and Data InterpretationDocument2 paginiAS-AD Applications and Data Interpretationalanoud AlmheiriÎncă nu există evaluări

- Update On IDFC Arbitrage FundDocument6 paginiUpdate On IDFC Arbitrage FundGÎncă nu există evaluări

- South Korean Energy Outlook 2015Document13 paginiSouth Korean Energy Outlook 2015Afifa KamilaÎncă nu există evaluări

- Florida's June Employment Figures Released: Governor DirectorDocument16 paginiFlorida's June Employment Figures Released: Governor DirectorMichael AllenÎncă nu există evaluări

- September 2010Document1 paginăSeptember 2010Stephanie Miller HofmanÎncă nu există evaluări

- Unemployment DataDocument2 paginiUnemployment Datakettle1Încă nu există evaluări

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDocument16 paginiGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaÎncă nu există evaluări

- Introduction To M&A With Piramal Abbott DealDocument22 paginiIntroduction To M&A With Piramal Abbott DealSachidanand Singh100% (2)

- Russia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010Document21 paginiRussia 2010 Worth A Tactical Look: An Investor's Guide To The Risks and Opportunities in 2010jamesdb1Încă nu există evaluări

- ASX_Metals_and_MiningDocument4 paginiASX_Metals_and_Miningaliminsyah.caneÎncă nu există evaluări

- November 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?Document8 paginiNovember 2008 Update: Why Are Electricity Prices in RTOs Increasingly Expensive?RobertMcCulloughÎncă nu există evaluări

- Record Early Sales of New Crop U.S. Soybeans Signal Robust Demand AheadDocument33 paginiRecord Early Sales of New Crop U.S. Soybeans Signal Robust Demand AheadAvinash KarnÎncă nu există evaluări

- Derivatives in IndiaDocument21 paginiDerivatives in IndiaShajupaulÎncă nu există evaluări

- Outlook For The SMSF SectorDocument13 paginiOutlook For The SMSF SectorRomeoÎncă nu există evaluări

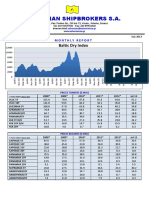

- Athenian-Shipbrokers-July 2013Document18 paginiAthenian-Shipbrokers-July 2013Nguyen Le Thu HaÎncă nu există evaluări

- Athenian Shipbrokers - Monthy Report - 14.07.15 PDFDocument18 paginiAthenian Shipbrokers - Monthy Report - 14.07.15 PDFgeorgevarsasÎncă nu există evaluări

- Gmo - For Whom The Bond TollsDocument8 paginiGmo - For Whom The Bond Tollsfreemind3682Încă nu există evaluări

- Presentation To Macquarie Corporate Day in Singapore & Hong KongDocument54 paginiPresentation To Macquarie Corporate Day in Singapore & Hong KongnigelburkeÎncă nu există evaluări

- athenian-shipbrokers-NOV 2010Document17 paginiathenian-shipbrokers-NOV 2010Nguyen Le Thu HaÎncă nu există evaluări

- Apollo Credit Market Outlook Jul23Document157 paginiApollo Credit Market Outlook Jul23supÎncă nu există evaluări

- SEB Commodities Monthly May 2010Document22 paginiSEB Commodities Monthly May 2010SEB GroupÎncă nu există evaluări

- MEF Analysis UI Claims - March 2020Document2 paginiMEF Analysis UI Claims - March 2020Dave AllenÎncă nu există evaluări

- HDFC Mutual FundDocument25 paginiHDFC Mutual Fundapi-25886395Încă nu există evaluări

- Livestock Price Volatility: Eric BelascoDocument15 paginiLivestock Price Volatility: Eric BelascoGlen YÎncă nu există evaluări

- Indian Stock Market AnalysisDocument36 paginiIndian Stock Market AnalysisTushar GangolyÎncă nu există evaluări

- in Our View,: Vrddhi Capital Investment AdvisorsDocument5 paginiin Our View,: Vrddhi Capital Investment AdvisorsMohit AgarwalÎncă nu există evaluări

