S-ar putea să vă placă și

- Special Audit ReportDocument4 paginiSpecial Audit ReportConrad Briones0% (1)

- Tugs - Developments For PDFDocument28 paginiTugs - Developments For PDFP Venkata SureshÎncă nu există evaluări

- Vessel CharacteristicDocument7 paginiVessel CharacteristicAlvin AlfiyansyahÎncă nu există evaluări

- Argus: Tanker FreightDocument25 paginiArgus: Tanker FreightIvan OsipovÎncă nu există evaluări

- Case Study - Marsoft Valuation MethodologyDocument8 paginiCase Study - Marsoft Valuation MethodologymekulaÎncă nu există evaluări

- Tekomar Performance Evaluation SWDocument17 paginiTekomar Performance Evaluation SWmaronnamÎncă nu există evaluări

- Shipping Market Report 17082011Document18 paginiShipping Market Report 17082011bleuwinzÎncă nu există evaluări

- Tankers Dry Bulk: Published by Fearnresearch 18. September 2013Document3 paginiTankers Dry Bulk: Published by Fearnresearch 18. September 2013SimmarineÎncă nu există evaluări

- CRSL Presentation 2nd October 2013 FinalDocument41 paginiCRSL Presentation 2nd October 2013 FinalWilliam FergusonÎncă nu există evaluări

- From T-2 to Supertanker: Development of the Oil Tanker, 1940 - 2000, RevisedDe la EverandFrom T-2 to Supertanker: Development of the Oil Tanker, 1940 - 2000, RevisedÎncă nu există evaluări

- LPGDocument15 paginiLPGMilkiss SweetÎncă nu există evaluări

- Common Chartering TermsDocument5 paginiCommon Chartering TermsNuman Kooliyat IsmethÎncă nu există evaluări

- Age Matters in ShippingDocument15 paginiAge Matters in ShippingmekulaÎncă nu există evaluări

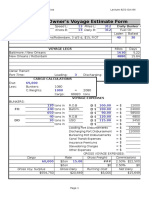

- Owner's Voyage Estimate Form: Daily Bunker ConsumptionDocument1 paginăOwner's Voyage Estimate Form: Daily Bunker ConsumptionYudi DarmawanÎncă nu există evaluări

- Worldyards May 2007 NewsletterDocument20 paginiWorldyards May 2007 Newsletternestor mospanÎncă nu există evaluări

- (E) Drybulk Daily Report 2018-12-11 (Vol. 180)Document3 pagini(E) Drybulk Daily Report 2018-12-11 (Vol. 180)amornrat kampitthayakulÎncă nu există evaluări

- MV Lubie: Wartsila Sulzer 6RTA48T-B ME Rotation: Anticlockwise AnticlockwiseDocument1 paginăMV Lubie: Wartsila Sulzer 6RTA48T-B ME Rotation: Anticlockwise AnticlockwiseemailcesÎncă nu există evaluări

- SeaIntel Sunday Spotlight Issue 100Document31 paginiSeaIntel Sunday Spotlight Issue 100Alan Roos MurphyÎncă nu există evaluări

- Wartsila o e W 34df TRDocument16 paginiWartsila o e W 34df TRMartin KratkyÎncă nu există evaluări

- Freight Methodology PDFDocument45 paginiFreight Methodology PDFNilesh JoshiÎncă nu există evaluări

- Container Market PDFDocument3 paginiContainer Market PDFDhruv AgarwalÎncă nu există evaluări

- The Worlds Top Ship Broking FirmsDocument2 paginiThe Worlds Top Ship Broking Firmsjikkuabraham2Încă nu există evaluări

- Intermodal Weekly 01-2012Document8 paginiIntermodal Weekly 01-2012Wisnu KertaningnagoroÎncă nu există evaluări

- Latin America WireDocument3 paginiLatin America WirepacocardenasÎncă nu există evaluări

- Shipping OutlookDocument27 paginiShipping OutlookmervynteoÎncă nu există evaluări

- Owner's Voyage Estimate Form: Daily Bunker ConsumptionDocument2 paginiOwner's Voyage Estimate Form: Daily Bunker ConsumptionJuan Ramón FuentesÎncă nu există evaluări

- Daily Market Report: Poten & PartnersDocument1 paginăDaily Market Report: Poten & PartnersalgeriacandaÎncă nu există evaluări

- 15 Deg - CHEMICAL BUCHANAN LOADING XX DOC. (Version 1)Document43 pagini15 Deg - CHEMICAL BUCHANAN LOADING XX DOC. (Version 1)Pavel ViktorÎncă nu există evaluări

