S-ar putea să vă placă și

- E CommerceDocument7 paginiE CommerceSubaash KumaraswamyÎncă nu există evaluări

- Marine PollutionDocument3 paginiMarine PollutionSubaash KumaraswamyÎncă nu există evaluări

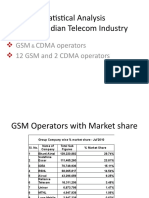

- Statistical Analysis of The Indian Telecom Industry: GSM CDMA Operators 12 GSM and 2 CDMA OperatorsDocument18 paginiStatistical Analysis of The Indian Telecom Industry: GSM CDMA Operators 12 GSM and 2 CDMA OperatorsSubaash KumaraswamyÎncă nu există evaluări

- Leadership GE CASE AnalysisDocument19 paginiLeadership GE CASE Analysisavik_bang100% (11)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Vertical Boundaries of The Firm PDFDocument53 paginiThe Vertical Boundaries of The Firm PDFsilvia100% (1)

- Chapter 6 - Macroeconomics Big PictureDocument37 paginiChapter 6 - Macroeconomics Big Picturemajor raveendraÎncă nu există evaluări

- CH 21Document20 paginiCH 21sumihosaÎncă nu există evaluări

- The Weekly Profile Guide - VolDocument19 paginiThe Weekly Profile Guide - VolJean TehÎncă nu există evaluări

- Bed1201 Introduction To MacroeconomicsDocument3 paginiBed1201 Introduction To Macroeconomicsisaac rotichÎncă nu există evaluări

- Northwest University Nursing Graduates EmployabilityDocument14 paginiNorthwest University Nursing Graduates EmployabilityMinti BravoÎncă nu există evaluări

- Inflation in Cambodia-Causes and Effects On The PoorDocument3 paginiInflation in Cambodia-Causes and Effects On The PoorVutha Ros100% (1)

- 36 HDocument3 pagini36 HabducdmaÎncă nu există evaluări

- ArbitrageDocument16 paginiArbitrageRishabYdvÎncă nu există evaluări

- A Strategic Management Review of Pakistan RailwaysDocument28 paginiA Strategic Management Review of Pakistan RailwaysBilal100% (3)

- The RC ExcelDocument12 paginiThe RC ExcelGorang PatÎncă nu există evaluări

- Supply and Demand: Managerial Economics: Economic Tools For Today's Decision Makers, 4/e by Paul Keat and Philip YoungDocument42 paginiSupply and Demand: Managerial Economics: Economic Tools For Today's Decision Makers, 4/e by Paul Keat and Philip YoungGAYLY ANN TOLENTINOÎncă nu există evaluări

- Assume That You Recently Graduated With A Major in FinanceDocument2 paginiAssume That You Recently Graduated With A Major in FinanceAmit PandeyÎncă nu există evaluări

- Friend's Cell Phone Provider ChoiceDocument4 paginiFriend's Cell Phone Provider ChoiceRose Fetz100% (3)

- JPM Guide To The Markets 2020Document71 paginiJPM Guide To The Markets 2020John PÎncă nu există evaluări

- Tutorial 1 QuestionsDocument4 paginiTutorial 1 QuestionsShayal ChandÎncă nu există evaluări

- Project Viability Assessment Worked ExampleDocument5 paginiProject Viability Assessment Worked ExampleokucuanthonyÎncă nu există evaluări

- Managing Finances A Shariah Compliant Way PDFDocument290 paginiManaging Finances A Shariah Compliant Way PDFkhaliljoiy100% (1)

- Transfer Pricing: CA Final: Paper 5: Advanced Management Accounting: Chapter 7Document71 paginiTransfer Pricing: CA Final: Paper 5: Advanced Management Accounting: Chapter 7Abid Siddiq Murtazai100% (1)

- QEP 2022 Theme General State TheIAShub Sample FIDocument26 paginiQEP 2022 Theme General State TheIAShub Sample FIakash bhattÎncă nu există evaluări

- Strategic Management and Businesss Policy: Corporate External EnvironmentDocument9 paginiStrategic Management and Businesss Policy: Corporate External EnvironmentTanvir KaziÎncă nu există evaluări

- FM6 - Capital BudgetingDocument22 paginiFM6 - Capital BudgetingFelicia CarissaÎncă nu există evaluări

- Morgan Models and Experiments 2005Document13 paginiMorgan Models and Experiments 2005Tim KhamÎncă nu există evaluări

- Rajkot: Bachelor of Business AdministrationDocument75 paginiRajkot: Bachelor of Business AdministrationHarsh GoswamiÎncă nu există evaluări

- Consumption in Islamic Economic by Zubair - Hasan06Document18 paginiConsumption in Islamic Economic by Zubair - Hasan06CANDERAÎncă nu există evaluări

- Universe 12 Group 4Document3 paginiUniverse 12 Group 4Arvind SarangiÎncă nu există evaluări

- Objective Questions: Paymeni. ReceiptsDocument7 paginiObjective Questions: Paymeni. ReceiptsSakshi NagotkarÎncă nu există evaluări

- Agricultural Marketing Is The Study of All TheDocument39 paginiAgricultural Marketing Is The Study of All TheNjuguna ReubenÎncă nu există evaluări

- Public Administration EbookDocument24 paginiPublic Administration Ebookapi-371002988% (17)

- ECON-602 Problem Set 3 - SolutionsDocument6 paginiECON-602 Problem Set 3 - SolutionszedisdedÎncă nu există evaluări