- Baltics RevisitedDocument12 paginiBaltics RevisitedideanoiseÎncă nu există evaluări

- Equity Debt Strategy For Mar20Document25 paginiEquity Debt Strategy For Mar20Saad KhanÎncă nu există evaluări

- The Week That Just Passed March 12, 2010Document4 paginiThe Week That Just Passed March 12, 2010WallstreetableÎncă nu există evaluări

- Short and Medium Term OutlookDocument6 paginiShort and Medium Term OutlookTushar LanjekarÎncă nu există evaluări

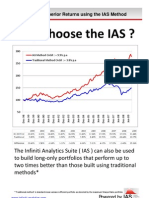

- Why Choose The IASDocument6 paginiWhy Choose The IASPeter UrbaniÎncă nu există evaluări

- Highlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldDocument19 paginiHighlights: S&P/ TSX Global Gold I Ndex Gold DXY I Ndex GoldkaiselkÎncă nu există evaluări

- Southeast Texas Labor StatisticsDocument1 paginăSoutheast Texas Labor StatisticsCharlie FoxworthÎncă nu există evaluări

- 2014 Deepa Puthran Forecasting Global Turbocharger Market A Mixed Method ApproachDocument5 pagini2014 Deepa Puthran Forecasting Global Turbocharger Market A Mixed Method ApproachShiv PrasadÎncă nu există evaluări

- HCMF Investor Letter October 2009 FINALDocument24 paginiHCMF Investor Letter October 2009 FINALAbsolute Return100% (1)

- Absensi Juli 2023Document3 paginiAbsensi Juli 2023Pira YuniarÎncă nu există evaluări

- Solr and Lucene Search RevolutionDocument27 paginiSolr and Lucene Search RevolutionErvin MillerÎncă nu există evaluări

- PvsystDocument44 paginiPvsystSgfvv100% (1)

- Special Section 1Document3 paginiSpecial Section 1M.A. ShaikhÎncă nu există evaluări

- Pew Research Center - Americans Fault China - 20200730Document26 paginiPew Research Center - Americans Fault China - 20200730bearsqÎncă nu există evaluări

- Harvard Kennedy - ASH Center - Understanding CCP Resilience - July2020Document18 paginiHarvard Kennedy - ASH Center - Understanding CCP Resilience - July2020bearsqÎncă nu există evaluări

- CME - Understanding FX Futures PDFDocument15 paginiCME - Understanding FX Futures PDFbearsqÎncă nu există evaluări

- Overview of Non-Deliverable Foreign Exchange Forward MarketsDocument6 paginiOverview of Non-Deliverable Foreign Exchange Forward MarketsRoland YauÎncă nu există evaluări

- Global Wealth Report 2019Document64 paginiGlobal Wealth Report 2019Jennifer NilleÎncă nu există evaluări

- ICE CDS White PaperDocument21 paginiICE CDS White PaperRajat SharmaÎncă nu există evaluări

- GICS Sector Classification HandbookDocument26 paginiGICS Sector Classification HandbookAndrewÎncă nu există evaluări

- CreditSuisse Bulletin - The New Asia - 2017Document76 paginiCreditSuisse Bulletin - The New Asia - 2017bearsqÎncă nu există evaluări

- CME - Currency Risk in Equity Portfolios PDFDocument8 paginiCME - Currency Risk in Equity Portfolios PDFbearsqÎncă nu există evaluări

- CME - Trading China Exposure - Mar2016 PDFDocument8 paginiCME - Trading China Exposure - Mar2016 PDFbearsqÎncă nu există evaluări

- 28 Essential Keyboard Shortcuts For Microsoft EdgeDocument11 pagini28 Essential Keyboard Shortcuts For Microsoft EdgebearsqÎncă nu există evaluări

- Nomura Global Phoenix Autocallable FactsheetDocument4 paginiNomura Global Phoenix Autocallable FactsheetbearsqÎncă nu există evaluări

- A Traders Guide To FuturesDocument34 paginiA Traders Guide To FuturesAggelos KotsokolosÎncă nu există evaluări

