S-ar putea să vă placă și

- How to Invest in Gold: A guide to making money (or securing wealth) by buying and selling goldDe la EverandHow to Invest in Gold: A guide to making money (or securing wealth) by buying and selling goldEvaluare: 3 din 5 stele3/5 (1)

- Gold As An InvestmentDocument15 paginiGold As An InvestmentSruthi Raveendran100% (1)

- The Silver Bull Market: Investing in the Other GoldDe la EverandThe Silver Bull Market: Investing in the Other GoldÎncă nu există evaluări

- Gold AmanDocument9 paginiGold AmanRishi DhallÎncă nu există evaluări

- The Changing Role of Gold Within the Global Financial ArchictectureDe la EverandThe Changing Role of Gold Within the Global Financial ArchictectureÎncă nu există evaluări

- GoldDocument25 paginiGoldarun1417100% (1)

- Intelligent Gold Investing: Including a section on BitcoinDe la EverandIntelligent Gold Investing: Including a section on BitcoinÎncă nu există evaluări

- Final Copy of Chapters.Document90 paginiFinal Copy of Chapters.skc111Încă nu există evaluări

- A Project On Factors Affecting Changes in Gold Prices: Submitted By: Submitted ToDocument13 paginiA Project On Factors Affecting Changes in Gold Prices: Submitted By: Submitted Toshubhamagrawal_88Încă nu există evaluări

- Trading GoldDocument5 paginiTrading GoldLeonard NgÎncă nu există evaluări

- Gold Market Us PDFDocument60 paginiGold Market Us PDFMohan RajÎncă nu există evaluări

- Gold ResearcherDocument84 paginiGold ResearchergoldresearcherÎncă nu există evaluări

- GoldDocument21 paginiGoldSonal KothariÎncă nu există evaluări

- World Goldreport 2010Document48 paginiWorld Goldreport 2010Tran Anh QuangÎncă nu există evaluări

- Gold Store of ValueDocument9 paginiGold Store of ValueHarshitha DammuÎncă nu există evaluări

- HASAN 09213521 (IF-cw2)Document12 paginiHASAN 09213521 (IF-cw2)Mahmudul HasanÎncă nu există evaluări

- The Truth About GoldDocument59 paginiThe Truth About GoldEric Platt100% (2)

- Reasons To BuyDocument1 paginăReasons To BuythiscoinsuxxÎncă nu există evaluări

- Gold Prices FluctuationsDocument6 paginiGold Prices Fluctuationskuldeep_chand10Încă nu există evaluări

- Precious Metals & Rare Coins For Investors and CollectorsDocument65 paginiPrecious Metals & Rare Coins For Investors and CollectorsRalow Lawson100% (1)

- Gold and Gold Investments: Example XVI.1Document15 paginiGold and Gold Investments: Example XVI.1kilowatt2point0Încă nu există evaluări

- Gold InvestmentDocument4 paginiGold InvestmentvinitclairÎncă nu există evaluări

- 2009 Winter Warning Volume 10 Issue 1Document6 pagini2009 Winter Warning Volume 10 Issue 1stevens106Încă nu există evaluări

- Gold Bear Market (1980-2001) : Gold Prices Ran Into A 20 Year Long Bear Market FromDocument6 paginiGold Bear Market (1980-2001) : Gold Prices Ran Into A 20 Year Long Bear Market FrommadhurÎncă nu există evaluări

- Dow Gold RatioDocument21 paginiDow Gold RatioPrimo KUSHFUTURES™ M©QUEENÎncă nu există evaluări

- Petrodollar & Gold - Ver17Document80 paginiPetrodollar & Gold - Ver17Hend HelmyÎncă nu există evaluări

- A Year Performance of Present Gold Trading ContractDocument27 paginiA Year Performance of Present Gold Trading Contractbalki123Încă nu există evaluări

- Module 2 - Learning MaterialDocument19 paginiModule 2 - Learning MaterialMICHELLE MILANAÎncă nu există evaluări

- Gold Standard PresentationDocument23 paginiGold Standard PresentationVijay Kumar VasamÎncă nu există evaluări

- Self Study 2Document48 paginiSelf Study 2siyammbaÎncă nu există evaluări

- Gold Gold Etf HDFC BankDocument27 paginiGold Gold Etf HDFC BankAakash SaxenaÎncă nu există evaluări

- 1gold Report PDFDocument86 pagini1gold Report PDFrahul84803Încă nu există evaluări

- Bullion Market PPPDocument24 paginiBullion Market PPPIndu PrakashÎncă nu există evaluări

- Monetary System Module 2Document102 paginiMonetary System Module 2Tarak MehtaÎncă nu există evaluări

