S-ar putea să vă placă și

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingDe la EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingÎncă nu există evaluări

- Employee Benefits: How to Make the Most of Your Stock, Insurance, Retirement, and Executive BenefitsDe la EverandEmployee Benefits: How to Make the Most of Your Stock, Insurance, Retirement, and Executive BenefitsEvaluare: 5 din 5 stele5/5 (1)

- Chapter 1 Introduction To Personal Financial ManagementDocument9 paginiChapter 1 Introduction To Personal Financial ManagementLee K.Încă nu există evaluări

- Brighten Your Future with Sun Acceler8Document7 paginiBrighten Your Future with Sun Acceler8Princessa Lopez Masangkay100% (1)

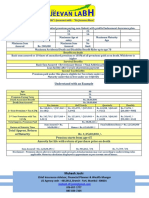

- LIC Jeevan LabhDocument1 paginăLIC Jeevan LabhMukesh JoshiÎncă nu există evaluări

- Motor Endorsement IMT Exam PrintDocument4 paginiMotor Endorsement IMT Exam Printsekkilarji92% (13)

- Auto Insurance Call Flow GuideDocument7 paginiAuto Insurance Call Flow GuideChristine Mary Lagrana GaerlanÎncă nu există evaluări

- Exercise 1Document5 paginiExercise 1Jade Y80% (5)

- HDFC Capital GuaranteeDocument34 paginiHDFC Capital GuaranteeRanjan SharmaÎncă nu există evaluări

- Jeevan Umang: Benefits Illustration SummaryDocument3 paginiJeevan Umang: Benefits Illustration Summarymr_anilpawarÎncă nu există evaluări

- GCAP - EnglishDocument2 paginiGCAP - EnglishJITENDRAÎncă nu există evaluări

- Guaranteed Savings Insurance PlanDocument5 paginiGuaranteed Savings Insurance PlanAnoop MannadathilÎncă nu există evaluări

- Edelweiss Tokio Life - GCAP - : OverviewDocument2 paginiEdelweiss Tokio Life - GCAP - : OverviewarunÎncă nu există evaluări

- HDFC Life Brochure-15Document16 paginiHDFC Life Brochure-15nayaksaismritiÎncă nu există evaluări

- HDFC Life Click 2 Wealth - Brochure - Retail - V3Document16 paginiHDFC Life Click 2 Wealth - Brochure - Retail - V3a26geniusÎncă nu există evaluări

- Jeevan Umang: Benefits Illustration SummaryDocument4 paginiJeevan Umang: Benefits Illustration SummarySelvam RamanathanÎncă nu există evaluări

- MoneyBackPlus BrochureDocument7 paginiMoneyBackPlus BrochuremanjugnpÎncă nu există evaluări

- ICICI Future Perfect - BrochureDocument11 paginiICICI Future Perfect - BrochureChandan Kumar SatyanarayanaÎncă nu există evaluări

- Summer Training Project Report On: Investors Behaviour in Insurance and Their Likeliness in Aegon LifeDocument30 paginiSummer Training Project Report On: Investors Behaviour in Insurance and Their Likeliness in Aegon LifeavnishÎncă nu există evaluări

- Exide Life Guaranteed Wealth Plus Flier 1Document6 paginiExide Life Guaranteed Wealth Plus Flier 1vickyÎncă nu există evaluări

- DownloadDocument3 paginiDownloadKiran JohnÎncă nu există evaluări

- Brochure Shriram Assured Income Plan Offline PDFDocument12 paginiBrochure Shriram Assured Income Plan Offline PDFVSÎncă nu există evaluări

- Why Wealth PlansDocument18 paginiWhy Wealth PlansDeepak SinghalÎncă nu există evaluări

- Get annual cashback and income with ICICI Pru Lakshya GoldDocument2 paginiGet annual cashback and income with ICICI Pru Lakshya GoldMehul Bajaj100% (1)

- Jeevan Labh: Benefits Illustration SummaryDocument2 paginiJeevan Labh: Benefits Illustration Summarymr_anilpawarÎncă nu există evaluări

- Lic Jeevan Umang Plan ExampleDocument3 paginiLic Jeevan Umang Plan ExampleAnil KUMAR H.VÎncă nu există evaluări

- Comparision of Whole Life PoliciesDocument8 paginiComparision of Whole Life PoliciesKunal BhansaliÎncă nu există evaluări

- Smart Platina Assure Brochure FinalDocument12 paginiSmart Platina Assure Brochure Finalsksen007Încă nu există evaluări

- Edelweiss Tokio Life - Income Builder - : OverviewDocument2 paginiEdelweiss Tokio Life - Income Builder - : OverviewarunÎncă nu există evaluări

- Protect Family & DreamsDocument6 paginiProtect Family & Dreamspradeep kumarÎncă nu există evaluări

- Edelweiss Tokio Life POS Saral Nivesh Plan SummaryDocument2 paginiEdelweiss Tokio Life POS Saral Nivesh Plan SummaryabilashvincentÎncă nu există evaluări

