S-ar putea să vă placă și

- Real Estate Community Digital Guide Book 3RD EditionDe la EverandReal Estate Community Digital Guide Book 3RD EditionÎncă nu există evaluări

- Amended RBPF PolicyDocument2 paginiAmended RBPF Policynfk roeÎncă nu există evaluări

- Implications of CDR Sanction TermsDocument4 paginiImplications of CDR Sanction Termsrao_gmailÎncă nu există evaluări

- Retail Banking AdvancesDocument38 paginiRetail Banking AdvancesShruti SrivastavaÎncă nu există evaluări

- Faq - 3Document11 paginiFaq - 3nani baradiÎncă nu există evaluări

- Chapter 1: The Principles of Lending and Lending BasicsDocument5 paginiChapter 1: The Principles of Lending and Lending Basicshesham zakiÎncă nu există evaluări

- Loan Transfer, Syndication - Niket KhandelwalDocument13 paginiLoan Transfer, Syndication - Niket Khandelwalaman.saini20Încă nu există evaluări

- Unit-6: Commercial & Industrial LendingDocument28 paginiUnit-6: Commercial & Industrial LendingRaaz Key Run ChhatkuliÎncă nu există evaluări

- Credit PlanningDocument9 paginiCredit PlanningMonika Saini100% (1)

- Tutorial 1 AnswerDocument6 paginiTutorial 1 AnswerPuteri XjadiÎncă nu există evaluări

- Lecture 3 - Loans & AdvancesDocument16 paginiLecture 3 - Loans & AdvancesEmmanuel MwapeÎncă nu există evaluări

- Lecture 3 - Loans - AdvancesDocument16 paginiLecture 3 - Loans - AdvancesYvonneÎncă nu există evaluări

- A Study On Credit Management at District CoDocument86 paginiA Study On Credit Management at District CoIMAM JAVOOR100% (2)

- Commercial and Industrial LoansDocument36 paginiCommercial and Industrial LoansAngela ChuaÎncă nu există evaluări

- Business FinanceDocument13 paginiBusiness FinanceThone Gregor VisayaÎncă nu există evaluări

- MBASummaryof Dodd FrankDocument17 paginiMBASummaryof Dodd FrankbplivecchiÎncă nu există evaluări

- Report On Working Capital Loan (Prime Bank)Document29 paginiReport On Working Capital Loan (Prime Bank)rrashadatt100% (3)

- Loan Policy PDFDocument3 paginiLoan Policy PDFVeeru Mudiraj0% (1)

- Project Report Format For Bank LoanDocument7 paginiProject Report Format For Bank LoanRaju Ramjeli70% (10)

- It Can Be Identified 4 Basic Scenarios When Rescheduling A LoanDocument4 paginiIt Can Be Identified 4 Basic Scenarios When Rescheduling A LoanMd Salah UddinÎncă nu există evaluări

- L15 Consumer Loans Credit CardsDocument18 paginiL15 Consumer Loans Credit CardsJAY SHUKLAÎncă nu există evaluări

- Pamantasan NG Lungsod NG Maynila PLM Business School A.Y. 2020 - 2021 First Semester Fin 3104: Credit Management and Collection PoliciesDocument29 paginiPamantasan NG Lungsod NG Maynila PLM Business School A.Y. 2020 - 2021 First Semester Fin 3104: Credit Management and Collection PoliciesHarlene BulaongÎncă nu există evaluări

- Working Capital ManagementDocument16 paginiWorking Capital ManagementAmit RoyÎncă nu există evaluări

- Loan and AdvancesDocument9 paginiLoan and AdvancesSumit NaugraiyaÎncă nu există evaluări

- VN Projects - S.Resources - QuestionnairesDocument3 paginiVN Projects - S.Resources - QuestionnairesAZHAR HASANÎncă nu există evaluări

- Chapter - Ii Review of Literature: Personal Debt Management: A Study Related To Urban Household's Debt Servicing BurdenDocument20 paginiChapter - Ii Review of Literature: Personal Debt Management: A Study Related To Urban Household's Debt Servicing BurdenSakshi BathlaÎncă nu există evaluări

