S-ar putea să vă placă și

- T2 Mock Exam (Dec'08 Exam)Document12 paginiT2 Mock Exam (Dec'08 Exam)vasanthipuruÎncă nu există evaluări

- T4 - Past Paper CombinedDocument53 paginiT4 - Past Paper CombinedU Abdul Rehman100% (1)

- T4 June 08 QuesDocument10 paginiT4 June 08 QuessmhgilaniÎncă nu există evaluări

- Fma Past Papers 1Document23 paginiFma Past Papers 1Fatuma Coco BuddaflyÎncă nu există evaluări

- 4 2008 Dec ADocument5 pagini4 2008 Dec ALai Hui Ing100% (1)

- 02 MA2 LRP QuestionsDocument36 pagini02 MA2 LRP QuestionsKopanang Leokana50% (2)

- Control Accounts Q8 PDFDocument3 paginiControl Accounts Q8 PDFRyanÎncă nu există evaluări

- 02 MA1 LRP Questions 2014Document34 pagini02 MA1 LRP Questions 2014Yahya KaimkhaniÎncă nu există evaluări

- F2 Past Paper - Question12-2005Document13 paginiF2 Past Paper - Question12-2005ArsalanACCA100% (1)

- 2007 - Jun - QUS CAT T3Document10 pagini2007 - Jun - QUS CAT T3asad19Încă nu există evaluări

- 2006 - Dec - QUS CAT T3Document9 pagini2006 - Dec - QUS CAT T3asad190% (1)

- 3int - 2008 - Jun - Ans CAT T3Document6 pagini3int - 2008 - Jun - Ans CAT T3asad19Încă nu există evaluări

- Test t4 Labor CostingDocument2 paginiTest t4 Labor CostingSyed Muzaffar Ali ShahÎncă nu există evaluări

- Cat/fia (FFM)Document9 paginiCat/fia (FFM)theizzatirosli100% (1)

- F2 Mock Questions 201603Document12 paginiF2 Mock Questions 201603Renato WilsonÎncă nu există evaluări

- 3uk - 2007 - Dec - Q CAT T3Document10 pagini3uk - 2007 - Dec - Q CAT T3asad19Încă nu există evaluări

- Financial Information For Management: Time Allowed 3 HoursDocument14 paginiFinancial Information For Management: Time Allowed 3 HoursAnousha DookheeÎncă nu există evaluări

- Ma1 Formula Sheet Lecture Notes All ChaptersDocument7 paginiMa1 Formula Sheet Lecture Notes All ChaptersJ&A Partners JANÎncă nu există evaluări

- FA2 S20-A21 Examiner's ReportDocument6 paginiFA2 S20-A21 Examiner's ReportAreeb AhmadÎncă nu există evaluări

- ACCACAT Paper T4 Accounting For Costs INT Topicwise Past PapersDocument40 paginiACCACAT Paper T4 Accounting For Costs INT Topicwise Past PapersGT Boss AvyLara50% (4)

- MA1 (Mock 2)Document19 paginiMA1 (Mock 2)Shamas 786Încă nu există evaluări

- F2 Past Paper - Question06-2007Document13 paginiF2 Past Paper - Question06-2007ArsalanACCA100% (1)

- ACCA F2 Revision Notes OpenTuition PDFDocument25 paginiACCA F2 Revision Notes OpenTuition PDFSaurabh KaushikÎncă nu există evaluări

- F2 and FMA Full Specimen Exam Answers PDFDocument4 paginiF2 and FMA Full Specimen Exam Answers PDFSNEHA MARIYAM VARGHESE SIM 16-18Încă nu există evaluări

- PartB-4d-Throughput Accounting-StudentDocument5 paginiPartB-4d-Throughput Accounting-StudentDebbie BlackburnÎncă nu există evaluări

- CAT T10 - 2010 - Dec - ADocument9 paginiCAT T10 - 2010 - Dec - AHussain MeskinzadaÎncă nu există evaluări

- ACCA F2 AC N MCDocument10 paginiACCA F2 AC N MCSamuel DwumfourÎncă nu există evaluări

- MA2 SummaryDocument20 paginiMA2 SummarypringuserÎncă nu există evaluări

- Absorption and Margin CostingDocument8 paginiAbsorption and Margin CostingIshfaq AhmadÎncă nu există evaluări

- Skans School of Accoutancy Subject Ma1 Test Teacher Shahab Name Batch Obtained Marks Total Marks 30Document4 paginiSkans School of Accoutancy Subject Ma1 Test Teacher Shahab Name Batch Obtained Marks Total Marks 30shahabÎncă nu există evaluări