- Shipping Intelligence 26.novDocument20 paginiShipping Intelligence 26.novleejingsongÎncă nu există evaluări

- DWT & Drafts Capacity PDFDocument7 paginiDWT & Drafts Capacity PDFRafaelsligerÎncă nu există evaluări

- Affinity Research Crude Oil Tanker Outlook 2016-11-16Document64 paginiAffinity Research Crude Oil Tanker Outlook 2016-11-16LondonguyÎncă nu există evaluări

- Marine Commercial PracticeDocument26 paginiMarine Commercial Practicekukuriku13Încă nu există evaluări

- Maritieme EconomieDocument25 paginiMaritieme Economienjirtak92Încă nu există evaluări

- NCB-PREDEP - 5 HoldsDocument5 paginiNCB-PREDEP - 5 HoldsJess NacarioÎncă nu există evaluări

- Insights Reg PlantationsDocument69 paginiInsights Reg PlantationsNasya YenitaÎncă nu există evaluări

- ASM Masters Solved Past Question Papers Solved Numericals From Sept16 Till Nov21Document302 paginiASM Masters Solved Past Question Papers Solved Numericals From Sept16 Till Nov21arivarasanÎncă nu există evaluări

- Tnker Operator Magazine 09-2015 PDFDocument52 paginiTnker Operator Magazine 09-2015 PDFyyxdÎncă nu există evaluări

- SRJ Aug Sep 2009Document76 paginiSRJ Aug Sep 2009majdirossrossÎncă nu există evaluări

- VOY 13-14 Passage Plan Merak SurabayaDocument11 paginiVOY 13-14 Passage Plan Merak SurabayaRaden Mas Farih100% (1)

- Fixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardDocument10 paginiFixation of JLPL & VSPL Tariff by PNGRB: An Overview of Gail'S Submissions To The BoardSanjai bhadouriaÎncă nu există evaluări

- Mari UglandDocument11 paginiMari UglandAtika MokhtarÎncă nu există evaluări

- Euro Gas DailyDocument8 paginiEuro Gas DailyJose DenizÎncă nu există evaluări

- CompilationDocument2 paginiCompilationryan_macadangdangÎncă nu există evaluări

- WinGD CWD-JUT-ship Template Ver20200702Document27 paginiWinGD CWD-JUT-ship Template Ver20200702Putra SeptiadyÎncă nu există evaluări

- Effective Fuel Cost On Liner Service ConfDocument13 paginiEffective Fuel Cost On Liner Service ConfOlga RegevÎncă nu există evaluări

- DNV Unveils LNG-Fueled VLCC..Document3 paginiDNV Unveils LNG-Fueled VLCC..VelmohanaÎncă nu există evaluări

- Diamond 53 Brochure PDFDocument3 paginiDiamond 53 Brochure PDFJaryÎncă nu există evaluări

- Dry BulkDocument28 paginiDry BulkyousfinacerÎncă nu există evaluări

- Draft Survey FormDocument39 paginiDraft Survey FormAnil yucebasÎncă nu există evaluări

- Willis Energy Market Review 2013 PDFDocument92 paginiWillis Energy Market Review 2013 PDFsushilk28Încă nu există evaluări

- Chemical Forecaster Exec Summary TOCDocument12 paginiChemical Forecaster Exec Summary TOCalgeriacandaÎncă nu există evaluări

- LW 20180731Document10 paginiLW 20180731Victor FernandezÎncă nu există evaluări

- Tomini Unity - Description: WWW - Alpina.dkDocument3 paginiTomini Unity - Description: WWW - Alpina.dkAnil SharmaÎncă nu există evaluări

- Intermodal Weekly Market Report 3rd February 2015, Week 5Document9 paginiIntermodal Weekly Market Report 3rd February 2015, Week 5Budi PrayitnoÎncă nu există evaluări

- Mr. G. V. Seetharam - ANALYSIS OF THE SCRAP SHIP MARKETDocument80 paginiMr. G. V. Seetharam - ANALYSIS OF THE SCRAP SHIP MARKETwebglistenÎncă nu există evaluări

- SSY Chemical WeeklyDocument3 paginiSSY Chemical WeeklyBeytullah KokoçÎncă nu există evaluări

- 2009 IAME Notteboom & CariouDocument26 pagini2009 IAME Notteboom & CarioupravanthbabuÎncă nu există evaluări

- Case Study: Ocean Carriers Inc.: Members Team: TitanicDocument9 paginiCase Study: Ocean Carriers Inc.: Members Team: TitanicAnkitÎncă nu există evaluări

