S-ar putea să vă placă și

- 99 Percent of What I Learned From Tony RobbinsDocument7 pagini99 Percent of What I Learned From Tony Robbinsngdaniel1302996% (24)

- Land Trust AgreementDocument11 paginiLand Trust Agreementchadhp92% (12)

- Opening The Third EyeDocument13 paginiOpening The Third EyekakamacgregorÎncă nu există evaluări

- The Complete Mentoring Program Toolkit 1Document26 paginiThe Complete Mentoring Program Toolkit 1ngdaniel13029Încă nu există evaluări

- Bitcoin Manifesto - Satoshi NakamotoDocument9 paginiBitcoin Manifesto - Satoshi NakamotoJessica Vu100% (1)

- LOMA FLMI CoursesDocument4 paginiLOMA FLMI CoursesCeleste Joy C. LinsanganÎncă nu există evaluări

- BofA - FX Quant Signals For The FOMC and ECB 20230130Document9 paginiBofA - FX Quant Signals For The FOMC and ECB 20230130G.Trading.FxÎncă nu există evaluări

- VISCOLAM202 D20 Acrylic 20 Thickeners 202017Document33 paginiVISCOLAM202 D20 Acrylic 20 Thickeners 202017Oswaldo Manuel Ramirez MarinÎncă nu există evaluări

- 2008 DB Fixed Income Outlook (12!14!07)Document107 pagini2008 DB Fixed Income Outlook (12!14!07)STÎncă nu există evaluări

- DLP in EmpowermentDocument13 paginiDLP in EmpowermentTek Casonete100% (1)

- Global - Macro - Weekly - 8 March 2019 PDFDocument60 paginiGlobal - Macro - Weekly - 8 March 2019 PDFchaotic_pandemoniumÎncă nu există evaluări

- Barclays FX Weekly Brief 20100902Document18 paginiBarclays FX Weekly Brief 20100902aaronandmosesllcÎncă nu există evaluări

- BNP FX WeeklyDocument22 paginiBNP FX WeeklyPhillip HsiaÎncă nu există evaluări

- FX Insight eDocument16 paginiFX Insight esilver lauÎncă nu există evaluări

- Weekly FX Insight: Citibank Wealth ManagementDocument16 paginiWeekly FX Insight: Citibank Wealth ManagementPopeye AlexÎncă nu există evaluări

- Citiinsight PDFDocument16 paginiCitiinsight PDFPopeye AlexÎncă nu există evaluări

- FX Insight e PDFDocument16 paginiFX Insight e PDFPopeye AlexÎncă nu există evaluări

- FX Insifddggfght e PDFDocument16 paginiFX Insifddggfght e PDFPopeye AlexÎncă nu există evaluări

- FX Insight e PDFDocument15 paginiFX Insight e PDFLeandro GuimaraesÎncă nu există evaluări

- FX Insight eDocument15 paginiFX Insight eBoris BonkoungouÎncă nu există evaluări

- Weekly FX Insight: Citibank Wealth ManagementDocument13 paginiWeekly FX Insight: Citibank Wealth ManagementtrinugrohoÎncă nu există evaluări

- FX TacticalsDocument6 paginiFX TacticalsodinÎncă nu există evaluări

- Fed To Eventually Remove The Punch Bowl: Global FX WeeklyDocument28 paginiFed To Eventually Remove The Punch Bowl: Global FX Weeklygerrich rusÎncă nu există evaluări

- 23 Feb 2024 FridayDocument13 pagini23 Feb 2024 FridaytanmaymaltarÎncă nu există evaluări

- 26 Feb 2024 MondayDocument17 pagini26 Feb 2024 MondaytanmaymaltarÎncă nu există evaluări

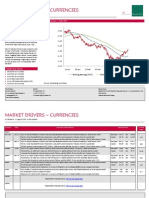

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- JYSKE Bank AUG 09 Market Drivers CurrenciesDocument5 paginiJYSKE Bank AUG 09 Market Drivers CurrenciesMiir ViirÎncă nu există evaluări

- Weekly FX Insight: Citibank Wealth ManagementDocument14 paginiWeekly FX Insight: Citibank Wealth ManagementBasilÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Macro Trade Pitch Individual Presentation: Steven Li Phi Gamma Nu New MemberDocument14 paginiMacro Trade Pitch Individual Presentation: Steven Li Phi Gamma Nu New MemberSteven LiÎncă nu există evaluări

- FX Daily: High Bar To Reverse The Dollar Bear TrendDocument3 paginiFX Daily: High Bar To Reverse The Dollar Bear Trenddbr trackdÎncă nu există evaluări

- Global FX StrategyDocument4 paginiGlobal FX StrategyllaryÎncă nu există evaluări

- Change of Year, Change of Course: FX Themes and Trades Monthly OutlookDocument15 paginiChange of Year, Change of Course: FX Themes and Trades Monthly OutlookJustinC.PaoliniÎncă nu există evaluări

