S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (894)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Singular Spectrum Analysis Demo With VBADocument12 paginiSingular Spectrum Analysis Demo With VBAPeter UrbaniÎncă nu există evaluări

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Document178 paginiIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- Opalesque New Managers May 2012Document51 paginiOpalesque New Managers May 2012Peter Urbani0% (1)

- Opalesque New Managers May 2012Document51 paginiOpalesque New Managers May 2012Peter Urbani0% (1)

- Random Forest in Excel and VBADocument24 paginiRandom Forest in Excel and VBAPeter UrbaniÎncă nu există evaluări

- Do You Have To Be Abnormal To Beat The MarketDocument3 paginiDo You Have To Be Abnormal To Beat The MarketPeter UrbaniÎncă nu există evaluări

- Partial Correlation Network Graph VBA (DJINDI)Document463 paginiPartial Correlation Network Graph VBA (DJINDI)Peter UrbaniÎncă nu există evaluări

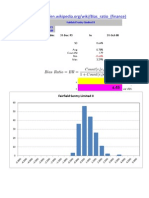

- Benford Bias Ratio VBA 2014Document136 paginiBenford Bias Ratio VBA 2014Peter UrbaniÎncă nu există evaluări

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBADocument7 paginiIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- Cholesky Versus SVDDocument4 paginiCholesky Versus SVDPeter UrbaniÎncă nu există evaluări

- Distressed Debt HF's Update (Mar 2013)Document40 paginiDistressed Debt HF's Update (Mar 2013)Peter UrbaniÎncă nu există evaluări

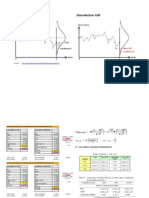

- Impact of Auto-Correlation On Expected Maximum DrawdownDocument67 paginiImpact of Auto-Correlation On Expected Maximum DrawdownPeter UrbaniÎncă nu există evaluări

- Opalesque NewManagers Sep 2012Document38 paginiOpalesque NewManagers Sep 2012Peter UrbaniÎncă nu există evaluări

- POD For GS VIP Hedge Fund Indices (Q3 2012)Document72 paginiPOD For GS VIP Hedge Fund Indices (Q3 2012)Peter UrbaniÎncă nu există evaluări

- Chimp Chump or ChampDocument7 paginiChimp Chump or ChampPeter UrbaniÎncă nu există evaluări

- Portfolio POD VBADocument14 paginiPortfolio POD VBAPeter Urbani100% (1)

- Opalesque NewManagers Jun 2012Document43 paginiOpalesque NewManagers Jun 2012Peter UrbaniÎncă nu există evaluări

- Risk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Document11 paginiRisk Perspectives: What Is Risk? Its Measurement, Dimensions, Modeling (Asset Classes, Risk Factors and Regimes)Peter UrbaniÎncă nu există evaluări

- Performance of NZ Super Vs Avg. Australian SuperfundDocument49 paginiPerformance of NZ Super Vs Avg. Australian SuperfundPeter UrbaniÎncă nu există evaluări

- Opalesque NewManagers July 2012Document45 paginiOpalesque NewManagers July 2012Peter UrbaniÎncă nu există evaluări

- Opalesque New Managers April 2012Document42 paginiOpalesque New Managers April 2012Peter UrbaniÎncă nu există evaluări

- Portfolio - Analytics Coskew and CoKurt VBA3Document131 paginiPortfolio - Analytics Coskew and CoKurt VBA3Peter Urbani0% (1)

- Opalesque New Managers March 2012Document37 paginiOpalesque New Managers March 2012Peter UrbaniÎncă nu există evaluări

- Do Emerging Managers Add Value (Mar 2012)Document19 paginiDo Emerging Managers Add Value (Mar 2012)Peter UrbaniÎncă nu există evaluări

- ETFdb Screening Model (March 2012)Document507 paginiETFdb Screening Model (March 2012)Peter UrbaniÎncă nu există evaluări

- Emerging Manager Time Series DecompositionDocument1 paginăEmerging Manager Time Series DecompositionPeter UrbaniÎncă nu există evaluări

- HFR 11april 2001 Young Funds ReportDocument7 paginiHFR 11april 2001 Young Funds ReportPeter UrbaniÎncă nu există evaluări

- Opalesque New Managers Feb 2012Document37 paginiOpalesque New Managers Feb 2012Peter UrbaniÎncă nu există evaluări

- Why Distributions Matter (16 Jan 2012)Document43 paginiWhy Distributions Matter (16 Jan 2012)Peter UrbaniÎncă nu există evaluări

- DGA July 2012 8872Document121 paginiDGA July 2012 8872Mike SchrimpfÎncă nu există evaluări