- "Essentials of Baking and Finance ": US Dollar & Crude OilDocument9 pagini"Essentials of Baking and Finance ": US Dollar & Crude Oilejaz_balti_1Încă nu există evaluări

- Unit 9 - Exchange Rate KeyDocument7 paginiUnit 9 - Exchange Rate KeyBò SữaÎncă nu există evaluări

- Silver Precious Metals Investment Money Store of Value Silver Standard Legal Tender Developed Countries United StatesDocument6 paginiSilver Precious Metals Investment Money Store of Value Silver Standard Legal Tender Developed Countries United StatesHardik GuptaÎncă nu există evaluări

- Industry Profile: (Type The Document Title)Document5 paginiIndustry Profile: (Type The Document Title)KumarKyÎncă nu există evaluări

- A Golden MulliganDocument14 paginiA Golden MulliganNick WeeksÎncă nu există evaluări

- Gold in The Investment Portfolio: Frankfurt School - Working PaperDocument50 paginiGold in The Investment Portfolio: Frankfurt School - Working PaperSharvani ChadalawadaÎncă nu există evaluări

- Past Pro.....Document11 paginiPast Pro.....Hitesh MattaÎncă nu există evaluări

- Lighthouse - Goldbug Galore - 2017-04Document11 paginiLighthouse - Goldbug Galore - 2017-04Alexander GloyÎncă nu există evaluări

- Presented By: Raveendhar.k Sathish Thalabow DiDocument24 paginiPresented By: Raveendhar.k Sathish Thalabow Diraveendhar.kÎncă nu există evaluări

- Gold Prices in IndiaDocument7 paginiGold Prices in IndiatechcaresystemÎncă nu există evaluări

- Gold's Irrational Price Movement: Understanding GoldDocument7 paginiGold's Irrational Price Movement: Understanding GoldNamrata KanodiaÎncă nu există evaluări

- Impact of Gold Prices On World EconomyDocument19 paginiImpact of Gold Prices On World EconomyGagan Preet Kaur100% (1)

- Gold As A Foreign Exchange Reserve of Central BanksDocument8 paginiGold As A Foreign Exchange Reserve of Central BanksMikiKikiÎncă nu există evaluări

- Part II: Gold Keeps Rising As Other Commodities FallDocument10 paginiPart II: Gold Keeps Rising As Other Commodities FallbengersonÎncă nu există evaluări

- BDNG 3103Document11 paginiBDNG 3103prithinahÎncă nu există evaluări

- GOLD BrochureDocument8 paginiGOLD BrochurelaxmiccÎncă nu există evaluări

- Introduction and MethodologyDocument3 paginiIntroduction and MethodologyJoshua JÎncă nu există evaluări

- Basics of Gold As An Investment ClassDocument6 paginiBasics of Gold As An Investment Classanandyadav_imgÎncă nu există evaluări

- Gold PricingDocument65 paginiGold Pricinggauravshetty2003Încă nu există evaluări

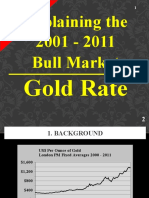

- Gold Rate - Explaining The Current Bull Market (2001 - )Document18 paginiGold Rate - Explaining The Current Bull Market (2001 - )Florian FisherÎncă nu există evaluări

- Gold Standard 1Document4 paginiGold Standard 1Hung Ngoc LeÎncă nu există evaluări

- Gold:Silk Road ReduxDocument5 paginiGold:Silk Road ReduxTim TruaxÎncă nu există evaluări

- NYU Presentation 11 17 10 v3 - 0Document48 paginiNYU Presentation 11 17 10 v3 - 0Kevin CreaseyÎncă nu există evaluări

- Bullion Market in IndiaDocument57 paginiBullion Market in IndiaVINAY MISHRA100% (1)

- Lesson10 Monetary Mechanisms HistoryDocument13 paginiLesson10 Monetary Mechanisms HistoryJAHONGIRÎncă nu există evaluări

- Latest Issue: Gold Demand Trends Q3 2012Document9 paginiLatest Issue: Gold Demand Trends Q3 2012Manish Jains JainsÎncă nu există evaluări

- Technical Glass ProductsDocument3 paginiTechnical Glass Productsmladen lakicÎncă nu există evaluări

- X-Ray Fluorescence - WikipediaDocument10 paginiX-Ray Fluorescence - Wikipediamladen lakicÎncă nu există evaluări

- Zone Refining. - Gold Refining ForumDocument4 paginiZone Refining. - Gold Refining Forummladen lakicÎncă nu există evaluări

- Method For Ultra High Purity Gold - Gold Refining ForumDocument11 paginiMethod For Ultra High Purity Gold - Gold Refining Forummladen lakic100% (1)

