S-ar putea să vă placă și

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- Part 4 Media Research MethodsDocument79 paginiPart 4 Media Research MethodsDEEPAK GROVERÎncă nu există evaluări

- News ReportingDocument70 paginiNews ReportingDEEPAK GROVER100% (2)

- Part 2 Business Communication and Corporate Life SkillsDocument72 paginiPart 2 Business Communication and Corporate Life SkillsDEEPAK GROVERÎncă nu există evaluări

- Part 6 Social Change and Development CommunicationDocument76 paginiPart 6 Social Change and Development CommunicationDEEPAK GROVERÎncă nu există evaluări

- Part 1 AdvertisingDocument157 paginiPart 1 AdvertisingDEEPAK GROVERÎncă nu există evaluări

- The Policies of Global CommunicationDocument11 paginiThe Policies of Global CommunicationDEEPAK GROVERÎncă nu există evaluări

- Development of Informatics and Telematic ApplicationsDocument4 paginiDevelopment of Informatics and Telematic ApplicationsDEEPAK GROVERÎncă nu există evaluări

- Media Development in Third WorldDocument1 paginăMedia Development in Third WorldDEEPAK GROVERÎncă nu există evaluări

- Journalism and Current Affairs 1Document54 paginiJournalism and Current Affairs 1DEEPAK GROVERÎncă nu există evaluări

- Role of UNESCO in Bridging The Gap BetweenDocument8 paginiRole of UNESCO in Bridging The Gap BetweenDEEPAK GROVER100% (1)

- Role of UN in Bridging The Gap BetweenDocument12 paginiRole of UN in Bridging The Gap BetweenDEEPAK GROVER100% (1)

- Role of UNDocument13 paginiRole of UNDEEPAK GROVERÎncă nu există evaluări

- Regional Cooper at IonsDocument8 paginiRegional Cooper at IonsDEEPAK GROVERÎncă nu există evaluări

- Recommendations of MacBride CommissionDocument25 paginiRecommendations of MacBride CommissionDEEPAK GROVER83% (41)

- Recommendations of NWICODocument3 paginiRecommendations of NWICODEEPAK GROVER100% (2)

- MacBride CommissionDocument1 paginăMacBride CommissionDEEPAK GROVER83% (12)

- Policies of Global CommunicationDocument14 paginiPolicies of Global CommunicationDEEPAK GROVERÎncă nu există evaluări

- IPDC (International Programme For Development of Communication)Document5 paginiIPDC (International Programme For Development of Communication)DEEPAK GROVERÎncă nu există evaluări

- Critique of International News AgenciesDocument2 paginiCritique of International News AgenciesDEEPAK GROVER100% (1)

- ITUDocument5 paginiITUDEEPAK GROVERÎncă nu există evaluări

- Government Media OrganizationsDocument13 paginiGovernment Media OrganizationsDEEPAK GROVERÎncă nu există evaluări

- You Are in Crisis!Document14 paginiYou Are in Crisis!DEEPAK GROVERÎncă nu există evaluări

- Bilateral Multilateral and Regional Information Co OperationsDocument11 paginiBilateral Multilateral and Regional Information Co OperationsDEEPAK GROVERÎncă nu există evaluări

- Democratization of CommunicationDocument5 paginiDemocratization of CommunicationDEEPAK GROVERÎncă nu există evaluări

- Democratization ofDocument18 paginiDemocratization ofDEEPAK GROVERÎncă nu există evaluări

- PRSA Code of EthicsDocument7 paginiPRSA Code of EthicsDEEPAK GROVERÎncă nu există evaluări

- Advertising in The MediaDocument21 paginiAdvertising in The MediaDEEPAK GROVERÎncă nu există evaluări

- Hollywood - S Foray Into Film IndustryDocument12 paginiHollywood - S Foray Into Film IndustryDEEPAK GROVER100% (2)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- ExxxxxxDocument2 paginiExxxxxxGuiness DeguzmanÎncă nu există evaluări

- Kashato ShirtsDocument24 paginiKashato ShirtslalaÎncă nu există evaluări

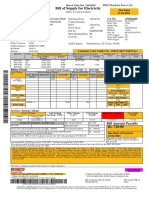

- Bill of Supply For Electricity: Due Date: 13-04-2021Document1 paginăBill of Supply For Electricity: Due Date: 13-04-2021Aditya RajÎncă nu există evaluări

