S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- ESigned TVSCS PL ApplicationDocument13 paginiESigned TVSCS PL ApplicationSATHISH KUMARÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Contoh Surat TawaranDocument4 paginiContoh Surat TawaranAmir UmarÎncă nu există evaluări

- CAIIB-Retail Banking-Short Notes by Murugan-Sep 2021Document74 paginiCAIIB-Retail Banking-Short Notes by Murugan-Sep 2021Divya SinghÎncă nu există evaluări

- Unit II Assessment Financial System and Financial MarketDocument9 paginiUnit II Assessment Financial System and Financial MarketMICHAEL DIPUTADO100% (2)

- Internal Control: Distinguish Between Floor Limit & House LimitDocument3 paginiInternal Control: Distinguish Between Floor Limit & House Limitsoundarya ReddyÎncă nu există evaluări

- Cash & GB MCQ NEW ESKATON FDocument18 paginiCash & GB MCQ NEW ESKATON FJubaida Alam Juthy57% (7)

- NOTES Onthe Bank Secrecy Law (RA1405)Document9 paginiNOTES Onthe Bank Secrecy Law (RA1405)edrianclydeÎncă nu există evaluări

- The Analysis of The Financial Market or Institution For Air Asia AirlinesDocument21 paginiThe Analysis of The Financial Market or Institution For Air Asia AirlinesIeyrah Rah ElisyaÎncă nu există evaluări

- The Analysis of The Financial Market or Institution For Air Asia AirlinesDocument21 paginiThe Analysis of The Financial Market or Institution For Air Asia AirlinesIeyrah Rah ElisyaÎncă nu există evaluări

- The Analysis of The Financial Market or Institution For Air Asia AirlinesDocument21 paginiThe Analysis of The Financial Market or Institution For Air Asia AirlinesIeyrah Rah ElisyaÎncă nu există evaluări

- Possibility of standardizing Islamic banks' products globallyDocument3 paginiPossibility of standardizing Islamic banks' products globallyIeyrah Rah ElisyaÎncă nu există evaluări

- Waqf Article ReviewDocument8 paginiWaqf Article ReviewIeyrah Rah Elisya100% (1)

- Report Case Study Macroeconomics PDFDocument17 paginiReport Case Study Macroeconomics PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Andi Nur Elisya Syahira Binti Bahri AIU18092007 Malaysian Sukuk: MurabahahDocument2 paginiAndi Nur Elisya Syahira Binti Bahri AIU18092007 Malaysian Sukuk: MurabahahIeyrah Rah ElisyaÎncă nu există evaluări

- Presentation LiteracyDocument4 paginiPresentation LiteracyIeyrah Rah ElisyaÎncă nu există evaluări

- (I) Mission, Vision and Core Values VisionDocument1 pagină(I) Mission, Vision and Core Values VisionIeyrah Rah ElisyaÎncă nu există evaluări

- Presentation LiteracyDocument4 paginiPresentation LiteracyIeyrah Rah ElisyaÎncă nu există evaluări

- Time Management Among AIU StudentsDocument30 paginiTime Management Among AIU StudentsIeyrah Rah ElisyaÎncă nu există evaluări

- Presentation LiteracyDocument4 paginiPresentation LiteracyIeyrah Rah ElisyaÎncă nu există evaluări

- Toturial 11 Assignment PDFDocument4 paginiToturial 11 Assignment PDFIeyrah Rah ElisyaÎncă nu există evaluări

- (I) Mission, Vision and Core Values VisionDocument16 pagini(I) Mission, Vision and Core Values VisionIeyrah Rah ElisyaÎncă nu există evaluări

- (I) Mission, Vision and Core Values VisionDocument16 pagini(I) Mission, Vision and Core Values VisionIeyrah Rah ElisyaÎncă nu există evaluări

- Case Study FP PDFDocument6 paginiCase Study FP PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Bursa Malaysia Report PDFDocument9 paginiBursa Malaysia Report PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Written Executive Summary PDFDocument7 paginiWritten Executive Summary PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Examining the complex relationship between China and Africa in "When China Met AfricaDocument3 paginiExamining the complex relationship between China and Africa in "When China Met AfricaIeyrah Rah ElisyaÎncă nu există evaluări

- Case Study FP PDFDocument6 paginiCase Study FP PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Assignment 4Document10 paginiAssignment 4Ieyrah Rah ElisyaÎncă nu există evaluări

- Difference between colonialism and imperialismDocument2 paginiDifference between colonialism and imperialismIeyrah Rah ElisyaÎncă nu există evaluări

- Final Exam AnswerDocument10 paginiFinal Exam AnswerIeyrah Rah ElisyaÎncă nu există evaluări

