S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- BT - Cat35fr005 - Field Report LaafDocument21 paginiBT - Cat35fr005 - Field Report LaafFabianoBorg100% (2)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- ALVProgramming GuideDocument46 paginiALVProgramming GuideManmeet SinghÎncă nu există evaluări

- ALVProgramming GuideDocument46 paginiALVProgramming GuideManmeet SinghÎncă nu există evaluări

- ABAP AlvDocument532 paginiABAP AlvJelli ArchanaÎncă nu există evaluări

- ABAP AlvDocument532 paginiABAP AlvJelli ArchanaÎncă nu există evaluări

- Understanding Production Order VarianceDocument21 paginiUnderstanding Production Order VarianceveysiyigitÎncă nu există evaluări

- Taylor Campbell FeatureDocument5 paginiTaylor Campbell Featureapi-666625755Încă nu există evaluări

- The Landmarks of MartinismDocument7 paginiThe Landmarks of Martinismcarlos incognitosÎncă nu există evaluări

- Foucault Truth and Power InterviewDocument7 paginiFoucault Truth and Power IntervieweastbayseiÎncă nu există evaluări

- Face Reading NotesDocument8 paginiFace Reading NotesNabeel TirmaziÎncă nu există evaluări

- St. Stephen's Association V CIRDocument3 paginiSt. Stephen's Association V CIRPatricia GonzagaÎncă nu există evaluări

- ABAP Code Sample To Edit ALV GridDocument12 paginiABAP Code Sample To Edit ALV GridAnil GadiparthiÎncă nu există evaluări

- ABAP Code Sample To Edit ALV GridDocument12 paginiABAP Code Sample To Edit ALV GridAnil GadiparthiÎncă nu există evaluări

- ABAP Code Sample To Edit ALV GridDocument12 paginiABAP Code Sample To Edit ALV GridAnil GadiparthiÎncă nu există evaluări

- SAP CO Product Cost Controlling Transaction CodesDocument25 paginiSAP CO Product Cost Controlling Transaction CodesveysiyigitÎncă nu există evaluări

- Open Data Driving Growth Ingenuity and InnovationDocument36 paginiOpen Data Driving Growth Ingenuity and InnovationAnonymous EBlYNQbiMyÎncă nu există evaluări

- GUBAnt BanwnaDocument36 paginiGUBAnt BanwnaMarc Philip100% (1)

- G.R. No. 172242Document2 paginiG.R. No. 172242Eap Bustillo67% (3)

- CoA Judgment - Kwan Ngen Wah V Julita Binti TinggalDocument25 paginiCoA Judgment - Kwan Ngen Wah V Julita Binti TinggalSerzan HassnarÎncă nu există evaluări

- KB61 - Repost Line Items: Cost Center Accounting Cost Center AccountingDocument6 paginiKB61 - Repost Line Items: Cost Center Accounting Cost Center AccountingveysiyigitÎncă nu există evaluări

- TCODE - KSVB - Execute - Plan - Cost - DistributionDocument5 paginiTCODE - KSVB - Execute - Plan - Cost - DistributionrajdeeppawarÎncă nu există evaluări

- Execute Plan Cost AssessmentDocument7 paginiExecute Plan Cost AssessmentveysiyigitÎncă nu există evaluări

- Execute Plan Cost SplittingDocument9 paginiExecute Plan Cost SplittingveysiyigitÎncă nu există evaluări

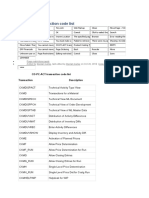

- CO-PC-ACT Transaction Code ListDocument5 paginiCO-PC-ACT Transaction Code ListveysiyigitÎncă nu există evaluări

- Conditionally Assigning Colors and Input Enable To ALV Columns in Web Dynpro ABAPDocument7 paginiConditionally Assigning Colors and Input Enable To ALV Columns in Web Dynpro ABAPLuboš AutrataÎncă nu există evaluări

- Alv Documentation and Examples11 by Rajagopalan. MDocument35 paginiAlv Documentation and Examples11 by Rajagopalan. MJaya SankarÎncă nu există evaluări

- Customize ALV Grid Reports in SAPDocument7 paginiCustomize ALV Grid Reports in SAPfdizaÎncă nu există evaluări

- ALV Row EditableDocument9 paginiALV Row Editablevijay_agarwal82Încă nu există evaluări

- Alv Grid List Using Radio ButtonsDocument12 paginiAlv Grid List Using Radio ButtonsNakul Sree FriendÎncă nu există evaluări

