S-ar putea să vă placă și

- Ngas Module Government AccountingDocument11 paginiNgas Module Government AccountingAnn Kristine Trinidad50% (2)

- Ola BillDocument3 paginiOla BillMohit TanwarÎncă nu există evaluări

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeDe la Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeEvaluare: 1 din 5 stele1/5 (1)

- Fixed Assets Guidelines for PT Siemens IndonesiaDocument22 paginiFixed Assets Guidelines for PT Siemens IndonesiaHary KhreesnaÎncă nu există evaluări

- Tax1 (T31920)Document82 paginiTax1 (T31920)Charles TuazonÎncă nu există evaluări

- XXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationDocument7 paginiXXXXXXXXXXXXXXX, Inc.: Notes To Financial Statements DECEMBER 31, 2018 1.) Corporate InformationJmei AfflieriÎncă nu există evaluări

- Significant Accounting PoliciesDocument4 paginiSignificant Accounting PoliciesVenkat Sai Kumar KothalaÎncă nu există evaluări

- July 2022 PayslipDocument1 paginăJuly 2022 Payslipalumi ghodÎncă nu există evaluări

- Financial StatementsDocument35 paginiFinancial StatementsTapish GroverÎncă nu există evaluări

- Notes To Financial StatementsDocument3 paginiNotes To Financial StatementsJohn Glenn100% (1)

- Come Back Soon - . .: Doni Kurniawan, Doni KurniawanDocument1 paginăCome Back Soon - . .: Doni Kurniawan, Doni Kurniawandkurnia9999Încă nu există evaluări

- 13.republic Vs RicarteDocument1 pagină13.republic Vs RicarteGyelamagne EstradaÎncă nu există evaluări

- BSNLDocument3 paginiBSNLPriyanshi AgarwalaÎncă nu există evaluări

- BSNL Benifit MedicalDocument4 paginiBSNL Benifit MedicalharishsatheÎncă nu există evaluări

- Nykaa E Retail Mar 19Document23 paginiNykaa E Retail Mar 19NatÎncă nu există evaluări

- Accounting PolicyDocument28 paginiAccounting PolicyAkshay AnandÎncă nu există evaluări

- Accounting Policies and Notes Final 14.09.2016Document10 paginiAccounting Policies and Notes Final 14.09.2016ramaiahÎncă nu există evaluări

- Financial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023Document28 paginiFinancial Staements Duly Authenticated As Per Section 134 (Including Boards Report, Auditors Report and Other Documents) - 29102023mnbvcxzqwerÎncă nu există evaluări

- Mohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Document4 paginiMohammed Bilal Choudhary (Ju2021Mba14574) Activity - 1 Fsra 1Md BilalÎncă nu există evaluări

- Accounting Policies in Bharat ElectronicsDocument4 paginiAccounting Policies in Bharat ElectronicsNafis SiddiquiÎncă nu există evaluări

- CK Foods Significant Accounting PoliciesDocument9 paginiCK Foods Significant Accounting PoliciesA YoungÎncă nu există evaluări

- Accounting Policies 31.3.2020Document3 paginiAccounting Policies 31.3.2020Sheenu KapoorÎncă nu există evaluări

- Master NoteDocument9 paginiMaster NoteCA Paramesh HemanathÎncă nu există evaluări

- Schedule - Specimen of Statement of Significant Accounting PoliciesDocument16 paginiSchedule - Specimen of Statement of Significant Accounting Policiesav_meshramÎncă nu există evaluări

- NDDB AR 2016-17 Eng 0 Part47Document2 paginiNDDB AR 2016-17 Eng 0 Part47siva kumarÎncă nu există evaluări

- Statement of ComplianceDocument21 paginiStatement of ComplianceFaiz Smile BuddyÎncă nu există evaluări

- Notes To Balance Sheet and Statement of Profit and Loss: Hundred and Seventh Annual Report 2013-14Document44 paginiNotes To Balance Sheet and Statement of Profit and Loss: Hundred and Seventh Annual Report 2013-14galacticwormÎncă nu există evaluări

- Accounting LearningsDocument4 paginiAccounting LearningsLovely Jane Raut CabiltoÎncă nu există evaluări

- EFU Accounting PoliciesDocument9 paginiEFU Accounting PoliciesJaved AkramÎncă nu există evaluări

- SAIL's General Information and Accounting PrinciplesDocument2 paginiSAIL's General Information and Accounting PrinciplesGhritachi PaulÎncă nu există evaluări

