S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- MT Im For 2002 3 PGC This Is A Lecture About Politics Governance and Citizenship This Will HelpDocument62 paginiMT Im For 2002 3 PGC This Is A Lecture About Politics Governance and Citizenship This Will HelpGen UriÎncă nu există evaluări

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Development of PBAT Based Bio Filler Masterbatch: A Scientific Research Proposal OnDocument15 paginiDevelopment of PBAT Based Bio Filler Masterbatch: A Scientific Research Proposal OnManmathÎncă nu există evaluări

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Office Administration: School-Based AssessmentDocument17 paginiOffice Administration: School-Based AssessmentFelix LawrenceÎncă nu există evaluări

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Tournament Rules and MechanicsDocument2 paginiTournament Rules and MechanicsMarkAllenPascualÎncă nu există evaluări

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Algorithm Development and Implementation For 3D Printers Based On Adaptive PID ControllerDocument8 paginiThe Algorithm Development and Implementation For 3D Printers Based On Adaptive PID ControllerShahrzad GhasemiÎncă nu există evaluări

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Introduction To Templates in C++Document16 paginiIntroduction To Templates in C++hammarbytpÎncă nu există evaluări

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Gol GumbazDocument6 paginiGol Gumbazmnv_iitbÎncă nu există evaluări

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- LampiranDocument26 paginiLampiranSekar BeningÎncă nu există evaluări

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- 103-Article Text-514-1-10-20190329Document11 pagini103-Article Text-514-1-10-20190329Elok KurniaÎncă nu există evaluări

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Mortars in Norway From The Middle Ages To The 20th Century: Con-Servation StrategyDocument8 paginiMortars in Norway From The Middle Ages To The 20th Century: Con-Servation StrategyUriel PerezÎncă nu există evaluări

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- OMM807100043 - 3 (PID Controller Manual)Document98 paginiOMM807100043 - 3 (PID Controller Manual)cengiz kutukcu100% (3)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Debate Lesson PlanDocument3 paginiDebate Lesson Planapi-280689729Încă nu există evaluări

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- PDFDocument1 paginăPDFJaime Arroyo0% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- TOK Assessed Student WorkDocument10 paginiTOK Assessed Student WorkPeter Jun Park100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Iot Based Garbage and Street Light Monitoring SystemDocument3 paginiIot Based Garbage and Street Light Monitoring SystemHarini VenkatÎncă nu există evaluări

- Auditing Multiple Choice Questions and Answers MCQs Auditing MCQ For CA, CS and CMA Exams Principle of Auditing MCQsDocument30 paginiAuditing Multiple Choice Questions and Answers MCQs Auditing MCQ For CA, CS and CMA Exams Principle of Auditing MCQsmirjapur0% (1)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Top249 1 PDFDocument52 paginiTop249 1 PDFCarlos Henrique Dos SantosÎncă nu există evaluări

- Résumé Emily Martin FullDocument3 paginiRésumé Emily Martin FullEmily MartinÎncă nu există evaluări

- Bomba Manual Hidraulica - P 19 LDocument2 paginiBomba Manual Hidraulica - P 19 LBruno PachecoÎncă nu există evaluări

- BIO122 - CHAPTER 7 Part 1Document53 paginiBIO122 - CHAPTER 7 Part 1lili100% (1)

- End Points SubrogadosDocument3 paginiEnd Points SubrogadosAgustina AndradeÎncă nu există evaluări

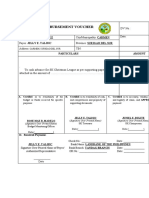

- Disbursement VoucherDocument7 paginiDisbursement VoucherDan MarkÎncă nu există evaluări

- Project 4 Close TestDocument7 paginiProject 4 Close TestErika MolnarÎncă nu există evaluări

- (Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Document7 pagini(Database Management Systems) : Biag, Marvin, B. BSIT - 202 September 6 2019Marcos JeremyÎncă nu există evaluări

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Pricelist 1Document8 paginiPricelist 1ChinangÎncă nu există evaluări

- Tripura 04092012Document48 paginiTripura 04092012ARTHARSHI GARGÎncă nu există evaluări

- Woldia University: A Non Ideal TransformerDocument24 paginiWoldia University: A Non Ideal TransformerKANDEGAMA H.R. (BET18077)Încă nu există evaluări

- Study On The Form Factor and Full-Scale Ship Resistance Prediction MethodDocument2 paginiStudy On The Form Factor and Full-Scale Ship Resistance Prediction MethodRaka AdityaÎncă nu există evaluări

- BIM and Big Data For Construction Cost ManagementDocument46 paginiBIM and Big Data For Construction Cost Managementlu09100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- ShopDrawings - Part 1Document51 paginiShopDrawings - Part 1YapÎncă nu există evaluări

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)