S-ar putea să vă placă și

- Bernanke Reinhart AER 2004Document6 paginiBernanke Reinhart AER 2004jcaboÎncă nu există evaluări

- Macroeconomics and Financial CrisisDocument11 paginiMacroeconomics and Financial Crisisslarti007Încă nu există evaluări

- El2018 06Document5 paginiEl2018 06TBP_Think_TankÎncă nu există evaluări

- Money and Capital Markets PDFDocument9 paginiMoney and Capital Markets PDFManish SinghÎncă nu există evaluări

- TTP 0611 Can You Time LongDurationDocument3 paginiTTP 0611 Can You Time LongDurationEun Woo HaÎncă nu există evaluări

- Money Market Interest RatesDocument4 paginiMoney Market Interest RatesTeffi Boyer MontoyaÎncă nu există evaluări

- Term Premia: Models and Some Stylised FactsDocument13 paginiTerm Premia: Models and Some Stylised FactssdafwetÎncă nu există evaluări

- Working Paper No. 698: $29,000,000,000,000: A Detailed Look at The Fed's Bailout by Funding Facility and RecipientDocument33 paginiWorking Paper No. 698: $29,000,000,000,000: A Detailed Look at The Fed's Bailout by Funding Facility and RecipientphollingsÎncă nu există evaluări

- The Feds New Monetary Policy Tools - SEDocument11 paginiThe Feds New Monetary Policy Tools - SEAndré M. TrottaÎncă nu există evaluări

- GW JEL DraftDocument65 paginiGW JEL DraftFirman Aditya BaskoroÎncă nu există evaluări

- Has Forward Guidance Been Effective?Document22 paginiHas Forward Guidance Been Effective?AdminAliÎncă nu există evaluări

- Interest RatesDocument8 paginiInterest RatesMuhammad Sanawar ChaudharyÎncă nu există evaluări

- The Federal Reserve's Framework For Monetary Policy-Recent Changes and New QuestionsDocument71 paginiThe Federal Reserve's Framework For Monetary Policy-Recent Changes and New Questionsrichardck61Încă nu există evaluări

- Monetary Policy ToolsDocument8 paginiMonetary Policy ToolsFreddie254Încă nu există evaluări

- Monetary PolicyDocument4 paginiMonetary PolicySadia R ChowdhuryÎncă nu există evaluări

- Monetary PolicyDocument8 paginiMonetary PolicyHarsha KhianiÎncă nu există evaluări

- ECO201 Pricniples of Macroeconomics Final ExaminationDocument5 paginiECO201 Pricniples of Macroeconomics Final ExaminationGinoh K.Încă nu există evaluări

- MacroDocument29 paginiMacrozohaibsikandarÎncă nu există evaluări

- The Signaling Channel For Federal Reserve Bond Purchases: Michael D. Bauer and Glenn D. RudebuschDocument57 paginiThe Signaling Channel For Federal Reserve Bond Purchases: Michael D. Bauer and Glenn D. RudebuschAdminAliÎncă nu există evaluări

- Open Market Operations vs. Quantitative Easing: What's The Difference?Document4 paginiOpen Market Operations vs. Quantitative Easing: What's The Difference?Kurt Del RosarioÎncă nu există evaluări

- Stein Et Al-2018-The Journal of FinanceDocument46 paginiStein Et Al-2018-The Journal of FinancesdafwetÎncă nu există evaluări

- An Arbitrage-Free Three-Factor Term Structure Model and The Recent Behavior of Long-Term Yields and Distant-Horizon Forward RatesDocument27 paginiAn Arbitrage-Free Three-Factor Term Structure Model and The Recent Behavior of Long-Term Yields and Distant-Horizon Forward RatessjanaszakÎncă nu există evaluări

- FIM Term ReportDocument8 paginiFIM Term ReportYousuf ShabbirÎncă nu există evaluări

- Fiscal Implications of The Federal Reserve's Balance Sheet NormalizationDocument47 paginiFiscal Implications of The Federal Reserve's Balance Sheet NormalizationTBP_Think_Tank100% (1)

- When Interest Rates Rise: Less Than 2%Document11 paginiWhen Interest Rates Rise: Less Than 2%macurriÎncă nu există evaluări

- Fed Rate Cut N ImplicationsDocument8 paginiFed Rate Cut N Implicationssplusk100% (1)

- The Importance of Interest RatesDocument8 paginiThe Importance of Interest RatesTanvi VermaÎncă nu există evaluări

- Proiect EnglezaDocument11 paginiProiect EnglezaAmy JonesÎncă nu există evaluări

- GR Fed Hidden Agenda-Drive Into DepressionDocument8 paginiGR Fed Hidden Agenda-Drive Into Depressionanon_717974Încă nu există evaluări

- Ife - UsaDocument13 paginiIfe - Usagiovanni lazzeriÎncă nu există evaluări

- Expectation and Monetary PolicyDocument38 paginiExpectation and Monetary Policy유빛나리Încă nu există evaluări

- FRBSF Economic LetterDocument4 paginiFRBSF Economic Letterga082003Încă nu există evaluări