- 13-ACCA-FA2-Chp 13Document22 pagini13-ACCA-FA2-Chp 13SMS PrintingÎncă nu există evaluări

- Test of Labour Overheads and Absorption and Marginal CostingDocument4 paginiTest of Labour Overheads and Absorption and Marginal CostingzairaÎncă nu există evaluări

- Ma2 Exam ReportDocument3 paginiMa2 Exam ReportAhmad Hafid Hanifah100% (1)

- F2 Past Paper - Question06-2002Document8 paginiF2 Past Paper - Question06-2002ArsalanACCAÎncă nu există evaluări

- F2 Past Paper - Question12-2004Document13 paginiF2 Past Paper - Question12-2004ArsalanACCAÎncă nu există evaluări

- MA1 (Mock 1)Document16 paginiMA1 (Mock 1)Shamas 786Încă nu există evaluări

- Fa1 4&BRSDocument5 paginiFa1 4&BRSShahab ShafiÎncă nu există evaluări

- MA1 BPP Kit (2016) CompletedDocument113 paginiMA1 BPP Kit (2016) CompletedAbdul Wasay AlsyedÎncă nu există evaluări

- Fa2 Mock 3 AnswersDocument13 paginiFa2 Mock 3 Answerssameerjameel678Încă nu există evaluări

- Mock 2Document13 paginiMock 2Angie Nguyen0% (1)

- Ma1 Examreport d12Document4 paginiMa1 Examreport d12Josh BissoonÎncă nu există evaluări

- F2 Past Paper - Question06-2005Document14 paginiF2 Past Paper - Question06-2005ArsalanACCAÎncă nu există evaluări

- 3int - 2005 - Dec - Ans CAT T3Document8 pagini3int - 2005 - Dec - Ans CAT T3asad19Încă nu există evaluări

- FA1 Mock 1Document10 paginiFA1 Mock 1Abdul MughalÎncă nu există evaluări

- Exam Revision QuestionsDocument5 paginiExam Revision Questionsfreddy kwakwalaÎncă nu există evaluări

- F2MA Test 3 From ACCA Sep 2020 QuestionDocument15 paginiF2MA Test 3 From ACCA Sep 2020 QuestionthetÎncă nu există evaluări

- 3int - 2004 - Jun - Ans CAT T3Document7 pagini3int - 2004 - Jun - Ans CAT T3asad19Încă nu există evaluări

- đề cô OanhDocument17 paginiđề cô OanhXuân Ngân Phùng HoàngÎncă nu există evaluări

- F 2Document6 paginiF 2Nasir Iqbal100% (1)

- Acct 2 0Document9 paginiAcct 2 0Kamran HaiderÎncă nu există evaluări

- JB Limited Is A Small Specialist Manufacturer of Electronic ComponentsDocument2 paginiJB Limited Is A Small Specialist Manufacturer of Electronic ComponentsAmit PandeyÎncă nu există evaluări

- Ma1 PilotDocument17 paginiMa1 PilotKu Farah Syarina0% (1)

- Fma Past Paper 3 (F2)Document24 paginiFma Past Paper 3 (F2)Shereka EllisÎncă nu există evaluări

- Saa Group Cat TT7 Mock 2011 PDFDocument16 paginiSaa Group Cat TT7 Mock 2011 PDFAngie NguyenÎncă nu există evaluări

- Ma 2 AccaDocument18 paginiMa 2 AccaRielleo Leo67% (3)

- Ma2 Specimen j14Document16 paginiMa2 Specimen j14talha100% (3)

- 1 2 2006 Dec QDocument12 pagini1 2 2006 Dec QGeorges NdumbeÎncă nu există evaluări

- Ma1 Specimen j14Document17 paginiMa1 Specimen j14Shohin100% (1)

- 3 1-2 - 2006 - Jun - Q.Document13 pagini3 1-2 - 2006 - Jun - Q.Patricia DouceÎncă nu există evaluări

- Adl 56 - Cost Managerial Accounting AssignmentDocument11 paginiAdl 56 - Cost Managerial Accounting AssignmentVincent Keys100% (1)

- CHAPTER 3 MCPROBLEMS, MCTHEORIES, SHORT PROBLEMS, COMPREHENSIVE PROBLEMS - Understanding-Financial-StatementsDocument99 paginiCHAPTER 3 MCPROBLEMS, MCTHEORIES, SHORT PROBLEMS, COMPREHENSIVE PROBLEMS - Understanding-Financial-StatementsRhedeline LugodÎncă nu există evaluări

