S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

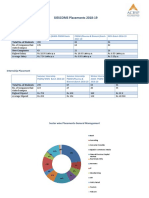

- Placement Reports SIESDocument3 paginiPlacement Reports SIESNeel ShahÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Cir vs. Solidbank Corporation2Document1 paginăCir vs. Solidbank Corporation2Raquel DoqueniaÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- K Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewDocument33 paginiK Kiran Kumar: Any Questions? Behavioral Finance, Netscape IPO, ReviewJohn DoeÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Mrunal's Economy Pillar#2B: Budget Revenue Part: Page 160Document3 paginiMrunal's Economy Pillar#2B: Budget Revenue Part: Page 160Washim Alam50CÎncă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Peregrine CNC Decision CaseDocument6 paginiPeregrine CNC Decision CaseAsadMughalÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Statement 42304092 USD 2023-03-07 2023-10-25Document6 paginiStatement 42304092 USD 2023-03-07 2023-10-25Fawad AkhtarÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Srinivas Project Questionnaire 3Document5 paginiSrinivas Project Questionnaire 3Srinivas Kannan100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Commodities: User GuideDocument9 paginiCommodities: User GuideDaer M Peña CrespoÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Your Rights: When Making Payments in EuropeDocument2 paginiYour Rights: When Making Payments in Europeenzo piroÎncă nu există evaluări

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Principle of BankingDocument2 paginiPrinciple of BankingShan PalanivalÎncă nu există evaluări

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Auditing, Kabucho MwangiDocument22 paginiAuditing, Kabucho MwangiKafonyi JohnÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- A Study On Analysis of Working Capital Management in Bhel, TrichyDocument8 paginiA Study On Analysis of Working Capital Management in Bhel, TrichyDiwakar BandarlaÎncă nu există evaluări

- SAP FICO FresherDocument3 paginiSAP FICO FresherAnudeep ReddyÎncă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Taxation in Fiscal Ad and Other IssuesDocument20 paginiTaxation in Fiscal Ad and Other IssuesJessica Villanueva GrifaldoÎncă nu există evaluări

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Credit and Debit Card Differentiation Assignment ResearchDocument9 paginiCredit and Debit Card Differentiation Assignment ResearchZubaidahÎncă nu există evaluări

- Auditor OpinionDocument1 paginăAuditor OpinionhaseebÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- Impact Turn File - MichiganClassic 2013 CTDocument125 paginiImpact Turn File - MichiganClassic 2013 CTmachina07Încă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1091)

- Specialty Packages To Super Bowl XLVDocument4 paginiSpecialty Packages To Super Bowl XLVsblaskovichÎncă nu există evaluări

- Current Liabilities and Contingencies: True-FalseDocument8 paginiCurrent Liabilities and Contingencies: True-FalseCarlo ParasÎncă nu există evaluări

- Syllabus of Private EquityDocument4 paginiSyllabus of Private EquityDeepanshu MalikÎncă nu există evaluări

- Fundamental Analysis of PNB Ltd.Document19 paginiFundamental Analysis of PNB Ltd.Ashutosh Gupta100% (1)

- The Cost of Capital: Multiple Choice QuestionsDocument26 paginiThe Cost of Capital: Multiple Choice QuestionsRodÎncă nu există evaluări

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Ar 2020 BTPN Eng 14 AprilDocument612 paginiAr 2020 BTPN Eng 14 AprilklieindwrÎncă nu există evaluări

- Assignment 001: Fundamentals of Accounting/Answer KeyDocument65 paginiAssignment 001: Fundamentals of Accounting/Answer Keymoncarla lagon83% (6)

- Bond Valuation ProblemsDocument3 paginiBond Valuation ProblemsVignesh KivickyÎncă nu există evaluări

- Chapter2 Statement of Comprehensive IncomeDocument46 paginiChapter2 Statement of Comprehensive IncomeRonald De La Rama100% (1)

- Module 4 Financial IntermediariesDocument12 paginiModule 4 Financial IntermediariesFernando III PerezÎncă nu există evaluări

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- HDFCDocument78 paginiHDFCsam04050Încă nu există evaluări

- Module 3 EXTRA SolutionsDocument17 paginiModule 3 EXTRA SolutionsJeff MercerÎncă nu există evaluări

- DHRE - Unifier Cost Code - EBS Expenditure Type Intermediate Mapping Table - Final - 7-SepDocument6 paginiDHRE - Unifier Cost Code - EBS Expenditure Type Intermediate Mapping Table - Final - 7-SepDilshad AhemadÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)