S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Advanced Derivatives CourseDocument16 paginiAdvanced Derivatives CourseGautam Chaini100% (1)

- Advanced Derivatives Course Chapter 6Document17 paginiAdvanced Derivatives Course Chapter 6api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 7Document2 paginiAdvanced Derivatives Course Chapter 7api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 5Document17 paginiAdvanced Derivatives Course Chapter 5api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 3Document8 paginiAdvanced Derivatives Course Chapter 3api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 4Document10 paginiAdvanced Derivatives Course Chapter 4api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 2Document14 paginiAdvanced Derivatives Course Chapter 2api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 11Document10 paginiAdvanced Derivatives Course Chapter 11api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 10Document15 paginiAdvanced Derivatives Course Chapter 10api-3841270Încă nu există evaluări

- Advanced Derivatives Course Chapter 1Document6 paginiAdvanced Derivatives Course Chapter 1api-3841270Încă nu există evaluări

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Icms Basis Conclusions 200717 JF PDFDocument7 paginiIcms Basis Conclusions 200717 JF PDFSujithÎncă nu există evaluări

- HP Blueprint - PsDocument87 paginiHP Blueprint - PsRangabashyam100% (2)

- Case Interview QnsDocument16 paginiCase Interview Qnsagaba100% (1)

- Uma KapilaDocument10 paginiUma Kapilarohan50% (2)

- Presented By,: - Abhijeet Muttepwar - Roll No. 57 - Dr. D. Y. Patil School of EnineeringDocument17 paginiPresented By,: - Abhijeet Muttepwar - Roll No. 57 - Dr. D. Y. Patil School of EnineeringAbhijeetMuttepwarÎncă nu există evaluări

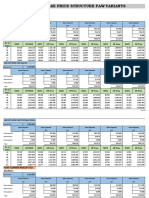

- Car PricesDocument47 paginiCar PricesMajoo SonsÎncă nu există evaluări

- Quick RatioDocument15 paginiQuick RatioAin roseÎncă nu există evaluări

- Natural Resource CharterDocument36 paginiNatural Resource CharterThe Globe and MailÎncă nu există evaluări

- NiftyDocument15 paginiNiftySayali KambleÎncă nu există evaluări

- Business Model CanvasDocument2 paginiBusiness Model CanvasMuhamad Arif RohmanÎncă nu există evaluări

- Ca Chapter 17-01Document9 paginiCa Chapter 17-01Yasmine JazzÎncă nu există evaluări

- Economic Principles 201819Document27 paginiEconomic Principles 201819Fortunatus JuliusÎncă nu există evaluări

- Milton M. Pressley Milton M. PressleyDocument31 paginiMilton M. Pressley Milton M. PressleyAvinEbaneshÎncă nu există evaluări

- Requirement 1 This Year Last Year: Case 3 (Comprehensive Ratio Analysis)Document6 paginiRequirement 1 This Year Last Year: Case 3 (Comprehensive Ratio Analysis)Mark Jayson Gonzaga CerezoÎncă nu există evaluări

- Topic 8 - Accounting For Manufacturing OperationsDocument41 paginiTopic 8 - Accounting For Manufacturing Operationsdenixng100% (8)

- Study Guide Variable Versus Absorption CostingDocument9 paginiStudy Guide Variable Versus Absorption CostingFlorie May HizoÎncă nu există evaluări

- New Criteria For Market SegmentationDocument9 paginiNew Criteria For Market Segmentationsumit jhaÎncă nu există evaluări

- TeDocument8 paginiTeRaja JulianÎncă nu există evaluări

- 2019mar S4 Exam Paper 1 EngDocument8 pagini2019mar S4 Exam Paper 1 EngcarliehtcheungÎncă nu există evaluări

- Brief Notes On The Arrow-Debreu-Mckenzie Model of An EconomyDocument6 paginiBrief Notes On The Arrow-Debreu-Mckenzie Model of An EconomySaadgi AgarwalÎncă nu există evaluări

- Questions Chapter 10Document25 paginiQuestions Chapter 10abdul majid khawajaÎncă nu există evaluări

- Auto Insurance Database Report 2013/2014: January 2017Document254 paginiAuto Insurance Database Report 2013/2014: January 2017ravikumarÎncă nu există evaluări

- How To Recognize Revenue From GWPDocument7 paginiHow To Recognize Revenue From GWPRush YuviencoÎncă nu există evaluări

- Finanncial Management 1 - Chapter 19Document5 paginiFinanncial Management 1 - Chapter 19lerryroyceÎncă nu există evaluări

- Case Study of The Gap, Inc.Document6 paginiCase Study of The Gap, Inc.nioriatti8924Încă nu există evaluări

- Cambridge International Advanced Subsidiary and Advanced LevelDocument20 paginiCambridge International Advanced Subsidiary and Advanced LevelTatenda NdlovuÎncă nu există evaluări

- Bangle Case StudyDocument2 paginiBangle Case StudyJay OswalÎncă nu există evaluări

- A Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Document25 paginiA Dollarization Blueprint For Argentina, Cato Foreign Policy Briefing No. 52Cato InstituteÎncă nu există evaluări

- Introduction To LCCDocument32 paginiIntroduction To LCCGonzalo LopezÎncă nu există evaluări

- CH 32 New Monetary and Fiscal PolicyDocument30 paginiCH 32 New Monetary and Fiscal PolicyEveÎncă nu există evaluări