- Giap Sales BrochureDocument11 paginiGiap Sales BrochureAlfred MathewsÎncă nu există evaluări

- SBI Life - Smart Platina Assure - BrochureDocument12 paginiSBI Life - Smart Platina Assure - Brochuresourav agarwalÎncă nu există evaluări

- Put your finances on autopilot with guaranteed benefitsDocument8 paginiPut your finances on autopilot with guaranteed benefitsDjddhÎncă nu există evaluări

- ICICI Pru Savings SurakshaDocument8 paginiICICI Pru Savings SurakshabindalmohitÎncă nu există evaluări

- ICICI Savings SurakshaDocument8 paginiICICI Savings SurakshaNipun JainÎncă nu există evaluări

- Smart Swadhan Supreme Brochure - V01 17th Jan 1Document10 paginiSmart Swadhan Supreme Brochure - V01 17th Jan 1Nitin KumarÎncă nu există evaluări

- Grip Leaflet LatestDocument14 paginiGrip Leaflet LatestsaurabÎncă nu există evaluări

- Cashflow Protection Plus - EnglishDocument2 paginiCashflow Protection Plus - EnglishJagdeesh ShettyÎncă nu există evaluări

- ICICI Pru Savings SurakshaDocument8 paginiICICI Pru Savings SurakshaRojan G JosephÎncă nu există evaluări

- Met Pension PlansDocument12 paginiMet Pension PlansDeepanshu SharmaÎncă nu există evaluări

- Max Life Monthly Income Advantage Plan ProspectusDocument11 paginiMax Life Monthly Income Advantage Plan Prospectushemantchawla89Încă nu există evaluări

- Premier: Income PlanDocument11 paginiPremier: Income PlansrinathpsgÎncă nu există evaluări

- SBI Life - Saral Jeevan Bima - BrochureDocument9 paginiSBI Life - Saral Jeevan Bima - BrochureH.O. Rajendra TiwariÎncă nu există evaluări

- Enjoy Regular Income with SBI Life Smart Platina PlusDocument13 paginiEnjoy Regular Income with SBI Life Smart Platina PlusSUNEET KUMARÎncă nu există evaluări

- Assured Returns Savings Plan Provides Life Cover & Guaranteed ReturnsDocument12 paginiAssured Returns Savings Plan Provides Life Cover & Guaranteed ReturnsVinodkumar ShethÎncă nu există evaluări

- Tata AIA Life Insurance MoneyBackPlus BrochureDocument6 paginiTata AIA Life Insurance MoneyBackPlus BrochureasfakpaliwalaÎncă nu există evaluări

- Guide to HDFC 3D Money Back SolutionDocument2 paginiGuide to HDFC 3D Money Back SolutionRambabuÎncă nu există evaluări

- When It Comes To Securing Your Loved Ones, Trust Us.: Saral JeevanDocument10 paginiWhen It Comes To Securing Your Loved Ones, Trust Us.: Saral Jeevanjithin jayÎncă nu există evaluări

- Future PerfectDocument11 paginiFuture PerfectAditi SinghÎncă nu există evaluări

- Brochure DSPDocument8 paginiBrochure DSPCHANDRAKANT RANAÎncă nu există evaluări

- Key Benefits: Enjoy Policy Benefits Till 99 Years of AgeDocument2 paginiKey Benefits: Enjoy Policy Benefits Till 99 Years of AgeRamesh SharmaÎncă nu există evaluări

- Icici Lakshya - 10kDocument5 paginiIcici Lakshya - 10kManjunath RÎncă nu există evaluări

- ENGLISH One Pager Sanchay Plus Long Term Income Retail FinalDocument2 paginiENGLISH One Pager Sanchay Plus Long Term Income Retail FinalAbhisek BrahmaÎncă nu există evaluări

- 5032-Sanchay Broucher PDFDocument8 pagini5032-Sanchay Broucher PDFChandanÎncă nu există evaluări

- IRaksha TROP Version2 Brochure WebDocument5 paginiIRaksha TROP Version2 Brochure WebNazeerÎncă nu există evaluări

- SBI Life - Smart Platina Assure - BrochureDocument12 paginiSBI Life - Smart Platina Assure - BrochureSanjeev KulkarniÎncă nu există evaluări

- Put Your Financial Life On Autopilot With Guaranteed BenefitsDocument12 paginiPut Your Financial Life On Autopilot With Guaranteed BenefitsRengarajan ThiruvengadaswamyÎncă nu există evaluări

- Tata AIA Life Insurance Diamond Savings Plan GuideDocument7 paginiTata AIA Life Insurance Diamond Savings Plan GuideneerajishanÎncă nu există evaluări

- MGFP BrochureDocument26 paginiMGFP BrochureAbhinesh KumarÎncă nu există evaluări

- Smart - Platina - Assure - Brochure - Brand ReimagineDocument12 paginiSmart - Platina - Assure - Brochure - Brand ReimaginepankajÎncă nu există evaluări

- Key Feature Document: You Have Chosen Step Up Income Option Maturity Benefit: Income BenefitDocument3 paginiKey Feature Document: You Have Chosen Step Up Income Option Maturity Benefit: Income BenefitAnji Reddy BijjamÎncă nu există evaluări