- DocCopper's Copper Electrorefining PageDocument2 paginiDocCopper's Copper Electrorefining Pagemladen lakicÎncă nu există evaluări

- GNS - E-Scrap Yield List v1.0Document13 paginiGNS - E-Scrap Yield List v1.0Gustavo Cabrera100% (1)

- Silver Chloride Dissolution in ARDocument5 paginiSilver Chloride Dissolution in ARAFLAC ............Încă nu există evaluări

- Gamma Energy (KeV)Document4 paginiGamma Energy (KeV)mladen lakicÎncă nu există evaluări

- Oxidations With Nickel Peroxide (NICL2 + NAOCL)Document5 paginiOxidations With Nickel Peroxide (NICL2 + NAOCL)mladen lakicÎncă nu există evaluări

- PFA Coating PFA Film - Teflon ™ PFADocument7 paginiPFA Coating PFA Film - Teflon ™ PFAmladen lakicÎncă nu există evaluări

- Dealing With WasteDocument6 paginiDealing With Wastemladen lakicÎncă nu există evaluări

- Dealing With WasteDocument6 paginiDealing With Wastemladen lakicÎncă nu există evaluări

- Review of Laser-Matter InteractionDocument29 paginiReview of Laser-Matter Interactionmladen lakicÎncă nu există evaluări

- TEMPO Catalyst SystemsDocument1 paginăTEMPO Catalyst Systemsmladen lakicÎncă nu există evaluări

- Torulaspora Delbrueckii and Conversion To Ephedrine byDocument4 paginiTorulaspora Delbrueckii and Conversion To Ephedrine bysalvia1025100% (1)

- Urushibara Nickel Eros - Ru003Document1 paginăUrushibara Nickel Eros - Ru003mladen lakic100% (1)

- Contrast Agents TutorialDocument32 paginiContrast Agents Tutorialmladen lakicÎncă nu există evaluări

- 4.1. Interaction Light-Matter 2-7-08Document10 pagini4.1. Interaction Light-Matter 2-7-08mladen lakicÎncă nu există evaluări

- Optics Communications: Shengli Pu, Min Dai, Guoqing SunDocument5 paginiOptics Communications: Shengli Pu, Min Dai, Guoqing Sunmladen lakicÎncă nu există evaluări

- Molecules 18 03206Document21 paginiMolecules 18 03206mladen lakicÎncă nu există evaluări

- Electronic Components - NoviteraDocument2 paginiElectronic Components - Noviteramladen lakicÎncă nu există evaluări

- Carbohydrates: Occurrence, Structures and Chemistry: Rieder IchtenthalerDocument30 paginiCarbohydrates: Occurrence, Structures and Chemistry: Rieder IchtenthalerAdriano Schindler Freire100% (1)

- Ball Mill Loading - Dry MillingDocument3 paginiBall Mill Loading - Dry Millingmladen lakicÎncă nu există evaluări

- Extraction of Silver From Waste X-Ray Films by Thiosulphate Leaching - IMPS2010-LibreDocument9 paginiExtraction of Silver From Waste X-Ray Films by Thiosulphate Leaching - IMPS2010-LibredorutzuÎncă nu există evaluări

- Recovery of Tin and CopperDocument9 paginiRecovery of Tin and Coppermladen lakicÎncă nu există evaluări

- Biocinjugate Chemistry Rad Sa KarbonilomDocument10 paginiBiocinjugate Chemistry Rad Sa Karbonilommladen lakicÎncă nu există evaluări

- 1 s2.0 S0304885311007256 MainDocument13 pagini1 s2.0 S0304885311007256 Mainmladen lakicÎncă nu există evaluări

- The Manufacture of Chemicals by ElectrolysisDocument92 paginiThe Manufacture of Chemicals by ElectrolysisJimÎncă nu există evaluări

- 04 Juten 19Document2 pagini04 Juten 19mladen lakicÎncă nu există evaluări

- $100M Leads: How to Get Strangers to Want to Buy Your StuffDe la Everand$100M Leads: How to Get Strangers to Want to Buy Your StuffEvaluare: 5 din 5 stele5/5 (18)

- Pattern Fitting and Alteration for Beginners: Fit and Alter Your Favorite Garments With ConfidenceDe la EverandPattern Fitting and Alteration for Beginners: Fit and Alter Your Favorite Garments With ConfidenceEvaluare: 3 din 5 stele3/5 (1)

- The Wire-Wrapped Jewelry Bible: Artistry Unveiled: Create Stunning Pieces, Master Techniques, and Ignite Your Passion | Include 30+ Wire-Wrapped Jewelry DIY ProjectsDe la EverandThe Wire-Wrapped Jewelry Bible: Artistry Unveiled: Create Stunning Pieces, Master Techniques, and Ignite Your Passion | Include 30+ Wire-Wrapped Jewelry DIY ProjectsÎncă nu există evaluări