- SBI Car Loan - Jan 2012Document17 paginiSBI Car Loan - Jan 2012mevrick_guyÎncă nu există evaluări

- Credit AppraisalDocument6 paginiCredit Appraisalnhan thanhÎncă nu există evaluări

- J. Peralta: Bpi V. Bpi Employees Union-Metro ManilaDocument3 paginiJ. Peralta: Bpi V. Bpi Employees Union-Metro ManilaCamille BritanicoÎncă nu există evaluări

- What Are The 5 C's of Credit?: Key TakeawaysDocument3 paginiWhat Are The 5 C's of Credit?: Key TakeawaysUSMANÎncă nu există evaluări

- University of Michigan Pat Hammett Six Sigma Program: The Life of A Mortgage Loan Case Study OverviewDocument4 paginiUniversity of Michigan Pat Hammett Six Sigma Program: The Life of A Mortgage Loan Case Study OverviewNaveen KumarÎncă nu există evaluări

- Bank CreditDocument5 paginiBank Creditnhan thanhÎncă nu există evaluări

- Credit AdministrationDocument5 paginiCredit AdministrationCarl AbruquahÎncă nu există evaluări

- Unit-II - nOTESDocument20 paginiUnit-II - nOTESMohammad ShahvanÎncă nu există evaluări

- 1.1 Introduction To Reverse MortgageDocument20 pagini1.1 Introduction To Reverse MortgageSandeep SandhuÎncă nu există evaluări

- Highlights of Proposed Ability-To-Repay RulesDocument3 paginiHighlights of Proposed Ability-To-Repay RulesForeclosure FraudÎncă nu există evaluări

- Chapter 08 Loans & Advances (Law & Practice of Banking)Document9 paginiChapter 08 Loans & Advances (Law & Practice of Banking)Rayyah AminÎncă nu există evaluări

- 2 Principles+of+LendingDocument25 pagini2 Principles+of+LendingBratati SahooÎncă nu există evaluări

- NHB Guidelines On RMLDocument8 paginiNHB Guidelines On RMLsreejit.mohanty4016Încă nu există evaluări

- Credit Appraisal and Non-Performing Assets Dr.P.Shanmukha Rao Dr.N.V.S.SuryanarayanaDocument8 paginiCredit Appraisal and Non-Performing Assets Dr.P.Shanmukha Rao Dr.N.V.S.SuryanarayanaImam AnnigeriÎncă nu există evaluări

- Credit, Collection and Compliance Application 1 - Introduction To CreditDocument5 paginiCredit, Collection and Compliance Application 1 - Introduction To CreditGabriel Matthew Lanzarfel GabudÎncă nu există evaluări

- CLD - BAO3404 TUTORIAL GUIDE WordDocument49 paginiCLD - BAO3404 TUTORIAL GUIDE WordShi MingÎncă nu există evaluări

- Bank Lending and Credit A DministrationDocument5 paginiBank Lending and Credit A Dministrationolikagu patrickÎncă nu există evaluări

- SLEM Proposed Policy On Collateral For Salary-Based LoansDocument4 paginiSLEM Proposed Policy On Collateral For Salary-Based LoansMoira Enegue AbenioÎncă nu există evaluări

- FindingsDocument5 paginiFindingsafifÎncă nu există evaluări

- Unit 2 Trade Credit RiskDocument15 paginiUnit 2 Trade Credit Risksaurabh thakurÎncă nu există evaluări

- General Banking - IIDocument6 paginiGeneral Banking - IIPallaviprasad kasturiÎncă nu există evaluări

- Mortgage Loans in IndiaDocument11 paginiMortgage Loans in IndiaDebobrata MajumdarÎncă nu există evaluări

- Consumer Act Q and ADocument4 paginiConsumer Act Q and ATine TineÎncă nu există evaluări

- A Study On Loans and Advances by Rohit RDocument91 paginiA Study On Loans and Advances by Rohit RChandrashekhar GurnuleÎncă nu există evaluări

