Documente Academic

Documente Profesional

Documente Cultură

2012 Outlook The Post-Stimulus Economy - Portuguese

Încărcat de

alexandrecezario0 evaluări0% au considerat acest document util (0 voturi)

61 vizualizări22 paginiTitlu original

2012 Outlook the Post-Stimulus Economy - Portuguese

Drepturi de autor

© Attribution Non-Commercial (BY-NC)

Formate disponibile

PDF, TXT sau citiți online pe Scribd

Partajați acest document

Partajați sau inserați document

Vi se pare util acest document?

Este necorespunzător acest conținut?

Raportați acest documentDrepturi de autor:

Attribution Non-Commercial (BY-NC)

Formate disponibile

Descărcați ca PDF, TXT sau citiți online pe Scribd

0 evaluări0% au considerat acest document util (0 voturi)

61 vizualizări22 pagini2012 Outlook The Post-Stimulus Economy - Portuguese

Încărcat de

alexandrecezarioDrepturi de autor:

Attribution Non-Commercial (BY-NC)

Formate disponibile

Descărcați ca PDF, TXT sau citiți online pe Scribd

Sunteți pe pagina 1din 22

EYE ON THE MARKET

PERSPECTIVAS PARA 2012

J.P. Morgan Private Bank

A economia ps-estmulo

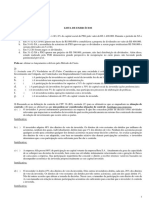

O ano de 2012 marca uma transio de abandono do estmulo monetrio e fscal extremo em nvel global, conforme ilustrado

pelo pr-do-sol. Em sua maior parte, a recuperao do setor privado ter de acontecer por conta prpria a partir daqui. As

notcias so melhores nos EUA do que na Europa ou no Japo. A sia est em expanso, mas o aperto nas taxas de juros est

trazendo o crescimento de volta a patamares mais realistas. A altura de cada rvore mostra a recuperao em cada varivel

relativa a sua queda durante a recesso. Mais informaes no interior da publicao.

No rastro da recesso, um grande volume de estmulos foi injetado na economia global. O nvel das polticas

de juros globais dos dfcits fscais defne a trajetria do sol. Apertos fscais esto programados praticamente

no mundo inteiro em 2012. Sobre a poltica monetria, embora a infao parea estar atingindo sua crista,

isso na maioria das vezes impede aumentos planejados nas taxas de juros, em vez de trazer outro perodo de

afrouxamento considervel. provvel que haja mais respostas em termos de poltica monetria na Europa, mas

seu objetivo primordial impedir o colapso da Unio Monetria com a desalavancagem de bancos e governos.

A altura de cada rvore mostra o nvel de recuperao de cada varivel em relao ao seu recuo anterior. Por

exemplo, os lucros do S&P, o varejo de luxo e o PIB alemo j recuperaram quase tudo que perderam durante a

recesso, ao passo que os preos dos imveis residenciais nos EUA e o ndice de emprego nos pases perifricos

da Europa ainda esto prximos s suas baixas ps-recesso. Os trs pontos de comparao para o clculo da

recuperao constituem o pico pr-ciclo; o patamar mais baixo dos ltimos quatro anos; e o valor atual. Uma

exceo: o reparo do balano dos imveis residenciais dos EUA calculado como a queda da dvida real por

residncia em relao ao pico.

Pases produtores de commodities, como Canad, Brasil e Austrlia, cujo PIB bem maior do que os pases do

sul da Europa no agregado, se recuperaram com rapidez. O trem-bala a sia, cuja produo e produtividade

sofreram apenas pequenas quedas, e que h muito tempo ofuscam os nveis pr-recesso. Contudo, o arrocho

do crdito e da poltica de taxas de juros provocaram uma desacelerao do trem-bala asitico e do restante

dos pases emergentes, em comparao com os ndices de crescimento meterico de 2010. A bola de vlei

defacionada a Unio Econmica e Monetria Europeia. Veja as fontes e defnies ao fnal desta apresentao.

How do you summarize a year that was in many respects indefnable? On one

hand, the European sovereign debt crisis, contracting housing markets and high

unemployment weighed heavy on all of our minds. But at the same time, record

corporate profts and strong emerging markets growth left reason for optimism.

So rather than look back, wed like to look ahead. Because if theres one thing that

weve learned from the past few years, its that while we cant predict the future,

we can certainly help you prepare for it.

To help guide you in the coming year, our Chief Investment Ofcer Michael

Cembalest has spent the past several months working with our investment

leadership across Asset Management worldwide to build a comprehensive view

of the macroeconomic landscape. In doing so, weve uncovered some potentially

exciting investment opportunities, as well as some areas where we see reason to

proceed with caution.

Sharing these perspectives and opportunities is part of our deep commitment to

you and what we focus on each and every day. We are grateful for your continued

trust and confdence, and look forward to working with you in 2011.