- 101 ListDocument5 pagini101 ListPragyan ThapaÎncă nu există evaluări

- Essentials: Places To Visit and Dates To RememberDocument4 paginiEssentials: Places To Visit and Dates To RememberbearsqÎncă nu există evaluări

- Finding Nemo GuideDocument15 paginiFinding Nemo GuideYuguang ZhouÎncă nu există evaluări

- CME Emini Futures IntroductionDocument27 paginiCME Emini Futures IntroductionbearsqÎncă nu există evaluări

- Replicate Vix in SpreadsheetDocument12 paginiReplicate Vix in Spreadsheetbearsq0% (1)

- (NERA) Subprime and Synthetic CDOs 2010Document37 pagini(NERA) Subprime and Synthetic CDOs 2010bearsqÎncă nu există evaluări

- George Lane-Father of StochasticsDocument4 paginiGeorge Lane-Father of StochasticsbearsqÎncă nu există evaluări

- (Bank of America) Option Prices Imply A Dividend Yield - Examining Recent Trading in JPMDocument1 pagină(Bank of America) Option Prices Imply A Dividend Yield - Examining Recent Trading in JPMbhartia2512Încă nu există evaluări

- Asian Journal of Management Cases: Zainab Riaz, Lahore University of Management Sciences, PakistanDocument1 paginăAsian Journal of Management Cases: Zainab Riaz, Lahore University of Management Sciences, PakistanbhagavathamhÎncă nu există evaluări

- Investment Appraisal TechniquesDocument2 paginiInvestment Appraisal TechniquesKANAK KOKAREÎncă nu există evaluări

- 2023 Q4 Multifamily Houston Report ColliersDocument4 pagini2023 Q4 Multifamily Houston Report ColliersKevin ParkerÎncă nu există evaluări

- Bangladesh Development ModelDocument59 paginiBangladesh Development ModelÑìtíñ PràkáshÎncă nu există evaluări

- Cement ProjectDocument66 paginiCement Projectmesfin esheteÎncă nu există evaluări

- Municipality of San Clemente - Citizens CharterDocument155 paginiMunicipality of San Clemente - Citizens CharterFree FlixnetÎncă nu există evaluări

- A211 Silibus Pelajar BPME3043Document5 paginiA211 Silibus Pelajar BPME3043yukeyÎncă nu există evaluări

- Economic OptimizationDocument11 paginiEconomic OptimizationCasillar, Irish Joy100% (1)

- Calculating conversion values and bond prices of convertible bondsDocument2 paginiCalculating conversion values and bond prices of convertible bondsDebarnob SarkarÎncă nu există evaluări

- Delaware Court Ruling on LLC Development DisputeDocument9 paginiDelaware Court Ruling on LLC Development Disputehancee tamboboyÎncă nu există evaluări

- M05 Gitman50803X 14 MF C05Document61 paginiM05 Gitman50803X 14 MF C05layan123456Încă nu există evaluări

- Pressure Vessel Inspection and Test Plan Sample: WWW - Inspection-For-Industry.c OmDocument4 paginiPressure Vessel Inspection and Test Plan Sample: WWW - Inspection-For-Industry.c OmMuh FarhanÎncă nu există evaluări

- Banking Manuals and Disciplinary ProceduresDocument8 paginiBanking Manuals and Disciplinary ProceduresGAGAN ANANDÎncă nu există evaluări

- Slide 4: Customer Relationship Management (CRM)Document3 paginiSlide 4: Customer Relationship Management (CRM)1921 Priyam PrakashÎncă nu există evaluări

- TCHE 303 - Money and Banking Tutorial QuestionsDocument2 paginiTCHE 303 - Money and Banking Tutorial QuestionsTường ThuậtÎncă nu există evaluări

- Group 2 - Sattve E TechDocument12 paginiGroup 2 - Sattve E TechMohanapriya JayakumarÎncă nu există evaluări

- Acm PDFDocument29 paginiAcm PDFJoule974Încă nu există evaluări

- Islamic Marketing: Strategy For Marketing Islamic Agro Products in Islamic Banking Institutions in MalaysiaDocument25 paginiIslamic Marketing: Strategy For Marketing Islamic Agro Products in Islamic Banking Institutions in MalaysiaMuhammad Ridhwan Ab. Aziz50% (2)

