S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- CFA MindmapDocument98 paginiCFA MindmapHongjun Yin92% (12)

- 19 Ways To Find Fast Cash, More Savings - NerdWalletDocument10 pagini19 Ways To Find Fast Cash, More Savings - NerdWalletGeorgios MoulkasÎncă nu există evaluări

- MCQDocument4 paginiMCQLouina YnciertoÎncă nu există evaluări

- Q&A - Case1Document2 paginiQ&A - Case1Daniele StrozzieriÎncă nu există evaluări

- RR No. 2-98 (As Amended by TRAIN Law)Document125 paginiRR No. 2-98 (As Amended by TRAIN Law)Magenic Manila IncÎncă nu există evaluări

- Building Strategy and Performance Through Time: The Critical PathDocument19 paginiBuilding Strategy and Performance Through Time: The Critical PathBusiness Expert PressÎncă nu există evaluări

- Investment Analysis Polar Sports ADocument9 paginiInvestment Analysis Polar Sports AtalabreÎncă nu există evaluări

- MCQ Chapter 1-9Document36 paginiMCQ Chapter 1-9rupok96% (27)

- Marketing PlanDocument51 paginiMarketing PlanSukh RajputÎncă nu există evaluări

- Director of Consulting Sample Resume From Freedom ResumesDocument2 paginiDirector of Consulting Sample Resume From Freedom ResumesFreedom Resumes100% (1)

- En Cima Appendix - 3Document1 paginăEn Cima Appendix - 3api-3838281Încă nu există evaluări

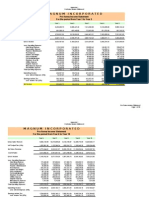

- Magnum Financial FinalDocument27 paginiMagnum Financial Finalapi-3838281Încă nu există evaluări

- En Cima Appendix - 5Document5 paginiEn Cima Appendix - 5api-3838281Încă nu există evaluări

- En Cima Market StudyDocument67 paginiEn Cima Market Studyapi-3838281100% (2)

- En Cima Appendix - 4Document2 paginiEn Cima Appendix - 4api-3838281Încă nu există evaluări

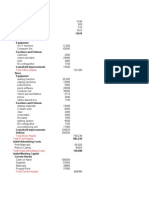

- Magnum Final Finally FsDocument30 paginiMagnum Final Finally Fsapi-3838281Încă nu există evaluări

- My Part For Report FinalDocument4 paginiMy Part For Report Finalapi-3838281Încă nu există evaluări

- Power Point - MarketingDocument11 paginiPower Point - Marketingapi-3838281Încă nu există evaluări

- En Cima Appendix - 2Document2 paginiEn Cima Appendix - 2api-3838281Încă nu există evaluări

- Power PointDocument7 paginiPower Pointapi-3838281Încă nu există evaluări

- Power Point - Market Demand ComputationDocument9 paginiPower Point - Market Demand Computationapi-3838281100% (1)

- RRJ JeansDocument1 paginăRRJ Jeansapi-3838281100% (1)

- Power Point TechnicalDocument9 paginiPower Point Technicalapi-3838281Încă nu există evaluări

- Pant SaloonDocument27 paginiPant Saloonapi-3838281Încă nu există evaluări

- Denim Sewing GuidelinesDocument3 paginiDenim Sewing Guidelinesapi-3838281Încă nu există evaluări

- Technical Appraisal Table of ContentsDocument5 paginiTechnical Appraisal Table of Contentsapi-3838281Încă nu există evaluări

- My Part For ReportDocument5 paginiMy Part For Reportapi-3838281Încă nu există evaluări

- Org Structure - HR Matters - Daily OpernsDocument10 paginiOrg Structure - HR Matters - Daily Opernsapi-3838281Încă nu există evaluări

- Pattern For Org StructureDocument8 paginiPattern For Org Structureapi-3838281Încă nu există evaluări

- Technical AppraisalDocument64 paginiTechnical Appraisalapi-3838281Încă nu există evaluări

