S-ar putea să vă placă și

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1091)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Flowchart Real Property TaxDocument1 paginăFlowchart Real Property TaxPrincess Mae SamborioÎncă nu există evaluări

- Financial Markets and InstitutionsDocument28 paginiFinancial Markets and Institutionsmomindkhan100% (4)

- ch9 Solutions PDFDocument38 paginich9 Solutions PDFHussnain NaneÎncă nu există evaluări

- Business Finance Lesson-Exemplar - Module 3Document7 paginiBusiness Finance Lesson-Exemplar - Module 3Divina Grace Rodriguez - LibreaÎncă nu există evaluări

- Understanding Reg CC WPDocument18 paginiUnderstanding Reg CC WPJeff WayneÎncă nu există evaluări

- NBFC in IndiaDocument19 paginiNBFC in IndiaBharath ReddyÎncă nu există evaluări

- Cash Flow Valuation MethodsDocument5 paginiCash Flow Valuation Methodssan_lookÎncă nu există evaluări

- De Minh Hoa Va Dap An Giua Hkii Khoi 10 - 63202416Document6 paginiDe Minh Hoa Va Dap An Giua Hkii Khoi 10 - 632024164701701078.studentÎncă nu există evaluări

- Notes On Letter of CreditDocument17 paginiNotes On Letter of CreditDileep MainaliÎncă nu există evaluări

- Camp Price-List 2014 inDocument1 paginăCamp Price-List 2014 inGjuro14Încă nu există evaluări

- Addendum Sheet - CA Final May'23Document54 paginiAddendum Sheet - CA Final May'23Utkarsh GuptaÎncă nu există evaluări

- Group 2 Financing The Mozal ProjectDocument10 paginiGroup 2 Financing The Mozal ProjectYohan100% (1)

- EconomicsDocument13 paginiEconomicsmarkanthonycorpinÎncă nu există evaluări

- Internship ReportDocument24 paginiInternship ReportSyed Rizwan Ullah ShahÎncă nu există evaluări

- 0integrated Accounting: Financial Accounting & Reporting (P1)Document32 pagini0integrated Accounting: Financial Accounting & Reporting (P1)Jochelle Anne PaetÎncă nu există evaluări

- I LRD 3 L HF 78 W9 NBDWDocument3 paginiI LRD 3 L HF 78 W9 NBDWBIKRAM KUMAR BEHERAÎncă nu există evaluări

- A Study On Financial Performance Analysis of ACCDocument5 paginiA Study On Financial Performance Analysis of ACCpramodÎncă nu există evaluări

- Bank ReconciliationDocument23 paginiBank ReconciliationJohn Anjelo MoraldeÎncă nu există evaluări

- Maturity Claim (Form No.3825) PDFDocument3 paginiMaturity Claim (Form No.3825) PDFRajeev Ranjan100% (1)

- StatmentDocument9 paginiStatmentManju ManjunathÎncă nu există evaluări

- Financial Statements Analysis: Author: Tănase Alin-Eliodor, EVERET România DistributionDocument12 paginiFinancial Statements Analysis: Author: Tănase Alin-Eliodor, EVERET România Distributionعبد المؤمنÎncă nu există evaluări

- TATA Steel Financial ModelDocument19 paginiTATA Steel Financial ModelAkshayÎncă nu există evaluări

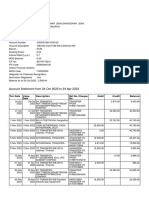

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument6 paginiStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceAluri SrinivasÎncă nu există evaluări

- Introduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtDocument38 paginiIntroduction To Accounting: Pg. 1 Compiled By: Abdul Ahad ButtMuhammad FaisalÎncă nu există evaluări

- CAIIB Paper 1 Module A Economic Analysis PDFDocument33 paginiCAIIB Paper 1 Module A Economic Analysis PDFPikku SharmaÎncă nu există evaluări

- FBI Chapter - 6 Part 2Document9 paginiFBI Chapter - 6 Part 2Golam RamijÎncă nu există evaluări

- Re - LLC Confirmation of DEVID V RDocument1 paginăRe - LLC Confirmation of DEVID V RShobha SinghÎncă nu există evaluări

- Activity Partnership DissolutionDocument2 paginiActivity Partnership DissolutionKaren Joy Jacinto ElloÎncă nu există evaluări

- Producers Bank of The PhilDocument15 paginiProducers Bank of The PhilTrisha RamentoÎncă nu există evaluări

- Sakshita Food LLP Balance Sheet As On 31/03/222 Particulars Current Year Previous Year I. Contribution and Liabilities A Partners' FundsDocument4 paginiSakshita Food LLP Balance Sheet As On 31/03/222 Particulars Current Year Previous Year I. Contribution and Liabilities A Partners' FundsAshish JainÎncă nu există evaluări