- Voyage CalculationDocument7 paginiVoyage CalculationAntonius Dimas AndityaÎncă nu există evaluări

- Shipping Market Review E12Document17 paginiShipping Market Review E12fromantoanÎncă nu există evaluări

- Shipping Market Review E13Document19 paginiShipping Market Review E13fromantoan100% (1)

- Docs 101Document3 paginiDocs 101Kristine B. MaestreÎncă nu există evaluări

- Hostel ManualDocument30 paginiHostel ManualpupegufÎncă nu există evaluări

- Accpac - Guide - Checklist For Bank Setup PDFDocument4 paginiAccpac - Guide - Checklist For Bank Setup PDFcaplusincÎncă nu există evaluări

- 4 6039689226176431369Document8 pagini4 6039689226176431369Nárdï TêsfðýêÎncă nu există evaluări

- Sec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageDocument2 paginiSec. 99 A Reinsurance Is Presumed To Be A Contract of Indemnity Against Liability, and Not Merely Against DamageFlorena CayundaÎncă nu există evaluări

- PolicySchedule-211200 31 2020 284388-167798016 PDFDocument3 paginiPolicySchedule-211200 31 2020 284388-167798016 PDFKP SinghÎncă nu există evaluări

- Lucio TanDocument12 paginiLucio TanNolyne Faith O. VendiolaÎncă nu există evaluări

- Collaborative Consumption With Rachel BotsmanDocument28 paginiCollaborative Consumption With Rachel BotsmanSeokwon Yang100% (1)

- Lend LeaseDocument4 paginiLend Leaseoakley0817Încă nu există evaluări

- Muthoot Finance NCD Application Form Mar 2012Document8 paginiMuthoot Finance NCD Application Form Mar 2012Prajna CapitalÎncă nu există evaluări

- A Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectDocument16 paginiA Study On Customers Satisfaction-1102-With-cover-page-V2 Ex ProjectFelix ChristoferÎncă nu există evaluări

- Audit ReportingDocument6 paginiAudit ReportingKeith Parker100% (1)

- Middle East ATE ListDocument10 paginiMiddle East ATE ListReem JavedÎncă nu există evaluări

- Account Statement PDFDocument12 paginiAccount Statement PDFAnkitÎncă nu există evaluări

- Car Owner's Guide and Automotive NewsDocument12 paginiCar Owner's Guide and Automotive NewsNDD1959Încă nu există evaluări

- CH 21 - Audit DocumentationDocument3 paginiCH 21 - Audit DocumentationJwyneth Royce DenolanÎncă nu există evaluări

- Chap 002 NotesDocument43 paginiChap 002 NotessamiullahaslamÎncă nu există evaluări

- Tax Review QuestionsDocument11 paginiTax Review QuestionsAbigail Regondola BonitaÎncă nu există evaluări

- Noda Vs Cruz-Arnaldo 1987Document2 paginiNoda Vs Cruz-Arnaldo 1987Krizzia GojarÎncă nu există evaluări

- DOCSDocument10 paginiDOCSSWATIÎncă nu există evaluări

- Annual Rate Contract For The Supply of Electrical Items at IIM IndoreDocument22 paginiAnnual Rate Contract For The Supply of Electrical Items at IIM IndoreBhavik PrajapatiÎncă nu există evaluări

- Accounting For Disbursements and Related TransactionsDocument12 paginiAccounting For Disbursements and Related TransactionsVenn Bacus Rabadon100% (9)

- Ific Final ReportDocument26 paginiIfic Final ReportFahim AhmedÎncă nu există evaluări

- Management Consultancy: Topic OutlineDocument5 paginiManagement Consultancy: Topic OutlineGeraldÎncă nu există evaluări

- Foreign Remittance of DBBLDocument55 paginiForeign Remittance of DBBLMd Khaled NoorÎncă nu există evaluări

- Manufacturers Vs MeerDocument4 paginiManufacturers Vs MeerAlandia GaspiÎncă nu există evaluări

- Dnbs. 167 / CGM (OPA) - 2003 Dated March 29, 2003Document4 paginiDnbs. 167 / CGM (OPA) - 2003 Dated March 29, 2003Anonymous WkYgrDRÎncă nu există evaluări

- Heirs of Maglasang V MBCDocument7 paginiHeirs of Maglasang V MBCParis LisonÎncă nu există evaluări

- Accounts Project FinalDocument18 paginiAccounts Project FinalPulakÎncă nu există evaluări