- ING Think FX Daily Patient Rba Remains A Secondary Driver For AudDocument4 paginiING Think FX Daily Patient Rba Remains A Secondary Driver For AudzushiiiÎncă nu există evaluări

- FX Insight eDocument16 paginiFX Insight ePopeye AlexÎncă nu există evaluări

- Citi InsightDocument16 paginiCiti InsightPopeye AlexÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Insights DeerDocument6 paginiInsights Deernathory68Încă nu există evaluări

- Dailyfx Guide en 2024 q1 JpyDocument7 paginiDailyfx Guide en 2024 q1 JpyboubaÎncă nu există evaluări

- DBS Flash: Asia Rates: Flows, Positioning & Valuation (June 2022)Document10 paginiDBS Flash: Asia Rates: Flows, Positioning & Valuation (June 2022)AdamZawÎncă nu există evaluări

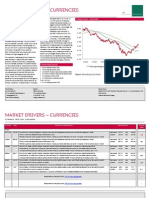

- Market Drivers - Currencies: Today's Comment Today's Chart - PMI Manufacturing & PMI Service (Euro Zone)Document5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - PMI Manufacturing & PMI Service (Euro Zone)Miir ViirÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Weekly FX Insight: Citibank Wealth ManagementDocument14 paginiWeekly FX Insight: Citibank Wealth Managementngdaniel13029Încă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/JPYDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/JPYMiir ViirÎncă nu există evaluări

- G10 FX Week Ahead: Tailgating Treasury YieldsDocument8 paginiG10 FX Week Ahead: Tailgating Treasury YieldsrockieballÎncă nu există evaluări

- Bank of Japan NotesDocument7 paginiBank of Japan NotesLudvig Timo HyttinenÎncă nu există evaluări

- HDFC Asset Management Company LimitedDocument8 paginiHDFC Asset Management Company LimitedankurbbhattÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Outlook 1er Semestre 2023Document8 paginiOutlook 1er Semestre 2023CCV CCVÎncă nu există evaluări

- CACIB - FX Daily 20230712Document4 paginiCACIB - FX Daily 20230712martinlukas950Încă nu există evaluări

- Global FX StrategyDocument3 paginiGlobal FX Strategyashish pandeyÎncă nu există evaluări

- Urrency Forecast: $ Continued To Weaken Vs Other Major CurrenciesDocument4 paginiUrrency Forecast: $ Continued To Weaken Vs Other Major CurrenciesprinceasatiÎncă nu există evaluări

- Global FX StrategyDocument3 paginiGlobal FX StrategyrockieballÎncă nu există evaluări

- UBS CIO Monthly Base en Oct 2019Document17 paginiUBS CIO Monthly Base en Oct 2019Blue RunnerÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/USDDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/USDMiir ViirÎncă nu există evaluări

- Top Trading OpportunitiesDocument25 paginiTop Trading Opportunitiestanyan.huangÎncă nu există evaluări

- Top Trading Opportunities 2017Document35 paginiTop Trading Opportunities 2017Max KennedyÎncă nu există evaluări

- Monthly Outlook GoldDocument10 paginiMonthly Outlook GoldKapil KhandelwalÎncă nu există evaluări

- Market Drivers - Currencies: Today's Comment Today's Chart - EUR/CHFDocument5 paginiMarket Drivers - Currencies: Today's Comment Today's Chart - EUR/CHFMiir ViirÎncă nu există evaluări

- Top Trading Opportunities FOR 2021: Dailyfx Research TeamDocument38 paginiTop Trading Opportunities FOR 2021: Dailyfx Research TeamKgoadi KgÎncă nu există evaluări

- Daily FX Update: Europe Provides Offset To Worrisome China PmiDocument3 paginiDaily FX Update: Europe Provides Offset To Worrisome China PmiMohd Sofian YusoffÎncă nu există evaluări

- ScotiaBank AUG 03 Daily FX UpdateDocument3 paginiScotiaBank AUG 03 Daily FX UpdateMiir ViirÎncă nu există evaluări

- CIO Monthly Base enDocument18 paginiCIO Monthly Base enoana_avramÎncă nu există evaluări

- NMFMS - Daily Market Analysis - 10th Jan (Wed)Document14 paginiNMFMS - Daily Market Analysis - 10th Jan (Wed)williamrmahasoaÎncă nu există evaluări

- Daily FX Update: Eur Limited by Fibo LevelsDocument3 paginiDaily FX Update: Eur Limited by Fibo LevelsBasil Baby-PisharathuÎncă nu există evaluări

- BCA - Gis So 2014 12 12 PDFDocument32 paginiBCA - Gis So 2014 12 12 PDFJBÎncă nu există evaluări

- Weekly FX Insight: Citibank Wealth ManagementDocument14 paginiWeekly FX Insight: Citibank Wealth Managementngdaniel13029Încă nu există evaluări