- WE'RE NOT Sweatshops - Garments Exporters Worry About Int'l ImageDocument2 paginiWE'RE NOT Sweatshops - Garments Exporters Worry About Int'l Imageapi-3838281Încă nu există evaluări

- Viktor JeansDocument2 paginiViktor Jeansapi-3838281Încă nu există evaluări

- The Philippine Garments IndustryDocument4 paginiThe Philippine Garments Industryapi-3838281100% (3)

- Technical Appraisal FinalDocument67 paginiTechnical Appraisal Finalapi-3838281Încă nu există evaluări

- Operating CostsDocument13 paginiOperating Costsapi-3838281Încă nu există evaluări

- Plains and PrintsDocument2 paginiPlains and Printsapi-3838281100% (3)

- RectoDocument2 paginiRectoapi-3838281Încă nu există evaluări

- June Garments Exports Adjust To PriceDocument2 paginiJune Garments Exports Adjust To Priceapi-3838281Încă nu există evaluări

- PIF2006Document57 paginiPIF2006api-3838281Încă nu există evaluări

- Philippines Cotton and Products Annual 2004Document3 paginiPhilippines Cotton and Products Annual 2004api-3838281Încă nu există evaluări

- The Information Approach To Decision UsefulnessDocument26 paginiThe Information Approach To Decision UsefulnessDiny Fariha ZakhirÎncă nu există evaluări

- Solution StarbucksDocument3 paginiSolution StarbucksMrityunjay Kumar PandayÎncă nu există evaluări

- More Solved Examples PDFDocument16 paginiMore Solved Examples PDFrobbsÎncă nu există evaluări

- Fundamental Analysis and Its Impact On Insurance SectorDocument103 paginiFundamental Analysis and Its Impact On Insurance Sectorsebijo8750% (6)

- Chap 04 and 05 (Mini Case)Document18 paginiChap 04 and 05 (Mini Case)ricky setiawan100% (1)

- What - If Using ExcelDocument17 paginiWhat - If Using ExcelcathycharmedxÎncă nu există evaluări

- Beneish N Nichols.2005Document60 paginiBeneish N Nichols.2005Shanti PertiwiÎncă nu există evaluări

- Section 247. General Provisions. - : Sections 247-252, Tax CodeDocument2 paginiSection 247. General Provisions. - : Sections 247-252, Tax CodeEdward Kenneth KungÎncă nu există evaluări

- Income Tax On Intraday TradingDocument7 paginiIncome Tax On Intraday Tradingkrutarth patelÎncă nu există evaluări

- Financial Accounting Part 2Document5 paginiFinancial Accounting Part 2Christopher Price0% (1)

- Bank Alfalah Limited: That Appear in Reliable Third-Party PublicationsDocument15 paginiBank Alfalah Limited: That Appear in Reliable Third-Party PublicationsChanchal KuriÎncă nu există evaluări

- Mind Map Chapter 3 and 4 OutlineDocument2 paginiMind Map Chapter 3 and 4 OutlinePatricia SantosÎncă nu există evaluări

- Income From Other SourceDocument20 paginiIncome From Other SourceRewant MehraÎncă nu există evaluări

- Nguyen Huong A 12Document8 paginiNguyen Huong A 12Quỳnh Hương NguyễnÎncă nu există evaluări

- Financial Analysis of Fauji Cement LTDDocument27 paginiFinancial Analysis of Fauji Cement LTDMBA...KIDÎncă nu există evaluări

- Current Liabilities and Payroll AccountingDocument17 paginiCurrent Liabilities and Payroll AccountingEla PelariÎncă nu există evaluări

- Gina Balance SheetDocument4 paginiGina Balance SheetNawshin DastagirÎncă nu există evaluări

- The Accounting Process (Part 1) : Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriDocument46 paginiThe Accounting Process (Part 1) : Ninia C. Pauig-Lumauan, MBA, CPA Lyceum of AparriTessang OnongenÎncă nu există evaluări

- Income StatementDocument1 paginăIncome StatementYOHANAÎncă nu există evaluări