S-ar putea să vă placă și

- The Incentive Plan for Efficiency in Government Operations: A Program to Eliminate Government DeficitsDe la EverandThe Incentive Plan for Efficiency in Government Operations: A Program to Eliminate Government DeficitsÎncă nu există evaluări

- CTS MCCscheme 2023 FinalDocument14 paginiCTS MCCscheme 2023 FinalLeo LouisÎncă nu există evaluări

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDe la Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsÎncă nu există evaluări

- Addendum: TO Specification For Monthly Tax Deduction (MTD) Calculations Using Computerised Calculation Method ForDocument19 paginiAddendum: TO Specification For Monthly Tax Deduction (MTD) Calculations Using Computerised Calculation Method ForKhoo Kah JinÎncă nu există evaluări

- Problems and Possibilities of the Us EconomyDe la EverandProblems and Possibilities of the Us EconomyÎncă nu există evaluări

- CTS MCCscheme 2022 FinalDocument14 paginiCTS MCCscheme 2022 FinalLeo LouisÎncă nu există evaluări

- 1040 Exam Prep: Module I: The Form 1040 FormulaDe la Everand1040 Exam Prep: Module I: The Form 1040 FormulaEvaluare: 1 din 5 stele1/5 (3)

- Circ 2815 Pay ScalesDocument104 paginiCirc 2815 Pay ScalesmagicalmarshmallowÎncă nu există evaluări

- Circular Letter 0075/2018Document5 paginiCircular Letter 0075/2018jmaguire1977Încă nu există evaluări

- October 2020 Consolidated Pay ScalesDocument91 paginiOctober 2020 Consolidated Pay ScalesdoodrillÎncă nu există evaluări

- Fundamentals of Business Economics Study Resource: CIMA Study ResourcesDe la EverandFundamentals of Business Economics Study Resource: CIMA Study ResourcesÎncă nu există evaluări

- Service Tax Exemption in IndiaDocument38 paginiService Tax Exemption in IndiaAnonymous it4wrfEOdÎncă nu există evaluări

- 06 2006 (E)Document34 pagini06 2006 (E)tracker1234100% (2)

- MACP Salient Featues DOPDocument11 paginiMACP Salient Featues DOPPNVITALKUMARÎncă nu există evaluări

- Two Pension SystemsDocument7 paginiTwo Pension SystemsSupratik PandeyÎncă nu există evaluări

- Pay Revision OrderDocument33 paginiPay Revision OrderVinod NarayaÎncă nu există evaluări

- Pay GoDocument213 paginiPay GodeepusvvpÎncă nu există evaluări

- Pay Revision Order Govt of Kerala 2010 (GO.P.85-2011)Document216 paginiPay Revision Order Govt of Kerala 2010 (GO.P.85-2011)Muhammed Basheer88% (8)

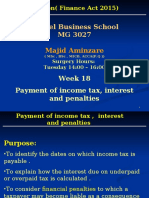

- MG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesDocument27 paginiMG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesSyed SafdarÎncă nu există evaluări

- NPS - Sec 80CCD - Additional Deduction For National Pension System ContributionDocument2 paginiNPS - Sec 80CCD - Additional Deduction For National Pension System ContributionManoj KakkarÎncă nu există evaluări

- Revision 2009Document4 paginiRevision 200904872260349Încă nu există evaluări

- Circular Letter 0024/2019Document6 paginiCircular Letter 0024/2019jmaguire1977Încă nu există evaluări

- Income Tax CircularDocument67 paginiIncome Tax CirculartaxscribdÎncă nu există evaluări

- No.11 1 2010-JCADocument31 paginiNo.11 1 2010-JCApenusilaÎncă nu există evaluări

- Chapter 03Document8 paginiChapter 03Leonel AlbanesÎncă nu există evaluări

- 03 2016 (E) PDFDocument122 pagini03 2016 (E) PDFSatkunalingam KesavarubanÎncă nu există evaluări

- Changes in GSTDocument4 paginiChanges in GSTRanjodh KaurÎncă nu există evaluări

- MACPDocument6 paginiMACPVishwesh ChaturvediÎncă nu există evaluări

- Zambia 2012 Budget HighlightsDocument10 paginiZambia 2012 Budget HighlightsChola MukangaÎncă nu există evaluări