Most sincerely,

MARY CALLAHAN ERDOES

Chief Executive Ofcer

J.P. Morgan Asset Management

Ao nos dirigirmos a um novo ano, importante refetirmos sobre o que deixamos

para trs e a atual conjuntura para oferecer a voc nossa melhor opinio sobre os

rumos do mundo.

Os ltimos doze meses foram repletos de acontecimentos sem precedentes.

Testemunhamos a Primavera rabe e suas consequentes transformaes

governamentais, um devastador terremoto e tsunami no Japo, o primeiro

rebaixamento da dvida dos EUA na histria, uma contnua evoluo da crise da

dvida soberana na Europa e o encerramento formal de um confito no Iraque

que durou quase uma dcada.

Em meio a tais acontecimentos transformadores em todo o mundo, reconhecemos

que nosso trabalho de absorver tudo isso e identifcar oportunidades de

investimento apropriadas para o futuro torna-se ainda mais importante. Nosso

Chief Investment Ofcer Michael Cembalest, em parceria com nossas equipes de

investimento em todo o mundo, criou um perspicaz panorama para compreender

e avaliar as oportunidades e riscos globais que podemos esperar para o ano que

se aproxima.

Espero que voc goste da inteligente capa encomendada por Michael para

expressar em uma nica imagem o avano (ou a falta dele) desde a recesso

global de 2008/2009.

Desejamos a voc um Ano Novo repleto de sade e felicidade. E mais importante:

agradecemos pela contnua confana e credibilidade no J.P. Morgan.

Atenciosamente,

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

1

2012 Outlook

1

January 1, 2012

The Post-Stimulus Economy isnt all bad (there are as many tall trees on the cover as short ones), but its risks and uncertainties

have not declined that much from a year ago. One historical frame of reference we have been using is shown in the first chart: a

prior period of monetary and fiscal uncertainty during which markets were volatile, and sideways. The bull market began in

1982 when there was a clear path forward, even though a lot of the prior mess hadnt been completely dealt with. Where are we

this time in terms of monetary and fiscal uncertainty? While fiscal deficits are being reined in and household balance sheets are

healing, the long-term debt questions of the West remain mostly unanswered as of December 2011 (c2, c3).

With fiscal stimulus coming to an end and with only modest monetary policy easing in the pipeline (see inside cover for more

details), the private sector will increasingly have to make it on its own. The US is showing some resilience (c4), while

Europe and Asia are showing more signs of a slowdown. The big issue for 2012 will be how deep the European recession turns

out to be. Prior sovereign debt crises were almost always solved by a combination of currency devaluation, higher growth and

aggressive monetary easing (c5). In contrast, Europe is taking the path of most resistance: no growth, no devaluation, lots of

austerity and the decision to turn the ECB into a Bad Bank repository.

Equity markets are aware of this, priced as cheaply as they have been in decades (c6). Even assuming a 15% earnings

decline, the S&P 500 would still be priced at the cheap end of history. Factoring in valuation, volatility and the risks (both

known and unknown), our equity weightings are modestly lower than normal; the US is our largest regional position, and we

remain very underweight Europe. In this document, we walk through our views on Europe, the US and Asia, and our

investment priorities for 2012. Its a narrative in pictures; when many things are at their widest extremes in decades (equity

valuations, government debt, central bank balance sheets, depressed labor incomes, housing inventory, etc.), pictures are better

than words. In the appendix, some thoughts on Iran, and a history of European austerity and its connection to social unrest.

On the December EU summit. The European debt bubble will be unwound more slowly given the decision by the ECB and

member central banks to finance just about every asset held by EU banks, and the pressure on banks from governments to buy

more sovereign debt. Bilateral lending facilities for sovereigns may also be expanded if necessary. The risk of a 2012 Europe

meltdown may have melted, but what remains is a slow burn from a recession, a credit contraction and investors possibly selling

all theyve got to the ECB and other non-economic buyers.

Michael Cembalest

Chief Investment Officer

300

400

500

600

700

800

20

40

60

80

100

120

140

160

180

1972 1974 1976 1978 1980 1982

(c1) 1970s post-recovery equity

market wilderness

S&P 500 level Germany DAX level

Period of extreme

monetary and fiscal

uncertainty

Bull market

begins

30%

40%

50%

60%

70%

80%

90%

100%

110%

1970 1976 1982 1988 1994 2000 2006 2012

(c2) OECD debt levels

Percent of GDP, gross

30%

32%

34%

36%

38%

40%

42%

44%

46%

1970 1976 1982 1988 1994 2000 2006 2012

(c3) OECD budget deficits

Percent of GDP

Public revenues

Public expenditure

30

35

40

45

50

55

60

65

2007 2008 2009 2010 2011

(c4) Global manufacturing surveys

Purchasing Managers Index, sa

Euro area

US

Asia

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

5% 35% 65% 95%

Currency Devaluation, %

G

D

P

G

r

o

w

t

h

,

%

(c5) Fiscal adjustments, then & now

Prior

European

and Latin

adjustments

1975-2000

Europe

today

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

1956 1965 1974 1983 1992 2001 2010

(c6) Real S&P 500 earnings yield

Trailing earnings yield less core CPI

As of

12/16/11

Assuming a 15%

decline in earnings

A Economia Ps-estmulo no de todo ruim (a capa mostra a mesma quantidade de rvores altas e baixas), mas a reduo de seus riscos

