S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Eun8e CH 011 TomDocument33 paginiEun8e CH 011 TomCarter JayanÎncă nu există evaluări

- Greenwich Capital CMBS 2006 & Outlook For 2007Document43 paginiGreenwich Capital CMBS 2006 & Outlook For 2007bvaheyÎncă nu există evaluări

- Bear Stearns Annual Report 2006Document117 paginiBear Stearns Annual Report 2006highfinance100% (1)

- 2008 CrisisDocument60 pagini2008 CrisisShreyansh SanchetiÎncă nu există evaluări

- Test Bank Financial InstrumentDocument13 paginiTest Bank Financial InstrumentMasi100% (1)

- CB1 CMP Upgrade 2022Document80 paginiCB1 CMP Upgrade 2022Linh TinhÎncă nu există evaluări

- IRS-Service Look Up MBS by Cusip October 2007Document163 paginiIRS-Service Look Up MBS by Cusip October 2007tsherwood100% (1)

- PS2 Behavioral IeDocument5 paginiPS2 Behavioral IePablo BozaÎncă nu există evaluări

- EbmDocument4 paginiEbmAnushree Harshaj GoelÎncă nu există evaluări

- Unfulfilled Education Aspiration: Article SummaryDocument5 paginiUnfulfilled Education Aspiration: Article SummaryAnushree Harshaj GoelÎncă nu există evaluări

- Book Review - It Happened in India by Kishore Biyani: Fore School of ManagementDocument3 paginiBook Review - It Happened in India by Kishore Biyani: Fore School of ManagementAnushree Harshaj GoelÎncă nu există evaluări

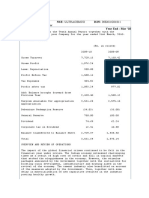

- Ultratech Cement Bse: 532538 Nse: Ultracemco Isin: Ine481G01011 Industry: Cement - Major Directors Report Year End: Mar '10Document7 paginiUltratech Cement Bse: 532538 Nse: Ultracemco Isin: Ine481G01011 Industry: Cement - Major Directors Report Year End: Mar '10Anushree Harshaj GoelÎncă nu există evaluări

- Diversification: Presented By: Anushree GuptaDocument9 paginiDiversification: Presented By: Anushree GuptaAnushree Harshaj GoelÎncă nu există evaluări

- Analysis of CMBS Bubble PDFDocument36 paginiAnalysis of CMBS Bubble PDFCooperÎncă nu există evaluări

- How To Save The Bond Insurers Presentation by Bill Ackman of Pershing Square Capital Management November 2007Document145 paginiHow To Save The Bond Insurers Presentation by Bill Ackman of Pershing Square Capital Management November 2007tomhigbieÎncă nu există evaluări

- CMBS Strategy WeeklyDocument14 paginiCMBS Strategy Weeklykkohle03Încă nu există evaluări

- The Evolution of Commercial Real Estate (Cre) Cdos: Nomura Fixed Income ResearchDocument20 paginiThe Evolution of Commercial Real Estate (Cre) Cdos: Nomura Fixed Income ResearchJay KabÎncă nu există evaluări

- Dissertation - Credit Risk Management Priority, Case Study of Russian BankingDocument32 paginiDissertation - Credit Risk Management Priority, Case Study of Russian Bankingthemany2292Încă nu există evaluări

- 2011 Exam 9 Financial Risk and Rate of Return: Options, Futures and Other Derivatives (SeventhDocument13 pagini2011 Exam 9 Financial Risk and Rate of Return: Options, Futures and Other Derivatives (Seventh97036795Încă nu există evaluări

- Spreads Versus Spread VolDocument14 paginiSpreads Versus Spread VolMatt WallÎncă nu există evaluări

- Credit Risk Analyst Interview Questions and Answers 1904Document13 paginiCredit Risk Analyst Interview Questions and Answers 1904MD ABDULLAH AL BAQUIÎncă nu există evaluări

- The Great Financial Scandal of 2003Document21 paginiThe Great Financial Scandal of 2003isaac setabiÎncă nu există evaluări

- Pricing of A CDODocument2 paginiPricing of A CDOJasvinder Josen100% (1)

- Fe5101 4Document60 paginiFe5101 4Yaomin SongÎncă nu există evaluări

- LB - Abs Cdo PrimerDocument28 paginiLB - Abs Cdo PrimerJonRLaiÎncă nu există evaluări

- Distressed Debt Investor StrategiesDocument20 paginiDistressed Debt Investor StrategiesProgyadityo Chatterjee100% (1)

- Debt Capital Market Conventions - May2013Document14 paginiDebt Capital Market Conventions - May2013kind.beach1199Încă nu există evaluări

- JP Morgan CDO HandbookDocument60 paginiJP Morgan CDO HandbookForeclosure Fraud100% (2)

- Credit DerivativesDocument21 paginiCredit Derivativesprachiz1Încă nu există evaluări

- Wachovia Securities DatabookDocument44 paginiWachovia Securities DatabookanshulsahibÎncă nu există evaluări

- Credit Risk - Credit DerivativesDocument20 paginiCredit Risk - Credit DerivativeskerenkangÎncă nu există evaluări

- ReillyBrown IAPM 11e PPT Ch12Document68 paginiReillyBrown IAPM 11e PPT Ch12rocky wongÎncă nu există evaluări

- Museum of American Finance - Credit Crises TimelineDocument1 paginăMuseum of American Finance - Credit Crises Timelinehythloday81Încă nu există evaluări

- Fi 17Document6 paginiFi 17priyanshu.goel1710Încă nu există evaluări

- A Study of Debt Securitization in Indian Financial Services SectorDocument40 paginiA Study of Debt Securitization in Indian Financial Services SectorShruti PandyaÎncă nu există evaluări