S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Longest HatredDocument44 paginiThe Longest HatredRene SchergerÎncă nu există evaluări

- LPPM Uninus: Lembar PengesahanDocument42 paginiLPPM Uninus: Lembar PengesahanYustita DamayantiÎncă nu există evaluări

- Credit Co-Operative SocietiesDocument31 paginiCredit Co-Operative SocietiesGurpreet Singh Deol100% (1)

- Docutel CorporationDocument16 paginiDocutel CorporationArchana SinhaÎncă nu există evaluări

- Types of Housing LoanDocument20 paginiTypes of Housing LoanIzzuddin ZulkefliÎncă nu există evaluări

- The Philippine National Bank Was Established As A GovernmentDocument7 paginiThe Philippine National Bank Was Established As A GovernmentIris Valerie Bontia CabunilasÎncă nu există evaluări

- July 2009 NavigatorDocument4 paginiJuly 2009 NavigatorRob FernandesÎncă nu există evaluări

- Evangelista V ScreenexDocument3 paginiEvangelista V ScreenexJustine83% (6)

- B1+ UNIT 10 Life Skills WorksheetDocument1 paginăB1+ UNIT 10 Life Skills Worksheetanon_548788229100% (1)

- Loan Documentation PDFDocument16 paginiLoan Documentation PDFMuhammad Akmal HossainÎncă nu există evaluări

- 11th Commerce EM Important Questions English Medium PDF DownloadDocument4 pagini11th Commerce EM Important Questions English Medium PDF DownloadworstjaganÎncă nu există evaluări

- UntitledDocument10 paginiUntitledHien HaÎncă nu există evaluări

- Annual Reports 2015Document128 paginiAnnual Reports 2015Fuaad DodooÎncă nu există evaluări

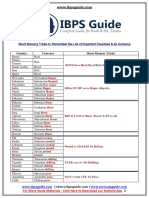

- Short TricksDocument2 paginiShort TricksAditi SaxenaÎncă nu există evaluări

- RRL ResearchDocument1 paginăRRL ResearchEzel May ArelladoÎncă nu există evaluări

- Feasibility ASKI Isabela PhilippinesDocument96 paginiFeasibility ASKI Isabela PhilippinesAyne Cabacungan50% (2)

- Panel de Control Obras Civiles - Luceli - Semana 09.1Document48 paginiPanel de Control Obras Civiles - Luceli - Semana 09.1Leydi BecerraÎncă nu există evaluări

- Bpi Vs Ca GR No. 136202Document7 paginiBpi Vs Ca GR No. 136202Drean TubislloÎncă nu există evaluări

- The Commercial Letter of Credit Final NA TALAGADocument27 paginiThe Commercial Letter of Credit Final NA TALAGAMaricar SalameñaÎncă nu există evaluări

- Fraz CVDocument2 paginiFraz CVfrazÎncă nu există evaluări

- OpTransactionHistoryTpr17 09 2019 PDFDocument2 paginiOpTransactionHistoryTpr17 09 2019 PDFSonu DangiÎncă nu există evaluări

- LL Line of CreditDocument20 paginiLL Line of Creditamir mahmudÎncă nu există evaluări

- Introduction To Financial SystemDocument37 paginiIntroduction To Financial SystemPauline BiancaÎncă nu există evaluări

- Reading Passage 1Document9 paginiReading Passage 1Kaushik RayÎncă nu există evaluări

- Invertis B Com Project 2016Document54 paginiInvertis B Com Project 2016shobhitÎncă nu există evaluări

- Sfatm Chapter 2Document16 paginiSfatm Chapter 2api-233324921Încă nu există evaluări

- Bank Asia LTD CRMDocument12 paginiBank Asia LTD CRMIslam MuhammadÎncă nu există evaluări

- The Brand Finance MENA 50 The Middle East's Most Valuable BrandsDocument1 paginăThe Brand Finance MENA 50 The Middle East's Most Valuable BrandsAhmed KorraÎncă nu există evaluări

- Bankers Trust Case Study - Finance TrainDocument2 paginiBankers Trust Case Study - Finance TrainPeterGomesÎncă nu există evaluări

- Income Tax ReviewerDocument99 paginiIncome Tax ReviewerKarlo Marco Cleto100% (1)