- SPX Monthly Chart: August 23, 2020 EditionDocument7 paginiSPX Monthly Chart: August 23, 2020 Editionngdaniel13029Încă nu există evaluări

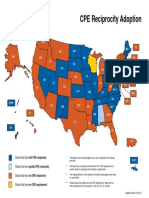

- Cpe Reciprocity MapDocument1 paginăCpe Reciprocity Mapngdaniel13029Încă nu există evaluări

- MUA CatalogDocument44 paginiMUA Catalogngdaniel13029Încă nu există evaluări

- Limited Liability Company (LLC) Cancellation Requirements - What Form To FileDocument8 paginiLimited Liability Company (LLC) Cancellation Requirements - What Form To Filengdaniel130290% (1)

- Becoming A Dog TrainerDocument6 paginiBecoming A Dog Trainerngdaniel13029Încă nu există evaluări

- 04 10 ALINT DatasheetDocument2 pagini04 10 ALINT DatasheetJoakim LangletÎncă nu există evaluări

- Jose André Morales, PH.D.: Ingeniería SocialDocument56 paginiJose André Morales, PH.D.: Ingeniería SocialJYMYÎncă nu există evaluări

- English ExerciseDocument2 paginiEnglish ExercisePankhuri Agarwal100% (1)

- Finite Element Method For Eigenvalue Problems in ElectromagneticsDocument38 paginiFinite Element Method For Eigenvalue Problems in ElectromagneticsBhargav BikkaniÎncă nu există evaluări

- Wilson v. Baker Hughes Et. Al.Document10 paginiWilson v. Baker Hughes Et. Al.Patent LitigationÎncă nu există evaluări

- 0apageo Catalogue Uk 2022Document144 pagini0apageo Catalogue Uk 2022Kouassi JaurèsÎncă nu există evaluări

- Glossario - GETTY - IngDocument24 paginiGlossario - GETTY - IngFabio ZarattiniÎncă nu există evaluări

- Repro Indo China Conf PDFDocument16 paginiRepro Indo China Conf PDFPavit KaurÎncă nu există evaluări

- Chapter 1Document20 paginiChapter 1Li YuÎncă nu există evaluări

- AppendixA LaplaceDocument12 paginiAppendixA LaplaceSunny SunÎncă nu există evaluări

- Multidimensional Scaling Groenen Velden 2004 PDFDocument14 paginiMultidimensional Scaling Groenen Velden 2004 PDFjoséÎncă nu există evaluări

- Lesson Plan Outline - Rebounding - Perez - JoseDocument7 paginiLesson Plan Outline - Rebounding - Perez - JoseJose PerezÎncă nu există evaluări

- Unknown 31Document40 paginiUnknown 31Tina TinaÎncă nu există evaluări

- PhysioEx Exercise 1 Activity 1Document3 paginiPhysioEx Exercise 1 Activity 1edvin merida proÎncă nu există evaluări

- Teacher Resource Disc: Betty Schrampfer Azar Stacy A. HagenDocument10 paginiTeacher Resource Disc: Betty Schrampfer Azar Stacy A. HagenRaveli pieceÎncă nu există evaluări

- Applications of Remote Sensing and Gis For UrbanDocument47 paginiApplications of Remote Sensing and Gis For UrbanKashan Ali KhanÎncă nu există evaluări

- Red Hat Ceph Storage-1.2.3-Ceph Configuration Guide-en-US PDFDocument127 paginiRed Hat Ceph Storage-1.2.3-Ceph Configuration Guide-en-US PDFJony NguyễnÎncă nu există evaluări

- Atmosphere Study Guide 2013Document4 paginiAtmosphere Study Guide 2013api-205313794Încă nu există evaluări

- Business Maths Chapter 5Document9 paginiBusiness Maths Chapter 5鄭仲抗Încă nu există evaluări

- Kharrat Et Al., 2007 (Energy - Fuels)Document4 paginiKharrat Et Al., 2007 (Energy - Fuels)Leticia SakaiÎncă nu există evaluări

- International Beach Soccer Cup Bali 2023 October 4-7 - Ver 15-3-2023 - Sponsor UPDATED PDFDocument23 paginiInternational Beach Soccer Cup Bali 2023 October 4-7 - Ver 15-3-2023 - Sponsor UPDATED PDFPrincess Jasmine100% (1)

- InfltiDocument13 paginiInfltiLEKH021Încă nu există evaluări

- NS1 UserManual EN V1.2Document31 paginiNS1 UserManual EN V1.2T5 TecnologiaÎncă nu există evaluări

- Med Error PaperDocument4 paginiMed Error Paperapi-314062228100% (1)

- Aggregate Production PlanningDocument5 paginiAggregate Production PlanningSarbani SahuÎncă nu există evaluări

- 15-3-2020 Chapter 4 Forward Kinematics Lecture 1Document29 pagini15-3-2020 Chapter 4 Forward Kinematics Lecture 1MoathÎncă nu există evaluări