- Devaiya Nikhil LDRP - Itr MbaDocument5 paginiDevaiya Nikhil LDRP - Itr MbaKaushik PatelÎncă nu există evaluări

- UntitledDocument24 paginiUntitledEric JohnsonÎncă nu există evaluări

- Damodaram Sanjivayya National Law University Visakhapatnam, A.P., IndiaDocument28 paginiDamodaram Sanjivayya National Law University Visakhapatnam, A.P., Indialeela naga janaki rajitha attiliÎncă nu există evaluări

- Business LoansDocument4 paginiBusiness LoansHimmanshu SabharwalÎncă nu există evaluări

- Loans and Advances - IRCBDocument68 paginiLoans and Advances - IRCBDr Linda Mary Simon100% (1)

- Direct Pay Letter of Credit Loan DPLC Program 530708Document4 paginiDirect Pay Letter of Credit Loan DPLC Program 530708Zainul Fikri TampengÎncă nu există evaluări

- Banking: Islamic Banking: Institute of Business Administration (Iba), JuDocument8 paginiBanking: Islamic Banking: Institute of Business Administration (Iba), JuYeasminAkterÎncă nu există evaluări

- Summary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActDocument16 paginiSummary of Mortgage Related Provisions of The Dodd-Frank Wall Street Reform and Consumer Protection ActPaula HillockÎncă nu există evaluări

- A Study On Loans and Advances by Rohit RDocument178 paginiA Study On Loans and Advances by Rohit RIram Fatmah100% (1)

- Sacco Lending Policies and GuidelinesDocument39 paginiSacco Lending Policies and GuidelinesKivumbi William90% (111)

- En Cima Appendix - 3Document1 paginăEn Cima Appendix - 3api-3838281Încă nu există evaluări

- Magnum Financial FinalDocument27 paginiMagnum Financial Finalapi-3838281Încă nu există evaluări

- En Cima Appendix - 5Document5 paginiEn Cima Appendix - 5api-3838281Încă nu există evaluări

- En Cima Market StudyDocument67 paginiEn Cima Market Studyapi-3838281100% (2)

- En Cima Appendix - 4Document2 paginiEn Cima Appendix - 4api-3838281Încă nu există evaluări

- Magnum Final Finally FsDocument30 paginiMagnum Final Finally Fsapi-3838281Încă nu există evaluări

- My Part For Report FinalDocument4 paginiMy Part For Report Finalapi-3838281Încă nu există evaluări

- Power Point - MarketingDocument11 paginiPower Point - Marketingapi-3838281Încă nu există evaluări

- En Cima Appendix - 2Document2 paginiEn Cima Appendix - 2api-3838281Încă nu există evaluări

- Power PointDocument7 paginiPower Pointapi-3838281Încă nu există evaluări

- Power Point - Market Demand ComputationDocument9 paginiPower Point - Market Demand Computationapi-3838281100% (1)

- RRJ JeansDocument1 paginăRRJ Jeansapi-3838281100% (1)

- Power Point TechnicalDocument9 paginiPower Point Technicalapi-3838281Încă nu există evaluări

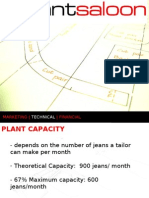

- Pant SaloonDocument27 paginiPant Saloonapi-3838281Încă nu există evaluări

- Denim Sewing GuidelinesDocument3 paginiDenim Sewing Guidelinesapi-3838281Încă nu există evaluări

- Technical Appraisal Table of ContentsDocument5 paginiTechnical Appraisal Table of Contentsapi-3838281Încă nu există evaluări

- My Part For ReportDocument5 paginiMy Part For Reportapi-3838281Încă nu există evaluări

- Org Structure - HR Matters - Daily OpernsDocument10 paginiOrg Structure - HR Matters - Daily Opernsapi-3838281Încă nu există evaluări

- Pattern For Org StructureDocument8 paginiPattern For Org Structureapi-3838281Încă nu există evaluări