- AC3104 - Chapter 2-3 AssessmentDocument2 paginiAC3104 - Chapter 2-3 AssessmentJohn Francis SumalinogÎncă nu există evaluări

- Fedpolicy Lecture MaterialsDocument8 paginiFedpolicy Lecture MaterialsAnimals12Încă nu există evaluări

- Financial MarketsDocument6 paginiFinancial MarketsRudella LizardoÎncă nu există evaluări

- SSRN Id2129296Document23 paginiSSRN Id2129296Edison LzÎncă nu există evaluări

- Central Bank Deposits Federal Reserve BankDocument2 paginiCentral Bank Deposits Federal Reserve Bankarvin cleinÎncă nu există evaluări

- Global MarketsDocument2 paginiGlobal MarketsSunny M.Încă nu există evaluări

- 5) Exam Is Due Back Before Midnight (EST) On Nov 5: WWW - Federalreserve.govDocument3 pagini5) Exam Is Due Back Before Midnight (EST) On Nov 5: WWW - Federalreserve.govTrevor TwardzikÎncă nu există evaluări

- EM4001Ch6 Gearing and Cost of CapitalDocument42 paginiEM4001Ch6 Gearing and Cost of CapitalGabriel OkuyemiÎncă nu există evaluări

- QE Equivalence To Interest Rate Policy: Implications For ExitDocument13 paginiQE Equivalence To Interest Rate Policy: Implications For ExitAlexandreau del FierroÎncă nu există evaluări

- GAO Report Fall 2009Document13 paginiGAO Report Fall 2009thecynicaleconomistÎncă nu există evaluări

- Name of The Student Course Professor University FinanceDocument16 paginiName of The Student Course Professor University FinanceBharat KoiralaÎncă nu există evaluări

- The U.S. Federal Reserve Is On The Verge of Raising Short-Term Rates For The Third Time Since The Global Financial Markets Crisis Hit Ten Years AgoDocument2 paginiThe U.S. Federal Reserve Is On The Verge of Raising Short-Term Rates For The Third Time Since The Global Financial Markets Crisis Hit Ten Years AgoEli LiÎncă nu există evaluări

- Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CDocument27 paginiFinance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CTBP_Think_TankÎncă nu există evaluări

- Federal Reserve: Unconventional Monetary Policy Options: Marc LabonteDocument37 paginiFederal Reserve: Unconventional Monetary Policy Options: Marc Labonterichardck61Încă nu există evaluări

- WP5 EpsteinDocument26 paginiWP5 EpsteinererereretrterÎncă nu există evaluări

- Viney7e SM Ch13Document27 paginiViney7e SM Ch13nooguÎncă nu există evaluări

- Felicia Irene - Week 5Document27 paginiFelicia Irene - Week 5felicia ireneÎncă nu există evaluări

- Macro Economics ProjectDocument12 paginiMacro Economics ProjectnilaykmajmudarÎncă nu există evaluări

- ChenPhelan DynamicConsequencesDocument58 paginiChenPhelan DynamicConsequencesHelloÎncă nu există evaluări

- What Does Monetary Policy Do To Long-Term Interest Rates at The Zero Lower Bound?Document38 paginiWhat Does Monetary Policy Do To Long-Term Interest Rates at The Zero Lower Bound?Gaurav JainÎncă nu există evaluări

- BIS Working Papers: The Interest Rate Effects of Government Debt MaturityDocument52 paginiBIS Working Papers: The Interest Rate Effects of Government Debt MaturityKarin Denise Zurita VidalÎncă nu există evaluări

- Fiscal ImpDocument5 paginiFiscal ImpabdulsamadÎncă nu există evaluări

- Why Real Yields Matter - Pictet Asset ManagementDocument7 paginiWhy Real Yields Matter - Pictet Asset ManagementLOKE SENG ONNÎncă nu există evaluări

- The ProblemDocument2 paginiThe ProblemDan IslÎncă nu există evaluări

- Thesis Monetary PolicyDocument6 paginiThesis Monetary Policycgvmxrief100% (2)

- Conduct of Monetary Policy Goal and TargetsDocument12 paginiConduct of Monetary Policy Goal and TargetsSumra KhanÎncă nu există evaluări

- Monetary Policy in an Uncertain World: Ten Years After the CrisisDe la EverandMonetary Policy in an Uncertain World: Ten Years After the CrisisÎncă nu există evaluări

- Common Sense Retirement Planning: Home, Savings and InvestmentDe la EverandCommon Sense Retirement Planning: Home, Savings and InvestmentÎncă nu există evaluări

- Kowa Sporting Optics Spotting Scopes TSN 880 770 ManualDocument4 paginiKowa Sporting Optics Spotting Scopes TSN 880 770 Manualetz3lÎncă nu există evaluări

- Spring Summer 2015Document28 paginiSpring Summer 2015etz3lÎncă nu există evaluări

- Liability SampleDocument2 paginiLiability Sampleetz3lÎncă nu există evaluări

- Whirlpool Duet Washer Service ManualDocument72 paginiWhirlpool Duet Washer Service ManualKenrick William60% (5)

