S-ar putea să vă placă și

- Running A Hedge FundDocument8 paginiRunning A Hedge Fundhandsomevj100% (1)

- The 2019 Digital Transformation - HCM - and ERP Report PDFDocument23 paginiThe 2019 Digital Transformation - HCM - and ERP Report PDFsaikrsh99Încă nu există evaluări

- IMG Menu: Controlling Profitability Analysis Structures Define Operating Concern Maintain Operating ConcernDocument25 paginiIMG Menu: Controlling Profitability Analysis Structures Define Operating Concern Maintain Operating ConcernMarceloÎncă nu există evaluări

- Zero-Based BudgetingDocument12 paginiZero-Based BudgetingXuan Hung0% (1)

- Module 5 - Fundamental Principles of ValuationDocument55 paginiModule 5 - Fundamental Principles of ValuationTricia Angela Nicolas100% (1)

- Textbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsDe la EverandTextbook of Urgent Care Management: Chapter 12, Pro Forma Financial StatementsÎncă nu există evaluări

- The Outsourcing Revolution (Review and Analysis of Corbett's Book)De la EverandThe Outsourcing Revolution (Review and Analysis of Corbett's Book)Încă nu există evaluări

- How To Analyse Profitability: Dupont System, Ebitda and Earnings QualityDocument11 paginiHow To Analyse Profitability: Dupont System, Ebitda and Earnings QualityNam Duy VuÎncă nu există evaluări

- Advantages and Disadvantages of Virtual TeamsDocument2 paginiAdvantages and Disadvantages of Virtual TeamsShannon RosalesÎncă nu există evaluări

- Dupont Ratio AnalysisDocument22 paginiDupont Ratio Analysiszeeshan655100% (1)

- HR Book of Metrics 2009Document18 paginiHR Book of Metrics 2009sngtÎncă nu există evaluări

- Blackbook 2022Document59 paginiBlackbook 2022champu gampuÎncă nu există evaluări

- CFA Scholarship 2015 Dec NotificationDocument1 paginăCFA Scholarship 2015 Dec NotificationZihad Al AminÎncă nu există evaluări

- Cost Benefit AnalysisDocument4 paginiCost Benefit AnalysisPriya SainiÎncă nu există evaluări

- 2013 Business Expense Benchmark SurveyDocument48 pagini2013 Business Expense Benchmark SurveyRichard SimmonsÎncă nu există evaluări

- Cost Benefit AnalysisDocument4 paginiCost Benefit AnalysisPriya SainiÎncă nu există evaluări

- Epicor Mid-Size Customers: Beating The Best-in-Class With Low TCODocument8 paginiEpicor Mid-Size Customers: Beating The Best-in-Class With Low TCOHuong NguyenÎncă nu există evaluări

- Accounting Information System Research PaperDocument8 paginiAccounting Information System Research Paperuylijwznd100% (1)

- Article 11Document8 paginiArticle 11Fadil YmÎncă nu există evaluări

- Protiviti Qa We v10n3Document2 paginiProtiviti Qa We v10n3jayapÎncă nu există evaluări

- Anil Kumar Singh Roll No-23 Section - A PgdimDocument7 paginiAnil Kumar Singh Roll No-23 Section - A PgdimAnil SinghÎncă nu există evaluări

- Workforce Alignment and The Bottom Line: The ROI of Enterprise Compensation ManagementDocument19 paginiWorkforce Alignment and The Bottom Line: The ROI of Enterprise Compensation ManagementGunjan KumariÎncă nu există evaluări

- Iofm Certify 5Document10 paginiIofm Certify 5Khaled YoussefÎncă nu există evaluări

- Effect of Earnings Management On Cost ofDocument10 paginiEffect of Earnings Management On Cost ofazhar maksumÎncă nu există evaluări

- Research Paper On Accounting Information SystemsDocument6 paginiResearch Paper On Accounting Information Systemsfvffv0x7Încă nu există evaluări

- Do You Know Your Cost of CapitalDocument12 paginiDo You Know Your Cost of CapitalSazidur RahmanÎncă nu există evaluări

- PHD Thesis On Ratio AnalysisDocument5 paginiPHD Thesis On Ratio Analysisaflodnyqkefbbm100% (2)

- Farm Financial RatiosDocument10 paginiFarm Financial Ratiosrobert_tignerÎncă nu există evaluări

- Literature Review On Profit MaximizationDocument6 paginiLiterature Review On Profit Maximizationea4c954q100% (1)

- KellogDocument2 paginiKellogDhruv Gupta100% (1)

- Insead: How To Understand Financial AnalysisDocument9 paginiInsead: How To Understand Financial Analysis0asdf4Încă nu există evaluări

- Accounting in A Nutshell 7: Financial Ratios and AnalysisDocument3 paginiAccounting in A Nutshell 7: Financial Ratios and AnalysisBusiness Expert PressÎncă nu există evaluări