- Budget 2010 SummaryDocument2 paginiBudget 2010 SummaryGopal Singh BhardwajÎncă nu există evaluări

- Budget 2016 Summary 30 11 2015Document4 paginiBudget 2016 Summary 30 11 2015api-301855106Încă nu există evaluări

- Tds SALARY FOR A.Y. 2011-12Document59 paginiTds SALARY FOR A.Y. 2011-12Pragnesh ShahÎncă nu există evaluări

- National Pension System (NPS) : Important Initiatives For Central Government Employees Covered Under NPSDocument5 paginiNational Pension System (NPS) : Important Initiatives For Central Government Employees Covered Under NPSதனேஷ் உÎncă nu există evaluări

- MACP 35034 - 3 - 2008-Estt. (D)Document10 paginiMACP 35034 - 3 - 2008-Estt. (D)Aniket GiriÎncă nu există evaluări

- NATIONAL BUDGET CIRCULAR NO 579 Dated January 24 2020Document9 paginiNATIONAL BUDGET CIRCULAR NO 579 Dated January 24 2020renbuenaÎncă nu există evaluări

- Compensation AND Benefits: Forms of Compensation Bases of CompensationDocument24 paginiCompensation AND Benefits: Forms of Compensation Bases of CompensationMaria LeeÎncă nu există evaluări

- Corporate Budget Circular No 23Document7 paginiCorporate Budget Circular No 23Tesa GDÎncă nu există evaluări

- Summary of Pensionary BenefitsDocument3 paginiSummary of Pensionary BenefitsAnonymous uFqb94BGzÎncă nu există evaluări

- Budget Analysis 2012Document26 paginiBudget Analysis 2012Rajpreet KaurÎncă nu există evaluări

- Pay CircularDocument1 paginăPay Circularvidhyaa1011Încă nu există evaluări

- G.O.Ms - No.3, Dated.19.1.2022 - Dearness AllowanceDocument8 paginiG.O.Ms - No.3, Dated.19.1.2022 - Dearness AllowanceVarshita HarshitÎncă nu există evaluări

- FixationDocument3 paginiFixationManjeet RanaÎncă nu există evaluări

- Subject: Amendments in Point of Taxation Rules, 2011 and Other Related ProvisionsDocument4 paginiSubject: Amendments in Point of Taxation Rules, 2011 and Other Related Provisionscool_321Încă nu există evaluări

- White Paper: Ministry of Finance, Trade and Economic PlanningDocument16 paginiWhite Paper: Ministry of Finance, Trade and Economic PlanningBonar StepanusÎncă nu există evaluări

- 1604 and OthersDocument86 pagini1604 and OthersBradley WhiteheadÎncă nu există evaluări

- How To Compute Withholding Tax On CompensationDocument7 paginiHow To Compute Withholding Tax On CompensationJessica GabejanÎncă nu există evaluări

- Spesifikasi Kaedah Pengiraan Berkomputer PCB 2015 Bi PDFDocument47 paginiSpesifikasi Kaedah Pengiraan Berkomputer PCB 2015 Bi PDFRHaikal Ming Zhi LeeÎncă nu există evaluări

- BMA Guidance On Restricting Pensions Tax Relief - October 2010Document6 paginiBMA Guidance On Restricting Pensions Tax Relief - October 2010fernandofloridoÎncă nu există evaluări

- Pay Fixation On PromotionDocument6 paginiPay Fixation On Promotionee_pod75% (4)

- Spending Review 2010 Policy Costings: October 2010Document35 paginiSpending Review 2010 Policy Costings: October 2010Bren-RÎncă nu există evaluări

- GO P 86 2011 PRC UniversityDocument63 paginiGO P 86 2011 PRC UniversitykgimoastateÎncă nu există evaluări

- Monthly Tax DeductionDocument47 paginiMonthly Tax DeductionLily JamesÎncă nu există evaluări

- Zencrack Installation and ExecutionDocument48 paginiZencrack Installation and ExecutionJu waÎncă nu există evaluări