- Alv OverviewDocument14 paginiAlv OverviewGaurav BansalÎncă nu există evaluări

- Oops ProgramDocument6 paginiOops ProgramNakul Sree FriendÎncă nu există evaluări

- Alv OverviewDocument14 paginiAlv OverviewGaurav BansalÎncă nu există evaluări

- ALV Row EditableDocument9 paginiALV Row Editablevijay_agarwal82Încă nu există evaluări

- Alv Grid List Using Radio ButtonsDocument12 paginiAlv Grid List Using Radio ButtonsNakul Sree FriendÎncă nu există evaluări

- Oops ProgramDocument6 paginiOops ProgramNakul Sree FriendÎncă nu există evaluări

- Customize ALV Grid Reports in SAPDocument7 paginiCustomize ALV Grid Reports in SAPfdizaÎncă nu există evaluări

- Conditionally Assigning Colors and Input Enable To ALV Columns in Web Dynpro ABAPDocument7 paginiConditionally Assigning Colors and Input Enable To ALV Columns in Web Dynpro ABAPLuboš AutrataÎncă nu există evaluări

- Alv Documentation and Examples11 by Rajagopalan. MDocument35 paginiAlv Documentation and Examples11 by Rajagopalan. MJaya SankarÎncă nu există evaluări

- Oops ProgramDocument6 paginiOops ProgramNakul Sree FriendÎncă nu există evaluări

- Alv OverviewDocument14 paginiAlv OverviewGaurav BansalÎncă nu există evaluări

- Sunat PerempuanDocument8 paginiSunat PerempuanJamaluddin MohammadÎncă nu există evaluări

- Contemporary Management Education: Piet NaudéDocument147 paginiContemporary Management Education: Piet Naudérolorot958Încă nu există evaluări

- 3rd Yr 2nd Sem Business Plan Preparation Quiz 1 MidtermDocument14 pagini3rd Yr 2nd Sem Business Plan Preparation Quiz 1 MidtermAlfie Jaicten SyÎncă nu există evaluări

- Clearlake City Council PacketDocument57 paginiClearlake City Council PacketLakeCoNewsÎncă nu există evaluări

- The Impact of E-Commerce in BangladeshDocument12 paginiThe Impact of E-Commerce in BangladeshMd Ruhul AminÎncă nu există evaluări

- Satyam PPT FinalDocument16 paginiSatyam PPT FinalBhumika ThakkarÎncă nu există evaluări

- AIDA Model in AdvertisingDocument3 paginiAIDA Model in AdvertisingHằng PhạmÎncă nu există evaluări

- Appendix F - Property ValueDocument11 paginiAppendix F - Property ValueTown of Colonie LandfillÎncă nu există evaluări

- Fundamentals of Accountancy, Business and Management 1 (FABM1)Document9 paginiFundamentals of Accountancy, Business and Management 1 (FABM1)A.Încă nu există evaluări

- Web Design Wordpress - Hosting Services ListDocument1 paginăWeb Design Wordpress - Hosting Services ListMotivatioNetÎncă nu există evaluări

- Uttarakhand NTSE 2021 Stage 1 MAT and SAT Question and SolutionsDocument140 paginiUttarakhand NTSE 2021 Stage 1 MAT and SAT Question and SolutionsAchyut SinghÎncă nu există evaluări

- The Powers To Lead Joseph S. Nye Jr.Document18 paginiThe Powers To Lead Joseph S. Nye Jr.George ForcoșÎncă nu există evaluări

- Education Secretaries 10Document6 paginiEducation Secretaries 10Patrick AdamsÎncă nu există evaluări

- Intercultural Presentation FinalDocument15 paginiIntercultural Presentation Finalapi-302652884Încă nu există evaluări

- Bio New KMJDocument11 paginiBio New KMJapi-19758547Încă nu există evaluări

- Heaven and Hell in The ScripturesDocument3 paginiHeaven and Hell in The ScripturesOvidiu PopescuÎncă nu există evaluări

- Memorandum Personnel Memo 21-11 To:: A B G D. WDocument2 paginiMemorandum Personnel Memo 21-11 To:: A B G D. WLEX18NewsÎncă nu există evaluări

- 1Document3 pagini1Ashok KumarÎncă nu există evaluări

- LG Overnight Trader Q3 2019 EST PDFDocument11 paginiLG Overnight Trader Q3 2019 EST PDFjim6116Încă nu există evaluări

- Classical Philosophies Guide Business Ethics DecisionsDocument48 paginiClassical Philosophies Guide Business Ethics DecisionsDanielyn GestopaÎncă nu există evaluări