- Consolidated Financial Statements Indian GAAP Dec07Document15 paginiConsolidated Financial Statements Indian GAAP Dec07martynmvÎncă nu există evaluări

- Accounting Policies - Study Group 4IDocument24 paginiAccounting Policies - Study Group 4ISatish Ranjan PradhanÎncă nu există evaluări

- Disclosure of Accounting PoliciesDocument17 paginiDisclosure of Accounting PoliciesarthurenjuÎncă nu există evaluări

- Megaworld Corporation: Liabilities and Equity 2010 2009 2008Document9 paginiMegaworld Corporation: Liabilities and Equity 2010 2009 2008Owdray CiaÎncă nu există evaluări

- Financial Statement Accounting PoliciesDocument9 paginiFinancial Statement Accounting PoliciesMy NameÎncă nu există evaluări

- Notes Forming Part of Financial StatementsDocument36 paginiNotes Forming Part of Financial StatementsSwarup RanjanÎncă nu există evaluări

- Allowable DeductionsDocument7 paginiAllowable DeductionsCOLLET GAOLEBEÎncă nu există evaluări

- Account CodeDocument35 paginiAccount CodeIsha SethiÎncă nu există evaluări

- Accounting PoliciesDocument9 paginiAccounting PoliciesKivumbi WilliamÎncă nu există evaluări

- Note FinantionalDocument4 paginiNote FinantionalhvhvmÎncă nu există evaluări

- Notes To The Financial Statements SampleDocument6 paginiNotes To The Financial Statements SampleKielRinonÎncă nu există evaluări

- Significant Accounting PoliciesDocument4 paginiSignificant Accounting PoliciesAdarsh NethwewalaÎncă nu există evaluări

- New Government Accounting System FeaturesDocument4 paginiNew Government Accounting System FeaturesabbiecdefgÎncă nu există evaluări

- Financial statements notes summaryDocument39 paginiFinancial statements notes summaryBharat AroraÎncă nu există evaluări

- Indian Accounting Standards: Manish B TardejaDocument45 paginiIndian Accounting Standards: Manish B TardejaManish TardejaÎncă nu există evaluări

- Significant Accounting Policies TVS MotorsDocument12 paginiSignificant Accounting Policies TVS MotorsArjun Singh Omkar100% (1)

- Major Accounting PoliciesDocument8 paginiMajor Accounting Policies325KAIVALYAPAIÎncă nu există evaluări

- 09-OVP2020 Part1-Notes To FSDocument24 pagini09-OVP2020 Part1-Notes To FSRuffus ToqueroÎncă nu există evaluări

- Section 4 IDocument22 paginiSection 4 ISatish Ranjan PradhanÎncă nu există evaluări

- Ar-18 9Document5 paginiAr-18 9jawad anwarÎncă nu există evaluări

- QuadrantDocument2 paginiQuadrantVibhor SinghÎncă nu există evaluări

- Amendment PArveen Sharma NotesDocument59 paginiAmendment PArveen Sharma NotesSuhag Patel0% (1)

- Aef 2013 Audit Acc ReqDocument9 paginiAef 2013 Audit Acc Reqvikas_ojha54706Încă nu există evaluări

- Standalone Notes To AccountsDocument31 paginiStandalone Notes To AccountsJP Jeya PrasannaÎncă nu există evaluări

- Picwise Mart - Notes To Financial Statements - 31dec2021Document1 paginăPicwise Mart - Notes To Financial Statements - 31dec2021Thomas Daniel CuarteroÎncă nu există evaluări

- Financial Management: Howard & UptonDocument4 paginiFinancial Management: Howard & Uptonak21679Încă nu există evaluări

- Schedule C Business Income TaxDocument12 paginiSchedule C Business Income TaxJichang HikÎncă nu există evaluări

- IND As SummaryDocument41 paginiIND As SummaryAishwarya RajeshÎncă nu există evaluări

- Date: 2009.03.31. Accounting Policies: Chambal Fertilisers & Chemicals LTDDocument14 paginiDate: 2009.03.31. Accounting Policies: Chambal Fertilisers & Chemicals LTDJayverdhan TiwariÎncă nu există evaluări

- 2.7 Intangible Assets (A) GoodwillDocument8 pagini2.7 Intangible Assets (A) GoodwillLolita IsakhanyanÎncă nu există evaluări

- Significant Accounting Policies of InfosysDocument5 paginiSignificant Accounting Policies of Infosyscadbury23Încă nu există evaluări