- Pansat 3500s Setup GuideDocument12 paginiPansat 3500s Setup Guideetz3lÎncă nu există evaluări

- Write A Note On Previous Year and Assessment YearDocument2 paginiWrite A Note On Previous Year and Assessment YearBhaskar BhaskiÎncă nu există evaluări

- CashflowFK Broad Game 1Document24 paginiCashflowFK Broad Game 1TerenceÎncă nu există evaluări

- UntitledDocument267 paginiUntitledGaurav KothariÎncă nu există evaluări

- Marketing - Ansoff MatrixDocument8 paginiMarketing - Ansoff Matrixmatthew mafaraÎncă nu există evaluări

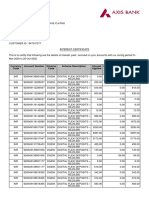

- Interest CertificateDocument2 paginiInterest CertificatesumitÎncă nu există evaluări

- Introduction AdvertisingDocument82 paginiIntroduction AdvertisingselbalÎncă nu există evaluări

- Exercise CorporationDocument3 paginiExercise CorporationJefferson MañaleÎncă nu există evaluări

- SM1001904 Chapter-5 Caselets PDFDocument4 paginiSM1001904 Chapter-5 Caselets PDFsai bhargavÎncă nu există evaluări

- Fauji Fertilizer Company LimitedDocument16 paginiFauji Fertilizer Company Limitedkhan izharÎncă nu există evaluări

- Tissue Paper Converting Unit Rs. 36.22 Million Mar-2020Document29 paginiTissue Paper Converting Unit Rs. 36.22 Million Mar-2020Rana Muhammad Ayyaz Rasul100% (1)

- Security Bank V Cuenca DigestDocument3 paginiSecurity Bank V Cuenca DigestJermone MuaripÎncă nu există evaluări

- Chapter 10: The Foreign Exchange Market: True / False QuestionsDocument49 paginiChapter 10: The Foreign Exchange Market: True / False QuestionsQuốc PhúÎncă nu există evaluări

- New FORM 15H Applicable PY 2016-17Document2 paginiNew FORM 15H Applicable PY 2016-17addsingh100% (1)

- Project of Merger Acquisition SANJAYDocument65 paginiProject of Merger Acquisition SANJAYmangundesanju77% (74)

- Chapter 21 The Influence of Monetary and Fiscal Policy On Aggregate DemandDocument50 paginiChapter 21 The Influence of Monetary and Fiscal Policy On Aggregate DemandRafiathsÎncă nu există evaluări

- MODULE 1 AFNA ACT2A AnswersDocument2 paginiMODULE 1 AFNA ACT2A AnswersRowena Serrano100% (3)

- Accounting For Managers Course PlanDocument3 paginiAccounting For Managers Course PlankelifaÎncă nu există evaluări

- Development Bank of The Philippines v. The Hon. Secretary of Labor, Cresencia Difontorum, Et AlDocument2 paginiDevelopment Bank of The Philippines v. The Hon. Secretary of Labor, Cresencia Difontorum, Et AlKriselÎncă nu există evaluări

- Business Studies - Exam Paper 1Document12 paginiBusiness Studies - Exam Paper 1Azar100% (1)

- Corporate Finance and Investment Decisions and Strategies 9Th Edition Full ChapterDocument41 paginiCorporate Finance and Investment Decisions and Strategies 9Th Edition Full Chapterharriett.murphy498100% (24)

- Chapter 6 Exclusions From Gross Income PDFDocument12 paginiChapter 6 Exclusions From Gross Income PDFkimberly tenebroÎncă nu există evaluări

- PIC Q As As of 6.30.20 PDFDocument749 paginiPIC Q As As of 6.30.20 PDFKatherine Cabading InocandoÎncă nu există evaluări

- Chapter 3 ProblemsDocument7 paginiChapter 3 ProblemsShaila MarceloÎncă nu există evaluări

- Ca Manoj Kumar: Skill Set ProfilesnapshotDocument2 paginiCa Manoj Kumar: Skill Set ProfilesnapshotThe Cultural CommitteeÎncă nu există evaluări

- Integrated Review Ceu PDFDocument28 paginiIntegrated Review Ceu PDFHello Kitty100% (1)

- Errata Group Statements Vol 2 17th Ed Reprint 2021Document10 paginiErrata Group Statements Vol 2 17th Ed Reprint 2021THABO CLARENCE MohleleÎncă nu există evaluări

- Assignment No. 1Document3 paginiAssignment No. 1EÎncă nu există evaluări

- Forex - DerivativesDocument5 paginiForex - DerivativesAllyse CarandangÎncă nu există evaluări

- NTRP - Track Transaction HistoryDocument2 paginiNTRP - Track Transaction HistorySathish KumarÎncă nu există evaluări

- Module 4 - Forms of Business OrganizationDocument6 paginiModule 4 - Forms of Business OrganizationMarjon DimafilisÎncă nu există evaluări