- Chapter 17Document18 paginiChapter 17sundaravalliÎncă nu există evaluări

- June 2011Document19 paginiJune 2011Murugesh Kasivel EnjoyÎncă nu există evaluări

- SSRN Id2888365Document19 paginiSSRN Id2888365LeilaÎncă nu există evaluări

- Bab 5Document15 paginiBab 5An Sakina FathiaÎncă nu există evaluări

- The Global Tax Disputes EnvironmentDocument16 paginiThe Global Tax Disputes EnvironmentFlaisLibelÎncă nu există evaluări

- Fsav4e SM Mod15Document25 paginiFsav4e SM Mod15Anonymous 9FlDK6YrJ100% (1)

- Aberdeen Cloud Research Report 2012Document6 paginiAberdeen Cloud Research Report 2012avalaraÎncă nu există evaluări

- Rvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612Document3 paginiRvunc Department of Management: Mba Program Course Title: Financial and Managerial Accounting Course Code: Mbad612markosÎncă nu există evaluări

- Business Finance Completed 3Document10 paginiBusiness Finance Completed 3mamaluicalinÎncă nu există evaluări

- A I A Financial Best PracticesDocument2 paginiA I A Financial Best PracticesamtavareÎncă nu există evaluări

- Final Empirical AnalysisDocument14 paginiFinal Empirical AnalysisOnyango StephenÎncă nu există evaluări

- Financial Ratio Analysis Research PaperDocument4 paginiFinancial Ratio Analysis Research Papergvznwmfc100% (1)

- Topics in Finance Part III-Leverage: American Journal of Business Education - April 2010 Volume 3, Number 4Document6 paginiTopics in Finance Part III-Leverage: American Journal of Business Education - April 2010 Volume 3, Number 4prem_k_sÎncă nu există evaluări

- Do Indian Companies Really Manipulate Their EarningsDocument3 paginiDo Indian Companies Really Manipulate Their EarningsarcherselevatorsÎncă nu există evaluări

- BC Resources Benchmarking Report 2022Document24 paginiBC Resources Benchmarking Report 2022Rafael GuessÎncă nu există evaluări

- Multiple Choice Questions: Top of FormDocument96 paginiMultiple Choice Questions: Top of Formchanfa3851Încă nu există evaluări

- 2.2 Article 2 - Accounting Comparability and Relative Performance Evaluation by Capital MarketsDocument40 pagini2.2 Article 2 - Accounting Comparability and Relative Performance Evaluation by Capital MarketsMonica Ratu LeoÎncă nu există evaluări

- CS Professional Programme Group 3Document37 paginiCS Professional Programme Group 3santhoshttacsÎncă nu există evaluări

- Managerial Economics: 14 EditionDocument32 paginiManagerial Economics: 14 EditionahmadÎncă nu există evaluări

- TAX FunctionDocument18 paginiTAX FunctionDaniel Andres CorderoÎncă nu există evaluări

- Research Paper On Ratio AnalysisDocument8 paginiResearch Paper On Ratio Analysislekotopizow2100% (1)

- Financial RatiosDocument30 paginiFinancial RatiosMomal KhawajaÎncă nu există evaluări

- An Analysis of Working Capital Management Efficiency in Telecommunication Equipment IndustryDocument10 paginiAn Analysis of Working Capital Management Efficiency in Telecommunication Equipment IndustryHerminaVeronikaÎncă nu există evaluări

- Full Download Managerial Economics 12th Edition Hirschey Solutions ManualDocument20 paginiFull Download Managerial Economics 12th Edition Hirschey Solutions Manualmasonsnydergpwo100% (24)

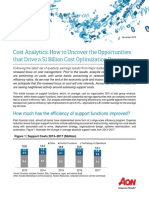

- How Much Has The Efficiency of Support Functions Improved?: Figure 1: Support Costs 2013 - 2017 ($billion)Document7 paginiHow Much Has The Efficiency of Support Functions Improved?: Figure 1: Support Costs 2013 - 2017 ($billion)Mehadi HasanÎncă nu există evaluări

- Application of Ratio Analysis and DuPont SystemDocument19 paginiApplication of Ratio Analysis and DuPont SystemRafatul IslamÎncă nu există evaluări

- ERP's Second Wave: Maximizing The Value of ERP-Enabled ProcessesDocument28 paginiERP's Second Wave: Maximizing The Value of ERP-Enabled ProcessesBrenno BarcelosÎncă nu există evaluări

- Basic Final Account RatiosDocument14 paginiBasic Final Account RatiosJahanzaib ButtÎncă nu există evaluări

- A Study On Working Capital Management at Berger Paints LTDDocument6 paginiA Study On Working Capital Management at Berger Paints LTDdanny kanniÎncă nu există evaluări