- Kadapa 1Document12 paginiKadapa 1Turumella VasuÎncă nu există evaluări

- The Omnichannel Value Proposition: An Ris News WhitepaperDocument7 paginiThe Omnichannel Value Proposition: An Ris News WhitepaperEric DesportesÎncă nu există evaluări

- Starkraft Presentation 2019Document37 paginiStarkraft Presentation 2019Liestia NoorÎncă nu există evaluări

- History of PartnershipsDocument2 paginiHistory of PartnershipsFox MacalinoÎncă nu există evaluări

- STTP - Slot 3 - Schedule PDFDocument1 paginăSTTP - Slot 3 - Schedule PDFshyam parakhiyaÎncă nu există evaluări

- Business Letters + ExercisesDocument8 paginiBusiness Letters + ExercisesBeatrice TeglasÎncă nu există evaluări

- Former Leitrim Hockey Association President Apologizes For Forging ChequesDocument3 paginiFormer Leitrim Hockey Association President Apologizes For Forging ChequesZahra RaheelÎncă nu există evaluări

- Front Page On Challenges and Prospects of Hotel Industries in IlaroDocument4 paginiFront Page On Challenges and Prospects of Hotel Industries in IlaropeterÎncă nu există evaluări

- BacklogDocument8 paginiBacklogamitdesai92Încă nu există evaluări

- Assignment Acn202 Number 13Document10 paginiAssignment Acn202 Number 13Nadil HaqueÎncă nu există evaluări

- OSMEÑA v. ORBOS, G.R. No. 99886, March 31, 1993Document9 paginiOSMEÑA v. ORBOS, G.R. No. 99886, March 31, 1993DodongÎncă nu există evaluări

- Woven Capital Associate ChallengeDocument2 paginiWoven Capital Associate ChallengeHaruka TakamoriÎncă nu există evaluări

- Value: The Four Cornerstones of Corporate FinanceDe la EverandValue: The Four Cornerstones of Corporate FinanceEvaluare: 4.5 din 5 stele4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- Joy of Agility: How to Solve Problems and Succeed SoonerDe la EverandJoy of Agility: How to Solve Problems and Succeed SoonerEvaluare: 4 din 5 stele4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000De la EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Evaluare: 4.5 din 5 stele4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 4.5 din 5 stele4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistDe la EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistEvaluare: 4.5 din 5 stele4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfDe la EverandProduct-Led Growth: How to Build a Product That Sells ItselfEvaluare: 5 din 5 stele5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe la EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanEvaluare: 4.5 din 5 stele4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsDe la EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsÎncă nu există evaluări

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisDe la EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisEvaluare: 5 din 5 stele5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)De la EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Evaluare: 4.5 din 5 stele4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialÎncă nu există evaluări

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityDe la EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityEvaluare: 4.5 din 5 stele4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualDe la EverandNote Brokering for Profit: Your Complete Work At Home Success ManualÎncă nu există evaluări

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursDe la EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursEvaluare: 4.5 din 5 stele4.5/5 (34)

- Connected Planning: A Playbook for Agile Decision MakingDe la EverandConnected Planning: A Playbook for Agile Decision MakingÎncă nu există evaluări

- Financial Risk Management: A Simple IntroductionDe la EverandFinancial Risk Management: A Simple IntroductionEvaluare: 4.5 din 5 stele4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNDe la Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNEvaluare: 4.5 din 5 stele4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaDe la EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaEvaluare: 3.5 din 5 stele3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthDe la EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthÎncă nu există evaluări

- Strategic Value Chain Analysis for Investors and ManagersDe la EverandStrategic Value Chain Analysis for Investors and ManagersÎncă nu există evaluări

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorDe la EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorÎncă nu există evaluări

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingDe la EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingEvaluare: 4.5 din 5 stele4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionDe la EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionEvaluare: 5 din 5 stele5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialDe la EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialEvaluare: 4.5 din 5 stele4.5/5 (32)