- The Ultimate Cigar Book: 4th EditionDe la EverandThe Ultimate Cigar Book: 4th EditionEvaluare: 4.5 din 5 stele4.5/5 (2)

- The Existential Literature CollectionDe la EverandThe Existential Literature CollectionEvaluare: 2.5 din 5 stele2.5/5 (2)

- How to Trade Gold: Gold Trading Strategies That WorkDe la EverandHow to Trade Gold: Gold Trading Strategies That WorkEvaluare: 1 din 5 stele1/5 (1)

- I'd Rather Be Reading: A Library of Art for Book LoversDe la EverandI'd Rather Be Reading: A Library of Art for Book LoversEvaluare: 3.5 din 5 stele3.5/5 (57)

- The RVer's Bible (Revised and Updated): Everything You Need to Know About Choosing, Using, and Enjoying Your RVDe la EverandThe RVer's Bible (Revised and Updated): Everything You Need to Know About Choosing, Using, and Enjoying Your RVEvaluare: 5 din 5 stele5/5 (2)

- The Rape of the Mind: The Psychology of Thought Control, Menticide, and BrainwashingDe la EverandThe Rape of the Mind: The Psychology of Thought Control, Menticide, and BrainwashingEvaluare: 4 din 5 stele4/5 (23)

- SuppressorsDe la EverandSuppressorsEditors of RECOIL MagazineÎncă nu există evaluări

- Ceramics: Contemporary Artists Working in ClayDe la EverandCeramics: Contemporary Artists Working in ClayEvaluare: 5 din 5 stele5/5 (3)

- Book of Glock: A Comprehensive Guide to America's Most Popular HandgunDe la EverandBook of Glock: A Comprehensive Guide to America's Most Popular HandgunEvaluare: 5 din 5 stele5/5 (1)

- Indian Polity with Indian Constitution & Parliamentary AffairsDe la EverandIndian Polity with Indian Constitution & Parliamentary AffairsÎncă nu există evaluări

- Stoned: Jewelry, Obsession, and How Desire Shapes the WorldDe la EverandStoned: Jewelry, Obsession, and How Desire Shapes the WorldEvaluare: 3.5 din 5 stele3.5/5 (55)

- Wrist Watches Explained: How to fully appreciate one of the most complex machine ever inventedDe la EverandWrist Watches Explained: How to fully appreciate one of the most complex machine ever inventedEvaluare: 4.5 din 5 stele4.5/5 (3)

- Sports Card Collector 101: The Simplified Newbie's Guide to Start Collecting and Investing in Sports Cards in Less Than 7 Days: The Simplified Newbie's Guide to Start Collecting and Investing in Sport Cards in Less than 7 daysDe la EverandSports Card Collector 101: The Simplified Newbie's Guide to Start Collecting and Investing in Sports Cards in Less Than 7 Days: The Simplified Newbie's Guide to Start Collecting and Investing in Sport Cards in Less than 7 daysÎncă nu există evaluări

- The Mary Brooks Picken Method of Modern DressmakingDe la EverandThe Mary Brooks Picken Method of Modern DressmakingEvaluare: 5 din 5 stele5/5 (1)

- Chinese Dress: From the Qing Dynasty to the Present DayDe la EverandChinese Dress: From the Qing Dynasty to the Present DayEvaluare: 5 din 5 stele5/5 (4)

- Amigurumi Made Simple: A Step-By-Step Guide for Trendy Crochet CreationsDe la EverandAmigurumi Made Simple: A Step-By-Step Guide for Trendy Crochet CreationsÎncă nu există evaluări

- Advanced Gunsmithing: A Manual of Instruction in the Manufacture, Alteration, and Repair of Firearms (75th Anniversary Edition)De la EverandAdvanced Gunsmithing: A Manual of Instruction in the Manufacture, Alteration, and Repair of Firearms (75th Anniversary Edition)Evaluare: 3.5 din 5 stele3.5/5 (2)

- Hands of Time: A Watchmaker’s HistoryDe la EverandHands of Time: A Watchmaker’s HistoryEvaluare: 4.5 din 5 stele4.5/5 (5)

- The LEGO Story: How a Little Toy Sparked the World's ImaginationDe la EverandThe LEGO Story: How a Little Toy Sparked the World's ImaginationEvaluare: 3.5 din 5 stele3.5/5 (14)

- The Illustrated Directory of Guns: A Collector's Guide to Over 1500 Military, Sporting, and Antique FirearmsDe la EverandThe Illustrated Directory of Guns: A Collector's Guide to Over 1500 Military, Sporting, and Antique FirearmsEvaluare: 4 din 5 stele4/5 (5)