- Technical AppraisalDocument64 paginiTechnical Appraisalapi-3838281Încă nu există evaluări

- WE'RE NOT Sweatshops - Garments Exporters Worry About Int'l ImageDocument2 paginiWE'RE NOT Sweatshops - Garments Exporters Worry About Int'l Imageapi-3838281Încă nu există evaluări

- Viktor JeansDocument2 paginiViktor Jeansapi-3838281Încă nu există evaluări

- The Philippine Garments IndustryDocument4 paginiThe Philippine Garments Industryapi-3838281100% (3)

- Technical Appraisal FinalDocument67 paginiTechnical Appraisal Finalapi-3838281Încă nu există evaluări

- Operating CostsDocument13 paginiOperating Costsapi-3838281Încă nu există evaluări

- Plains and PrintsDocument2 paginiPlains and Printsapi-3838281100% (3)

- RectoDocument2 paginiRectoapi-3838281Încă nu există evaluări

- June Garments Exports Adjust To PriceDocument2 paginiJune Garments Exports Adjust To Priceapi-3838281Încă nu există evaluări

- PIF2006Document57 paginiPIF2006api-3838281Încă nu există evaluări

- Philippines Cotton and Products Annual 2004Document3 paginiPhilippines Cotton and Products Annual 2004api-3838281Încă nu există evaluări

- AFAR 1.0 Partnership-Accounting ASSESSMENTDocument5 paginiAFAR 1.0 Partnership-Accounting ASSESSMENTMakisa YuÎncă nu există evaluări

- Securities Regulation HyposDocument46 paginiSecurities Regulation HyposErin JacksonÎncă nu există evaluări

- Entrepreneurial Finance - Luisa AlemanyDocument648 paginiEntrepreneurial Finance - Luisa Alemanytea.liuyudanÎncă nu există evaluări

- Functions of Treasury MGTDocument5 paginiFunctions of Treasury MGTk-911Încă nu există evaluări

- Junior Accountant RoleDocument1 paginăJunior Accountant RoleRICARDO PROMOTIONÎncă nu există evaluări

- AD312 Sample Final Exam 2020 (With Answers)Document2 paginiAD312 Sample Final Exam 2020 (With Answers)Ekin MadenÎncă nu există evaluări

- Viacom18 Gears Up For IPL Ex-Star Head Uday Shankar To Likely Drive Digital Initiatives?Document3 paginiViacom18 Gears Up For IPL Ex-Star Head Uday Shankar To Likely Drive Digital Initiatives?bdacÎncă nu există evaluări

- WFP Cash and Vouchers ManualDocument92 paginiWFP Cash and Vouchers ManualSoroush AsifÎncă nu există evaluări

- GR 11 Accounting P2 (English) November 2022 Question PaperDocument14 paginiGR 11 Accounting P2 (English) November 2022 Question Paperphafane2020Încă nu există evaluări

- Power of AttorneyDocument3 paginiPower of Attorneyjames brownÎncă nu există evaluări

- Ipsas 24 BudgetDocument2 paginiIpsas 24 Budgetritunath100% (1)

- Accounting For Decision Making Mid TermDocument5 paginiAccounting For Decision Making Mid Termumer12Încă nu există evaluări

- The Bankers Own The EarthDocument51 paginiThe Bankers Own The EarthIanSmith777100% (3)

- Pivot Boss SummaryDocument36 paginiPivot Boss SummaryVarun Vasurendran100% (2)

- AmazonFile 0Document2 paginiAmazonFile 0chawllarohitÎncă nu există evaluări

- Fae3e SM ch02Document42 paginiFae3e SM ch02JarkeeÎncă nu există evaluări

- Ocbc Ar2016 Full Report English PDFDocument236 paginiOcbc Ar2016 Full Report English PDFMr TanÎncă nu există evaluări

- Kuwait Finance House AustDocument2 paginiKuwait Finance House AustchairunnisanovÎncă nu există evaluări