- Accounting For Government and Not-For-Profit OrganizationsDocument8 paginiAccounting For Government and Not-For-Profit OrganizationsAngela QuililanÎncă nu există evaluări

- Probiotec Annual Report 2022 6Document8 paginiProbiotec Annual Report 2022 6楊敬宇Încă nu există evaluări

- BCOM HONS 5 Income Tax Law PracticeHDocument36 paginiBCOM HONS 5 Income Tax Law PracticeHPurushottam RathoreÎncă nu există evaluări

- 2021 TIMTA-ANNEX B Form (With Sample)Document27 pagini2021 TIMTA-ANNEX B Form (With Sample)Mark Kevin IIIÎncă nu există evaluări

- Guest Checkout GuideDocument7 paginiGuest Checkout GuideechxÎncă nu există evaluări

- Auto-Estradas / Motorways: Portagens / Toll SDocument9 paginiAuto-Estradas / Motorways: Portagens / Toll Scry19912617Încă nu există evaluări

- VAT problems with sales and purchase calculationsDocument3 paginiVAT problems with sales and purchase calculationsReginald ValenciaÎncă nu există evaluări

- Invoice No. 398484: Endor AGDocument1 paginăInvoice No. 398484: Endor AGLamesHunterÎncă nu există evaluări

- Assessment Types and Procedures in Indian Income TaxDocument12 paginiAssessment Types and Procedures in Indian Income TaxTanvi JawdekarÎncă nu există evaluări

- Universidad ECCI Sales ProFormaDocument1 paginăUniversidad ECCI Sales ProFormaManuel LopezÎncă nu există evaluări

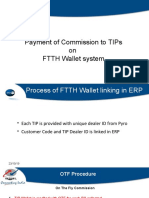

- FTTH Commission Payment ProcessDocument12 paginiFTTH Commission Payment ProcessVikrant PathakÎncă nu există evaluări

- Cash Receipts Journal (CRJ)Document1 paginăCash Receipts Journal (CRJ)KristineMarzanÎncă nu există evaluări

- Penawaran ECU VolvoDocument1 paginăPenawaran ECU VolvoAndy TeknikaÎncă nu există evaluări

- Instructions For Form 941: (Rev. April 2020)Document19 paginiInstructions For Form 941: (Rev. April 2020)suscripcionesbrmÎncă nu există evaluări

- Flexible Benefit Plan For LTTS FTCDocument1 paginăFlexible Benefit Plan For LTTS FTCDavidÎncă nu există evaluări

- Pune Municipal Corporation: Property Id: Financial Year: 2020-2021 Bill No: 112407 Nonresi Meter NoDocument1 paginăPune Municipal Corporation: Property Id: Financial Year: 2020-2021 Bill No: 112407 Nonresi Meter NoRajesh NayakÎncă nu există evaluări

- PGBP New SlidesDocument40 paginiPGBP New SlidesSachin Jain100% (2)

- RFUMSDocument2 paginiRFUMSSivakumar ThangarajanÎncă nu există evaluări

- Mi BillDocument1 paginăMi BillJagannath MandalÎncă nu există evaluări

- N28 TU2 Yljhuo PV 7 GDocument15 paginiN28 TU2 Yljhuo PV 7 GVishal BawaneÎncă nu există evaluări

- (Understanding TCC) TaxAdministrationDocument2 pagini(Understanding TCC) TaxAdministrationhandoutÎncă nu există evaluări

- TAX PART 1 Compiled PDFDocument114 paginiTAX PART 1 Compiled PDFArCee SantiagoÎncă nu există evaluări

- Gyaan All in OneDocument41 paginiGyaan All in OneHEMANT SARVANKARÎncă nu există evaluări

- P4-3 WPDocument4 paginiP4-3 WPAna LailaÎncă nu există evaluări

- Greenwood Nest Rate Chart 01.06.18Document4 paginiGreenwood Nest Rate Chart 01.06.18jubin4snapÎncă nu există evaluări

- Ebook Ebook PDF Pearsons Federal Taxation 2018 Individuals 31st Edition PDFDocument41 paginiEbook Ebook PDF Pearsons Federal Taxation 2018 Individuals 31st Edition PDFmichael.johnson225100% (33)

- Gmail - Booking Confirmation On IRCTC, Train - 12424, 10-Jul-2022, 2A, NDLS - GHY (1) - 2Document1 paginăGmail - Booking Confirmation On IRCTC, Train - 12424, 10-Jul-2022, 2A, NDLS - GHY (1) - 2Girwar SinghÎncă nu există evaluări