- 1. Mạch điện đồng hồ santafe 2014-2018Document5 pagini1. Mạch điện đồng hồ santafe 2014-2018PRO ECUÎncă nu există evaluări

- Sears Canada: Electric DryerDocument10 paginiSears Canada: Electric Dryerquarz11100% (1)

- Honeymoon in Vegas Word FileDocument3 paginiHoneymoon in Vegas Word FileElenaÎncă nu există evaluări

- Monster Energy v. Jing - Counterfeit OpinionDocument9 paginiMonster Energy v. Jing - Counterfeit OpinionMark JaffeÎncă nu există evaluări

- Body Wash Base Guide Recipe PDFDocument2 paginiBody Wash Base Guide Recipe PDFTanmay PatelÎncă nu există evaluări

- Freedom SW 2000 Owners Guide (975-0528!01!01 - Rev-D)Document48 paginiFreedom SW 2000 Owners Guide (975-0528!01!01 - Rev-D)MatthewÎncă nu există evaluări

- Basic Definition of Manufacturing SystemDocument18 paginiBasic Definition of Manufacturing SystemRavenjoy ArcegaÎncă nu există evaluări

- Management of Odontogenic Infection of Primary Teeth in Child That Extends To The Submandibular and Submental Space Case ReportDocument5 paginiManagement of Odontogenic Infection of Primary Teeth in Child That Extends To The Submandibular and Submental Space Case ReportMel FAÎncă nu există evaluări

- Pre-Colonial Philippine ArtDocument5 paginiPre-Colonial Philippine Artpaulinavera100% (5)

- CPM Pert Multiple Choice Questions and AnswersDocument2 paginiCPM Pert Multiple Choice Questions and Answersptarwatkar123Încă nu există evaluări

- 2018-2021 VUMC Nursing Strategic Plan: Vision Core ValuesDocument1 pagină2018-2021 VUMC Nursing Strategic Plan: Vision Core ValuesAmeng GosimÎncă nu există evaluări

- Four Quartets: T.S. EliotDocument32 paginiFour Quartets: T.S. Eliotschwarzgerat00000100% (1)

- Action Research Intervention in English 9Document6 paginiAction Research Intervention in English 9Rey Kris Joy ApatanÎncă nu există evaluări

- Fractal Approach in RoboticsDocument20 paginiFractal Approach in RoboticsSmileyÎncă nu există evaluări

- ACCA Strategic Business Reporting (SBR) Workbook 2020Document840 paginiACCA Strategic Business Reporting (SBR) Workbook 2020Azba Nishath0% (1)

- Exercises: Use The Correct Form of Verbs in BracketsDocument3 paginiExercises: Use The Correct Form of Verbs in BracketsThủy NguyễnÎncă nu există evaluări

- Waste SM4500-NH3Document10 paginiWaste SM4500-NH3Sara ÖZGENÎncă nu există evaluări

- Train Collision Avoidance SystemDocument4 paginiTrain Collision Avoidance SystemSaurabh GuptaÎncă nu există evaluări

- AEC 34 - ACB Assignment: Module 1: Problem 1-1.TRUE OR FALSEDocument5 paginiAEC 34 - ACB Assignment: Module 1: Problem 1-1.TRUE OR FALSEDrew BanlutaÎncă nu există evaluări

- Book2Chapter10 and 11 EvaluationDocument55 paginiBook2Chapter10 and 11 EvaluationEmmanuel larbiÎncă nu există evaluări

- Nava LunchDocument3 paginiNava LuncheatlocalmenusÎncă nu există evaluări

- Packet Tracer - VLSM Design and Implementation Practice TopologyDocument3 paginiPacket Tracer - VLSM Design and Implementation Practice TopologyBenj MendozaÎncă nu există evaluări

- Lotte Advanced Materials Co., LTD.: ISO 9001:2015, KS Q ISO 9001:2015Document2 paginiLotte Advanced Materials Co., LTD.: ISO 9001:2015, KS Q ISO 9001:2015Tayyab KhanÎncă nu există evaluări

- Opening StrategyDocument6 paginiOpening StrategyashrafsekalyÎncă nu există evaluări

- Computer ArchitectureDocument46 paginiComputer Architecturejaime_parada3097100% (2)