- Malaysian Airline System Berhad Annual Report 04/05 (10601-W)Document87 paginiMalaysian Airline System Berhad Annual Report 04/05 (10601-W)Nur AfiqahÎncă nu există evaluări

- SP PaperDocument11 paginiSP Paper9137373282abcdÎncă nu există evaluări

- Cost of Capital ChapterDocument25 paginiCost of Capital ChapterHossain Belal100% (1)

- Alem Ketema Proposal NewDocument25 paginiAlem Ketema Proposal NewLeulÎncă nu există evaluări

- UntitledDocument267 paginiUntitledGaurav KothariÎncă nu există evaluări

- Malaysia and The Global Financial Crisis, The Case of Malaysia As A Plan-Rationality State in Responding The CrisisDocument22 paginiMalaysia and The Global Financial Crisis, The Case of Malaysia As A Plan-Rationality State in Responding The CrisisErika Angelika60% (5)

- BSBCRT611 BriefDocument2 paginiBSBCRT611 BriefJohnÎncă nu există evaluări

- Chapter 6 Mankiw (Macroeconomics)Document36 paginiChapter 6 Mankiw (Macroeconomics)andrew myintmyat100% (1)

- PGI Sample QuestionDocument4 paginiPGI Sample QuestionleoneseÎncă nu există evaluări

- Arvog Finance Corporate Presentation 2022Document9 paginiArvog Finance Corporate Presentation 2022Dinesh KandpalÎncă nu există evaluări

- Workshop 2 AccountingDocument6 paginiWorkshop 2 AccountingJulieth CaviativaÎncă nu există evaluări

- Finance Basics (HBR 20-Minute Manager Series)De la EverandFinance Basics (HBR 20-Minute Manager Series)Evaluare: 4.5 din 5 stele4.5/5 (32)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De la EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Evaluare: 4.5 din 5 stele4.5/5 (13)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)De la EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Evaluare: 4.5 din 5 stele4.5/5 (5)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyDe la EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyEvaluare: 4.5 din 5 stele4.5/5 (37)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe la EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindEvaluare: 5 din 5 stele5/5 (231)

- Ledger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceDe la EverandLedger Legends: A Bookkeeper's Handbook for Financial Success: Navigating the World of Business Finances with ConfidenceÎncă nu există evaluări

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantDe la EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantEvaluare: 4.5 din 5 stele4.5/5 (146)

- Getting to Yes: How to Negotiate Agreement Without Giving InDe la EverandGetting to Yes: How to Negotiate Agreement Without Giving InEvaluare: 4 din 5 stele4/5 (652)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDe la EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyEvaluare: 5 din 5 stele5/5 (1)

- Bookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesDe la EverandBookkeeping: A Beginner’s Guide to Accounting and Bookkeeping for Small BusinessesEvaluare: 5 din 5 stele5/5 (4)

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageDe la EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageEvaluare: 4.5 din 5 stele4.5/5 (109)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)De la EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Evaluare: 4.5 din 5 stele4.5/5 (24)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)De la EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Evaluare: 4 din 5 stele4/5 (33)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe la Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelÎncă nu există evaluări

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsDe la EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsEvaluare: 4 din 5 stele4/5 (4)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe la EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItEvaluare: 5 din 5 stele5/5 (13)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDe la EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineÎncă nu există evaluări

- Financial Accounting For Dummies: 2nd EditionDe la EverandFinancial Accounting For Dummies: 2nd EditionEvaluare: 5 din 5 stele5/5 (10)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe la EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesÎncă nu există evaluări

- Accounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)De la EverandAccounting Principles: Learn The Simple and Effective Methods of Basic Accounting And Bookkeeping Using This comprehensive Guide for Beginners(quick-books,made simple,easy,managerial,finance)Evaluare: 4.5 din 5 stele4.5/5 (5)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeDe la EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeEvaluare: 4 din 5 stele4/5 (21)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessDe la EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessEvaluare: 4.5 din 5 stele4.5/5 (28)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDe la EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetÎncă nu există evaluări