- MOBT26 Breakthrough IT BankingDocument6 paginiMOBT26 Breakthrough IT BankingMuhammad RamadhanÎncă nu există evaluări

- Analyzing and Quantifying Your Company Asset Management OpportunityDocument8 paginiAnalyzing and Quantifying Your Company Asset Management OpportunityWojtek MaczynskiÎncă nu există evaluări

- Chapter 12Document11 paginiChapter 12diane camansagÎncă nu există evaluări

- Tugas ManPro Group 1Document2 paginiTugas ManPro Group 1Salshadina SundariÎncă nu există evaluări

- Investing in Banking Sector Mutual Funds - An OverviewDocument5 paginiInvesting in Banking Sector Mutual Funds - An OverviewarcherselevatorsÎncă nu există evaluări

- Circular 1 of 2016 TR 32 Directors LoanDocument6 paginiCircular 1 of 2016 TR 32 Directors LoanAunÎncă nu există evaluări

- End User License Agreement BOOM LIBRARY For Single Users IMPORTANT-READ CAREFULLY: This BOOM Library End-User License Agreement (Or "EULA")Document3 paginiEnd User License Agreement BOOM LIBRARY For Single Users IMPORTANT-READ CAREFULLY: This BOOM Library End-User License Agreement (Or "EULA")jumoÎncă nu există evaluări

- Basic Accounting ExamDocument8 paginiBasic Accounting ExamMikaela SalvadorÎncă nu există evaluări

- FIN 335 UNCW Phase III NotesDocument23 paginiFIN 335 UNCW Phase III NotesMonydit SantinoÎncă nu există evaluări

- Inspection & Test Plans (ITP's) : A Step by Step Guide To Producing An ITPDocument7 paginiInspection & Test Plans (ITP's) : A Step by Step Guide To Producing An ITPMohd parvezÎncă nu există evaluări

- Pengaruh Marketing Public Relations Dan Kualitas Pelayanan Terhadap Citra Rumah Sakit Syafira PekanbaruDocument14 paginiPengaruh Marketing Public Relations Dan Kualitas Pelayanan Terhadap Citra Rumah Sakit Syafira PekanbaruRahmaÎncă nu există evaluări

- 1812 Growing Revenues Through Commercial Excellence LEK Executive InsightsDocument5 pagini1812 Growing Revenues Through Commercial Excellence LEK Executive InsightsNguyễn Duy LongÎncă nu există evaluări

- HCS-341-Human Resource Management RolesDocument4 paginiHCS-341-Human Resource Management RolesJulia A. SkahanÎncă nu există evaluări

- Definition of WagesDocument8 paginiDefinition of WagesCorolla SedanÎncă nu există evaluări

- CCS Analysis - Group 11 - Blue PDFDocument9 paginiCCS Analysis - Group 11 - Blue PDFYash BumbÎncă nu există evaluări

- 2 1 Charting BasicsDocument11 pagini2 1 Charting BasicsEzequiel RodriguezÎncă nu există evaluări

- Almarai Company in UAE RevisionDocument14 paginiAlmarai Company in UAE Revisionsaleem razaÎncă nu există evaluări

- Company Auditor's ReportDocument11 paginiCompany Auditor's ReportVinayak SaxenaÎncă nu există evaluări

- Edp Imp QuestionsDocument3 paginiEdp Imp QuestionsAshutosh SinghÎncă nu există evaluări

- Payment Gateway PlayerDocument5 paginiPayment Gateway PlayerHilmanie RamadhanÎncă nu există evaluări

- Quantity Discount Model (Example)Document13 paginiQuantity Discount Model (Example)shirleyna saraÎncă nu există evaluări

- Mid-1990's Competitive Positioning (Tangible) New Competitive Positioning (Tangible)Document3 paginiMid-1990's Competitive Positioning (Tangible) New Competitive Positioning (Tangible)Bogs MartinezÎncă nu există evaluări

- Smart Investors DataDocument6 paginiSmart Investors DataSamrat SahaÎncă nu există evaluări

- Index: Manual For (BIG)Document32 paginiIndex: Manual For (BIG)suryaÎncă nu există evaluări

- Barlaman Today, 2022, Food Delivery Services in MoroccoDocument7 paginiBarlaman Today, 2022, Food Delivery Services in MoroccoFatima Zahra ZeroualiÎncă nu există evaluări

- Market Leader Progress TestDocument3 paginiMarket Leader Progress TestBenGreenÎncă nu există evaluări

- Lundin Oilgate War Crimes Carl Bildt (Company Propaganda)Document108 paginiLundin Oilgate War Crimes Carl Bildt (Company Propaganda)mary engÎncă nu există evaluări

- Engineering EconomicspreboardDocument2 paginiEngineering EconomicspreboardNUCUP Marco V.Încă nu există evaluări