- It Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesDocument24 paginiIt Is A Stock Valuation Method - That Uses Financial and Economic Analysis - To Predict The Movement of Stock PricesAnonymous KN4pnOHmÎncă nu există evaluări

- Acroynms Capital MarketsDocument37 paginiAcroynms Capital MarketsAnuj Sharma100% (1)

- Betting DoctorDocument8 paginiBetting DoctorTim80% (5)

- Republic Act No. 9160, As Amended (Anti-Money Laundering Act of 2001 (AMLA) ) : Strong Anti-Money Laundering Regime A Deterrent To Corruption in The Public Sector.Document20 paginiRepublic Act No. 9160, As Amended (Anti-Money Laundering Act of 2001 (AMLA) ) : Strong Anti-Money Laundering Regime A Deterrent To Corruption in The Public Sector.targa215Încă nu există evaluări

- Export GuidanceDocument45 paginiExport GuidanceRomi PatelÎncă nu există evaluări

- Africa Horizons: A Unique Guide To Real Estate Investment OpportunitiesDocument18 paginiAfrica Horizons: A Unique Guide To Real Estate Investment OpportunitiesJonathan MahengeÎncă nu există evaluări

- B B ADocument3 paginiB B AVaishnavi SubramanianÎncă nu există evaluări

- CRUDE OIL Hedge-StrategyDocument4 paginiCRUDE OIL Hedge-StrategyNeelesh KamathÎncă nu există evaluări

- 2017 12 07 - APU Draft02 SignedDocument49 pagini2017 12 07 - APU Draft02 SignedAnonymous pWVSQ1oIG6Încă nu există evaluări

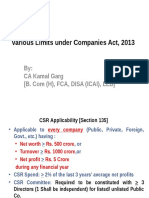

- Various Limits Under Companies Act, 2013 (CA Final)Document61 paginiVarious Limits Under Companies Act, 2013 (CA Final)Asim JavedÎncă nu există evaluări

- K Hoff PAR 115 Portfolio #15 Trust AgreementDocument21 paginiK Hoff PAR 115 Portfolio #15 Trust AgreementlegalparaeagleÎncă nu există evaluări

- Wallstreetjournal 20171124 TheWallStreetJournalDocument42 paginiWallstreetjournal 20171124 TheWallStreetJournalTevinWaiguruÎncă nu există evaluări

- A Problem and Decision Analysis of The HBR Clayton IndustriesDocument3 paginiA Problem and Decision Analysis of The HBR Clayton IndustriesnurudddinÎncă nu există evaluări

- Managerial Finance: Article InformationDocument22 paginiManagerial Finance: Article Informationlia s.Încă nu există evaluări

- Ashirbad Production HomeDocument4 paginiAshirbad Production Homeanon_913070355Încă nu există evaluări

- Project Finance (Smart Task 3)Document13 paginiProject Finance (Smart Task 3)Aseem Vashist100% (1)

- Sinco Vs Longa & Tevez 1928 (Guardianship) Facts:: Specpro Digest - MidtermDocument2 paginiSinco Vs Longa & Tevez 1928 (Guardianship) Facts:: Specpro Digest - MidtermAngelic ArcherÎncă nu există evaluări

- NullDocument206 paginiNullapi-24983466Încă nu există evaluări

- 17-BSA 700 and 705Document16 pagini17-BSA 700 and 705Sohel Rana100% (1)

- Net Present Value AnalysisDocument6 paginiNet Present Value AnalysisAmna Khalid100% (1)

- 202E08Document22 pagini202E08David David100% (1)

- Project On Resort Cum HotelDocument13 paginiProject On Resort Cum Hotelsunilsony12376% (21)

- Urban Planning and Real Estate DevelopmentDocument5 paginiUrban Planning and Real Estate Developmentanon_145354896Încă nu există evaluări

- Finman 1-4 SummaryDocument8 paginiFinman 1-4 SummaryElieÎncă nu există evaluări

- Asian Tigers Financial Crisis 1997Document25 paginiAsian Tigers Financial Crisis 1997Vanshika AroraÎncă nu există evaluări

- Theresa Wulff ResumeDocument3 paginiTheresa Wulff ResumemomnpopÎncă nu există evaluări

- Scott 7FigureGuide V2 PDFDocument23 paginiScott 7FigureGuide V2 PDFObiÎncă nu există evaluări

- Advacc 2 Chapter 1 ProblemsDocument5 paginiAdvacc 2 Chapter 1 ProblemsClint-Daniel Abenoja100% (1)