- Individual AssignmentDocument5 paginiIndividual AssignmentIeyrah Rah ElisyaÎncă nu există evaluări

- Riba PDFDocument1 paginăRiba PDFIeyrah Rah ElisyaÎncă nu există evaluări

- Class Preparation Week 1Document1 paginăClass Preparation Week 1Ieyrah Rah ElisyaÎncă nu există evaluări

- Islamic Banking AnswerDocument2 paginiIslamic Banking AnswerIeyrah Rah ElisyaÎncă nu există evaluări

- History and IdentityDocument2 paginiHistory and IdentityMuhammad SalehuddinÎncă nu există evaluări

- The Peace ImperativeDocument3 paginiThe Peace ImperativeIeyrah Rah ElisyaÎncă nu există evaluări

- Assignment 3 (Ayush Jain)Document5 paginiAssignment 3 (Ayush Jain)Abhijeet JainÎncă nu există evaluări

- AccountingDocument13 paginiAccountingFarrukhsgÎncă nu există evaluări

- 4AC0 01 Que 20150107Document20 pagini4AC0 01 Que 20150107anupama dissanaykeÎncă nu există evaluări

- Bashir-UCP Art1, Trade PaymentDocument89 paginiBashir-UCP Art1, Trade PaymentMasud Khan ShakilÎncă nu există evaluări

- Retailing ConceptsDocument5 paginiRetailing Conceptsbeena antuÎncă nu există evaluări

- MCQs - RatiosDocument9 paginiMCQs - RatiosLalitÎncă nu există evaluări

- Calculating Profit and LossDocument8 paginiCalculating Profit and Lossramana3339Încă nu există evaluări

- The Impact of E-Banking On Customer Satisfaction: Evidence From Banking Sector of PakistanDocument15 paginiThe Impact of E-Banking On Customer Satisfaction: Evidence From Banking Sector of PakistanEraj RehanÎncă nu există evaluări

- Midterm Exam Intermediate Accounting 1Document9 paginiMidterm Exam Intermediate Accounting 111-C2 Dennise EscobidoÎncă nu există evaluări

- Audit 2Document6 paginiAudit 2Frances Mikayla EnriquezÎncă nu există evaluări

- Internship Report MMBLDocument23 paginiInternship Report MMBLKhizir Mohammad Julkifil MuheetÎncă nu există evaluări

- Blank Medical Invoice TemplateDocument2 paginiBlank Medical Invoice Templatemiranda criggerÎncă nu există evaluări

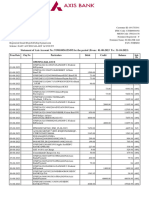

- Statement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)Document5 paginiStatement of Axis Account No:919010056153495 For The Period (From: 01-08-2023 To: 31-10-2023)pooja.acharyaÎncă nu există evaluări

- Bond Valuation Case SolutionDocument7 paginiBond Valuation Case SolutiongeorgeÎncă nu există evaluări

- Investment Analysis & Portfolio ManagementDocument22 paginiInvestment Analysis & Portfolio ManagementJyoti YadavÎncă nu există evaluări

- New Central Bank Act - Usec YebraDocument9 paginiNew Central Bank Act - Usec YebragieeÎncă nu există evaluări

- Chapter 4 Interest RatesDocument4 paginiChapter 4 Interest Ratessamrawithagos2002Încă nu există evaluări

- Uplive Basic Policy With Detail NEW August 2022Document4 paginiUplive Basic Policy With Detail NEW August 2022just crizÎncă nu există evaluări

- Kindly Execute The Following Request/sDocument2 paginiKindly Execute The Following Request/sAxtella Global for Information Technology CompanyqÎncă nu există evaluări

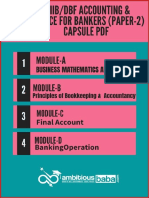

- JAIJAIIB Paper 2 CAPSULE PDF 2.O Accounting Finance For Bankers by Ambitious BabaDocument159 paginiJAIJAIIB Paper 2 CAPSULE PDF 2.O Accounting Finance For Bankers by Ambitious BabaSaurabhÎncă nu există evaluări

- Financial Liberalization and Stock Market VolatilityDocument46 paginiFinancial Liberalization and Stock Market VolatilityazeemÎncă nu există evaluări

- BI Stock PortfolioDocument100 paginiBI Stock PortfoliobayuÎncă nu există evaluări

- The Economics of Money, Banking, and Financial Markets: Twelfth Edition, Global EditionDocument62 paginiThe Economics of Money, Banking, and Financial Markets: Twelfth Edition, Global Editionsawmon myintÎncă nu există evaluări