- NBPME Part II 2008 Practice Tests 1-3Document49 paginiNBPME Part II 2008 Practice Tests 1-3Vinay Matai50% (2)

- AM2020-AFP1010 Installation Programming OperatingDocument268 paginiAM2020-AFP1010 Installation Programming OperatingBaron RicthenÎncă nu există evaluări

- LAC BrigadaDocument6 paginiLAC BrigadaRina Mae LopezÎncă nu există evaluări

- Slides 5 - Disposal and AppraisalDocument77 paginiSlides 5 - Disposal and AppraisalRave OcampoÎncă nu există evaluări

- Perversion of Justice: The Jeffrey Epstein StoryDe la EverandPerversion of Justice: The Jeffrey Epstein StoryEvaluare: 4.5 din 5 stele4.5/5 (10)

- For the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoDe la EverandFor the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoEvaluare: 4 din 5 stele4/5 (97)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismDe la EverandReading the Constitution: Why I Chose Pragmatism, not TextualismEvaluare: 4 din 5 stele4/5 (1)

- Summary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisDe la EverandSummary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisEvaluare: 4 din 5 stele4/5 (2)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDe la EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingEvaluare: 4.5 din 5 stele4.5/5 (98)

- Lady Killers: Deadly Women Throughout HistoryDe la EverandLady Killers: Deadly Women Throughout HistoryEvaluare: 4 din 5 stele4/5 (155)

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesDe la EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesÎncă nu există evaluări

- Hunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossDe la EverandHunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossEvaluare: 3.5 din 5 stele3.5/5 (6)

- All You Need to Know About the Music Business: Eleventh EditionDe la EverandAll You Need to Know About the Music Business: Eleventh EditionÎncă nu există evaluări

- The Law of the Land: The Evolution of Our Legal SystemDe la EverandThe Law of the Land: The Evolution of Our Legal SystemEvaluare: 4.5 din 5 stele4.5/5 (11)

- Reasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemDe la EverandReasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemEvaluare: 4 din 5 stele4/5 (25)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDe la EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorEvaluare: 4.5 din 5 stele4.5/5 (132)

- The Law Says What?: Stuff You Didn't Know About the Law (but Really Should!)De la EverandThe Law Says What?: Stuff You Didn't Know About the Law (but Really Should!)Evaluare: 4.5 din 5 stele4.5/5 (10)

- The Edge of Innocence: The Trial of Casper BennettDe la EverandThe Edge of Innocence: The Trial of Casper BennettEvaluare: 4.5 din 5 stele4.5/5 (3)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!De la EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Evaluare: 4.5 din 5 stele4.5/5 (14)

- Insider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorDe la EverandInsider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorEvaluare: 3.5 din 5 stele3.5/5 (3)

- All You Need to Know About the Music Business: 11th EditionDe la EverandAll You Need to Know About the Music Business: 11th EditionÎncă nu există evaluări

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageDe la EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageEvaluare: 2 din 5 stele2/5 (3)

- Dean Corll: The True Story of The Houston Mass MurdersDe la EverandDean Corll: The True Story of The Houston Mass MurdersEvaluare: 4 din 5 stele4/5 (29)

- The Articulate Advocate: Persuasive Skills for Lawyers in Trials, Appeals, Arbitrations, and MotionsDe la EverandThe Articulate Advocate: Persuasive Skills for Lawyers in Trials, Appeals, Arbitrations, and MotionsEvaluare: 5 din 5 stele5/5 (5)

- A Contractor's Guide to the FIDIC Conditions of ContractDe la EverandA Contractor's Guide to the FIDIC Conditions of ContractÎncă nu există evaluări

- Chokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackDe la EverandChokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackEvaluare: 5 din 5 stele5/5 (20)

- Beyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceDe la EverandBeyond the Body Farm: A Legendary Bone Detective Explores Murders, Mysteries, and the Revolution in Forensic ScienceEvaluare: 4 din 5 stele4/5 (107)

- The Internet Con: How to Seize the Means of ComputationDe la EverandThe Internet Con: How to Seize the Means of ComputationEvaluare: 5 din 5 stele5/5 (6)