- Audit of InventoryDocument7 paginiAudit of InventoryDianne Antoinette Basallo0% (1)

- An Introduction To The Nielsen CompanyDocument17 paginiAn Introduction To The Nielsen CompanysinghbabitaÎncă nu există evaluări

- Global Audit Director Controller Worldwide Resume George BayidesDocument2 paginiGlobal Audit Director Controller Worldwide Resume George BayidesGeorgeBayidesÎncă nu există evaluări

- Audit Committees ChecklistDocument8 paginiAudit Committees ChecklistTarryn Jacinth NaickerÎncă nu există evaluări

- Fundamental and Technical Analysis - Technical PaperDocument16 paginiFundamental and Technical Analysis - Technical PaperGauree AravkarÎncă nu există evaluări

- ReviewerDocument27 paginiReviewerJedaiah CruzÎncă nu există evaluări

- Malayang Samahan NG Mga Manggagawa Sa M. Greenfield (Msmg-Uwp) v. RamosDocument3 paginiMalayang Samahan NG Mga Manggagawa Sa M. Greenfield (Msmg-Uwp) v. RamosAbigayle RecioÎncă nu există evaluări

- Shanti Business School: PGDM / PGDM-C Trimester - Iii End Term Examination JUNE - 2015Document6 paginiShanti Business School: PGDM / PGDM-C Trimester - Iii End Term Examination JUNE - 2015SharmaÎncă nu există evaluări

- I BD 20130711Document45 paginiI BD 20130711cphanhuyÎncă nu există evaluări

- A Brief Summary of The Caesars Entertainment Examiner's ReportDocument5 paginiA Brief Summary of The Caesars Entertainment Examiner's ReportUH_Gaming_ResearchÎncă nu există evaluări

- Flight: Head To HeadDocument68 paginiFlight: Head To HeadSaleh1fÎncă nu există evaluări

- Airline Industry One Fragile Industries Market Since TragiDocument4 paginiAirline Industry One Fragile Industries Market Since TragilsinožićÎncă nu există evaluări

- Business Directories 2017Document8 paginiBusiness Directories 2017Amjad ShareefÎncă nu există evaluări

- Moats Part OneDocument9 paginiMoats Part OnerobintanwhÎncă nu există evaluări

- Aditya Vikram Birla KimigrgDocument9 paginiAditya Vikram Birla KimigrgKeeran TamusyoÎncă nu există evaluări

- Tax Manager Job Description ExpertiseDocument1 paginăTax Manager Job Description Expertisetino mediamudaÎncă nu există evaluări

- Assurance Services: - DefinitionDocument27 paginiAssurance Services: - Definitionzanmatto22Încă nu există evaluări

- Iridium Enters Public Markets via GHL Acquisition CorpDocument31 paginiIridium Enters Public Markets via GHL Acquisition CorpshtshtshtÎncă nu există evaluări

- ASF Deacons Advice 2005Document4 paginiASF Deacons Advice 2005Saucebg1Încă nu există evaluări

- New York State Urban Development Corporation D/b/a Empire State DevelopmentDocument166 paginiNew York State Urban Development Corporation D/b/a Empire State DevelopmentjspectorÎncă nu există evaluări

- Class 12 Cbse Accountancy Sample Paper 2012 Model 2Document20 paginiClass 12 Cbse Accountancy Sample Paper 2012 Model 2Sunaina RawatÎncă nu există evaluări

- S&P 1000 Index - Dividends and Implied Volatility Surfaces ParametersDocument8 paginiS&P 1000 Index - Dividends and Implied Volatility Surfaces ParametersQ.M.S Advisors LLCÎncă nu există evaluări

- Mutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPDocument32 paginiMutual Fund - An Introduction: Project Report Submitted by Team B" Name Enrolment Number Roll Number Assigned in MSOPbholagangster1Încă nu există evaluări

- The Payment of The Bonus Act 1965Document28 paginiThe Payment of The Bonus Act 1965Arpita Acharjya100% (1)

- Summer Training Project Report: Banasthali University C-Scheme Jaipur Campus, RajasthanDocument74 paginiSummer Training Project Report: Banasthali University C-Scheme Jaipur Campus, Rajasthandrdipin100% (3)

- Working Capital RequirementsDocument2 paginiWorking Capital RequirementsAshuwajitÎncă nu există evaluări

- Cost Accounting Basics and Job Order CycleDocument22 paginiCost Accounting Basics and Job Order CycleJi Baltazar100% (1)

- HK Companies Ordinance Auditor ReportsDocument23 paginiHK Companies Ordinance Auditor Reportsbbe431Încă nu există evaluări