- Never Put All Eggs in One Basket: Insurance Portfolio Suggested For Mr. D. BansalDocument8 paginiNever Put All Eggs in One Basket: Insurance Portfolio Suggested For Mr. D. BansalmonamipanjaÎncă nu există evaluări

- Win22 Pill1D Insurance Pension HDT MrunalDocument8 paginiWin22 Pill1D Insurance Pension HDT MrunalSmart BoyzÎncă nu există evaluări

- Bsvy Scheme AngulDocument125 paginiBsvy Scheme Angulvenkateswara rao PothinaÎncă nu există evaluări

- What Book Should You Read - QuizondoDocument1 paginăWhat Book Should You Read - Quizondoswirp306Încă nu există evaluări

- Attachmentsresources90316 101442 Advance Accounting Nov. 2008 PDFDocument25 paginiAttachmentsresources90316 101442 Advance Accounting Nov. 2008 PDFDipen AdhikariÎncă nu există evaluări

- Life Insurance Pension PlanDocument11 paginiLife Insurance Pension PlanHARSHAÎncă nu există evaluări

- Land Building MachineryDocument11 paginiLand Building MachineryJomerÎncă nu există evaluări

- ch.4 0Document25 paginich.4 0solid9283Încă nu există evaluări

- frmStaticPage - 2022-11-04T172525.484Document2 paginifrmStaticPage - 2022-11-04T172525.484krishna11143Încă nu există evaluări

- Notes BMGT 211 Introduction To Risk and Insurance May 2020-1Document94 paginiNotes BMGT 211 Introduction To Risk and Insurance May 2020-1jeremieÎncă nu există evaluări

- Bar Questions and Answers in Mercantile Law (Repaired)Document208 paginiBar Questions and Answers in Mercantile Law (Repaired)Ken ArnozaÎncă nu există evaluări

- Caballero Savanna Resume 2022Document1 paginăCaballero Savanna Resume 2022api-621816262Încă nu există evaluări

- Og 21 1701 1802 00209522Document10 paginiOg 21 1701 1802 00209522NaveenÎncă nu există evaluări

- Pioneer House Makati, 108 Paseo de Roxas, Legaspi Village Makati City 1229, Philippines VAT Reg. TIN: 000-541-177-00000Document6 paginiPioneer House Makati, 108 Paseo de Roxas, Legaspi Village Makati City 1229, Philippines VAT Reg. TIN: 000-541-177-00000JerroldLYIGÎncă nu există evaluări

- QBE Marine Cargo Insurance Policy SummaryDocument7 paginiQBE Marine Cargo Insurance Policy SummaryANGEL JOY RABAGOÎncă nu există evaluări

- Tom Mboya University College: Mac 206: Actuarial Mathematics 1Document6 paginiTom Mboya University College: Mac 206: Actuarial Mathematics 1EZEKIEL IGOGO100% (1)

- Sample Artist Investment AgreementDocument9 paginiSample Artist Investment AgreementMarshall - MuzeÎncă nu există evaluări

- IPFAS-AdvisoryContract-2023 Revised 4-10-2023 - Blank VersionDocument15 paginiIPFAS-AdvisoryContract-2023 Revised 4-10-2023 - Blank Versionindo 5SÎncă nu există evaluări

- IFFCO Tokio General Insurance Motor Commercial Vehicle Package PolicyDocument1 paginăIFFCO Tokio General Insurance Motor Commercial Vehicle Package PolicyAjay KumarÎncă nu există evaluări

- Patricia Kluczyk Resume: 20+ Years Customer Service ExperienceDocument3 paginiPatricia Kluczyk Resume: 20+ Years Customer Service ExperienceDana KluczykÎncă nu există evaluări

- Monthly Current Affairs PDF June PDF DownloadDocument563 paginiMonthly Current Affairs PDF June PDF DownloadVAISHNAVI SHARMAÎncă nu există evaluări

- FAC4863 NFA4863 Exam Paper 1 ScenarioDocument10 paginiFAC4863 NFA4863 Exam Paper 1 ScenarioNosipho NyathiÎncă nu există evaluări

- Sandesh MANJREKAR - TYBBI PDFDocument70 paginiSandesh MANJREKAR - TYBBI PDFnarayan patelÎncă nu există evaluări

- Chola MS: Motor Policy Schedule Cum Certificate of InsuranceDocument2 paginiChola MS: Motor Policy Schedule Cum Certificate of InsuranceAjay PrajapatiÎncă nu există evaluări

- Test Bank For A Guide To Crisis Intervention 6th EditionDocument21 paginiTest Bank For A Guide To Crisis Intervention 6th Editionbutyroushydrinae7em100% (48)

- Insurance NotesDocument3 paginiInsurance NotesNiala AlmarioÎncă nu există evaluări

- Insurance Policy Stipulation Pour Autrui CaseDocument1 paginăInsurance Policy Stipulation Pour Autrui Caseinu yashaÎncă nu există evaluări