S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Cryptocurrency - 5 Expert Secrets For Beginners Investing Into Bitcoin, Ethereum and Litecoin by Anthony Tu PDFDocument105 paginiCryptocurrency - 5 Expert Secrets For Beginners Investing Into Bitcoin, Ethereum and Litecoin by Anthony Tu PDFgfgfgfgÎncă nu există evaluări

- Internship Report On ZTBL by Mumtaz Ali HulioDocument48 paginiInternship Report On ZTBL by Mumtaz Ali Hulioasif_iqbal84Încă nu există evaluări

- Revenue of PaytmDocument56 paginiRevenue of Paytmkaushal2442100% (2)

- GK Tornado Ibps RRB Main Exam 2019 English 43 PDFDocument150 paginiGK Tornado Ibps RRB Main Exam 2019 English 43 PDFSankar SreeramdasÎncă nu există evaluări

- February 2019Document4 paginiFebruary 2019sagar manghwaniÎncă nu există evaluări

- Makalah Kelompok Bahasa Inggris Tentang BankingDocument10 paginiMakalah Kelompok Bahasa Inggris Tentang BankingMuhammad Farhan Ramadhan100% (3)

- Etana - Kraken User ManualDocument28 paginiEtana - Kraken User ManualpdfimpresionesÎncă nu există evaluări

- Financial Statement: Funds SummaryDocument1 paginăFinancial Statement: Funds SummarymorganÎncă nu există evaluări

- Press Release: Finscope 2010 South Africa Small Business SurveyDocument4 paginiPress Release: Finscope 2010 South Africa Small Business SurveyadvswagathÎncă nu există evaluări

- Bank Companies Act 1991 GuideDocument16 paginiBank Companies Act 1991 GuideismailabtiÎncă nu există evaluări

- Shaadi - Traing PresentationDocument31 paginiShaadi - Traing Presentationyoge269Încă nu există evaluări

- Sturgis Rotaract Certification FormDocument3 paginiSturgis Rotaract Certification FormFenosoa HeriniainaÎncă nu există evaluări

- Tata Teleservices Limited.: Project ConnectDocument28 paginiTata Teleservices Limited.: Project ConnectshekarÎncă nu există evaluări

- Comm Rev ABELLA NOTES PDFDocument65 paginiComm Rev ABELLA NOTES PDFMarian SantosÎncă nu există evaluări

- ICICI Bank: Ecosystems For Growth: February 2021Document31 paginiICICI Bank: Ecosystems For Growth: February 2021FARMERS FLAVOURSÎncă nu există evaluări

- Ch. 1 and Ch. 2 Multiple Choice QuestionsDocument5 paginiCh. 1 and Ch. 2 Multiple Choice QuestionsBrylle TamanoÎncă nu există evaluări

- Pre and Post of Accounting 2Document14 paginiPre and Post of Accounting 2Nancy AtentarÎncă nu există evaluări

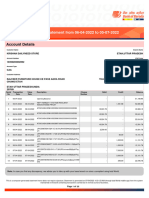

- Account Statement 230919 221019Document7 paginiAccount Statement 230919 221019Latest UpdatesÎncă nu există evaluări

- Chapter 7 Jan.22Document56 paginiChapter 7 Jan.22AaaÎncă nu există evaluări

- Hopfan Ago Tankfarm Delivery - Lagos-1Document15 paginiHopfan Ago Tankfarm Delivery - Lagos-1inspirohm777Încă nu există evaluări

- PMLA (Maintainence of Records), 2005Document24 paginiPMLA (Maintainence of Records), 2005Devendra VermaÎncă nu există evaluări

- Account StatementDocument83 paginiAccount StatementAshwani KumarÎncă nu există evaluări

- Kevin O'Connor & The Offline Assistant LOSE at The Texas Supreme Court - DecisionDocument12 paginiKevin O'Connor & The Offline Assistant LOSE at The Texas Supreme Court - DecisionTim CastlemanÎncă nu există evaluări

- TLM Fees and Expense ManagementDocument4 paginiTLM Fees and Expense ManagementMalika DwarkaÎncă nu există evaluări

- SBBL Organization Profile and ServicesDocument27 paginiSBBL Organization Profile and ServicesEklo Newar100% (1)

- Chapter 15 Managing ShortDocument48 paginiChapter 15 Managing ShortArven FrancoÎncă nu există evaluări

- EY-Smart Commerce Battling For Customers in Digital RetailDocument40 paginiEY-Smart Commerce Battling For Customers in Digital RetailEuglena VerdeÎncă nu există evaluări

- International Money Market GuideDocument2 paginiInternational Money Market GuideKainat TanveerÎncă nu există evaluări

- Istisna' - Mira&nadDocument11 paginiIstisna' - Mira&nadknadhirah100% (2)

- Chap 01Document149 paginiChap 01Hamna AzeezÎncă nu există evaluări