- Hidalgo Enterprises Vs Baladan, 91 Phil 488Document8 paginiHidalgo Enterprises Vs Baladan, 91 Phil 488Arnold ClavioÎncă nu există evaluări

- Notification DMRCL Asst ManagersDocument8 paginiNotification DMRCL Asst ManagersRamanuja SuriÎncă nu există evaluări

- Batas Pambansa BLG 22Document19 paginiBatas Pambansa BLG 22JS DSÎncă nu există evaluări

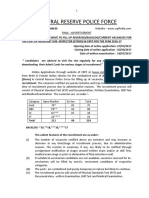

- Notification CRPF ASI Steno PostsDocument43 paginiNotification CRPF ASI Steno PostsRaju NaiduÎncă nu există evaluări

- Atp 106 LPM Accounting - Topic 3 - Bank ReconciliationDocument10 paginiAtp 106 LPM Accounting - Topic 3 - Bank ReconciliationTwain JonesÎncă nu există evaluări

- LC & Its ClassificationDocument42 paginiLC & Its ClassificationEngr Ahmed SabbirÎncă nu există evaluări

- How To File 1096 1099a 1099oid To Pay Utility BillsDocument7 paginiHow To File 1096 1099a 1099oid To Pay Utility BillsNotarys To Go98% (51)

- SST Guideline PDFDocument119 paginiSST Guideline PDFonghpÎncă nu există evaluări

- IDFCFIRSTBankstatement 10023948749Document8 paginiIDFCFIRSTBankstatement 10023948749Praveen SainiÎncă nu există evaluări

- PhilgepsDocument11 paginiPhilgepsreivinÎncă nu există evaluări

- Application & Challan FormDocument5 paginiApplication & Challan FormShiraz AhmedÎncă nu există evaluări

- Lab Task 3 Fully Dressed Use CasesDocument5 paginiLab Task 3 Fully Dressed Use CasesMuhammad ImranÎncă nu există evaluări

- Project ReportDocument41 paginiProject Reportsarthakzz50% (2)

- B&i C.P.Document3 paginiB&i C.P.Aditya D TanwarÎncă nu există evaluări

- Cham Vs Atty. Eva Paita-Moya 27 Jun 08 PDFDocument5 paginiCham Vs Atty. Eva Paita-Moya 27 Jun 08 PDFKaye RodriguezÎncă nu există evaluări

- Instruction Sheet - INR A2 Form - GIC-220610049Document1 paginăInstruction Sheet - INR A2 Form - GIC-220610049vivekÎncă nu există evaluări

- Remrev Digest Set 2Document54 paginiRemrev Digest Set 2Ayra Arcilla100% (1)

- Release of Preserved Benefit  " Financial Hardship Assets Less Than $50,000Document6 paginiRelease of Preserved Benefit  " Financial Hardship Assets Less Than $50,000Dallas MillerÎncă nu există evaluări

- Negotiable Instruments and Indian LawDocument147 paginiNegotiable Instruments and Indian LawNeed NotknowÎncă nu există evaluări

- Ebill 100007950200Document6 paginiEbill 100007950200nurul ainÎncă nu există evaluări

- Business Studies Past Papers With Answers (2015-2023)Document142 paginiBusiness Studies Past Papers With Answers (2015-2023)Chimwemwe TemboÎncă nu există evaluări

- Sales and Distribution (SD) : SAP University Alliances Authors Bret Wagner Stefan WeidnerDocument16 paginiSales and Distribution (SD) : SAP University Alliances Authors Bret Wagner Stefan WeidnerobÎncă nu există evaluări

- 2012 NLRC Sheriffs' Manual On ExecutionDocument13 pagini2012 NLRC Sheriffs' Manual On ExecutionBrian Baldwin100% (1)

- Hleb FaqDocument20 paginiHleb FaqChoon CheÎncă nu există evaluări

- 5.digested Diego v. DiegoDocument3 pagini5.digested Diego v. DiegoArrianne Obias100% (1)

- Cooperatives LatestDocument30 paginiCooperatives LatestsbikmmÎncă nu există evaluări

- Obligation Request and Status Budget Utilization Request and StatusDocument2 paginiObligation Request and Status Budget Utilization Request and StatusKatrina SedilloÎncă nu există evaluări