e incertezas no foi to expressiva de um ano atrs at hoje. Um quadro de referncia histrica que temos usado aparece no primeiro grfco:

um perodo anterior de incerteza monetria e fscal durante o qual os mercados apresentaram volatilidade e seguiram pela tangente. A alta no

mercado teve incio em 1982, quando havia um evidente caminho adiante, muito embora boa parte da confuso anterior ainda no tivesse sido

resolvida por completo. Em que p estamos desta vez em termos de incerteza monetria e fscal? Se por um lado os dfcits fscais esto sendo

domados e as fnanas domsticas esto se recuperando, a maioria das questes de dvida de longo prazo do Ocidente permanece sem resposta

em dezembro de 2011 (g2, g3).

Com o estmulo fscal chegando ao fm e com o afrouxamento no mais que modesto da poltica monetria a caminho (mais informaes

so encontradas nesta publicao), cada vez mais o setor privado ter de se virar por conta prpria. Os EUA esto demonstrando

certa resilincia (g4), ao passo que Europa e sia esto dando mais sinais de desacelerao. A grande questo para 2012 ser descobrir

a profundidade da recesso na Europa. As crises da dvida soberana anteriores quase sempre foram sanadas por uma combinao de

desvalorizao cambial, elevao do crescimento e afrouxamento enrgico da poltica monetria (g5). Em contraste, a Europa est tomando

o rumo da mxima resistncia: nada de crescimento, nada de desvalorizao, muita austeridade e a deciso de transformar o BCE em um

repositrio de bancos de m qualidade.

Os mercados acionrios esto cientes disso, com os preos to baixos quanto em dcadas (g6). Mesmo supondo uma queda* de 15%

nos lucros, os preos do S&P 500 ainda assim estariam no extremo inferior da histria. Considerando a avaliao, a volatilidade e todos os

riscos (tanto os conhecidos como os desconhecidos), nossas alocaes em aes esto modestamente abaixo do normal; os EUA representam a

nossa maior posio regional; e permanecemos bastante desconcentrados na Europa. Neste documento, apresentamos um panorama de nossas

opinies sobre Europa, EUA e sia, e de nossas prioridades de investimento para 2012. Trata-se de um relato em imagens; quando muitas

coisas atingem seus maiores extremos em dcadas (avaliaes de aes, dvida pblica, fnanas dos bancos centrais, achatamentos salariais,

estoque de moradias, etc.), as imagens falam mais alto do que as palavras. No anexo, algumas consideraes sobre o Ir, e uma estria de

austeridade europeia e sua ligao com a agitao social.

Sobre a cpula da UE em dezembro. A bolha da dvida europeia ser resolvida mais lentamente, em funo da deciso do BCE e dos bancos

centrais afliados de fnanciar praticamente todos os ativos mantidos por bancos da UE. As linhas de crdito bilaterais para as dvidas soberanas

tambm podero ser ampliadas se necessrio. O risco de um desmoronamento da Europa em 2012 pode ter cado por terra, mas o que persiste

o ressentimento de uma recesso, uma contrao no crdito e investidores possivelmente vendendo tudo o que tm para o BCE e outros

compradores no econmicos.

Michael Cembalest

Chief Investment Offcer

2012 Outlook

1

January 1, 2012

The Post-Stimulus Economy isnt all bad (there are as many tall trees on the cover as short ones), but its risks and uncertainties

have not declined that much from a year ago. One historical frame of reference we have been using is shown in the first chart: a

prior period of monetary and fiscal uncertainty during which markets were volatile, and sideways. The bull market began in

1982 when there was a clear path forward, even though a lot of the prior mess hadnt been completely dealt with. Where are we

this time in terms of monetary and fiscal uncertainty? While fiscal deficits are being reined in and household balance sheets are

healing, the long-term debt questions of the West remain mostly unanswered as of December 2011 (c2, c3).

With fiscal stimulus coming to an end and with only modest monetary policy easing in the pipeline (see inside cover for more

details), the private sector will increasingly have to make it on its own. The US is showing some resilience (c4), while

Europe and Asia are showing more signs of a slowdown. The big issue for 2012 will be how deep the European recession turns

out to be. Prior sovereign debt crises were almost always solved by a combination of currency devaluation, higher growth and

aggressive monetary easing (c5). In contrast, Europe is taking the path of most resistance: no growth, no devaluation, lots of

austerity and the decision to turn the ECB into a Bad Bank repository.

Equity markets are aware of this, priced as cheaply as they have been in decades (c6). Even assuming a 15% earnings

decline, the S&P 500 would still be priced at the cheap end of history. Factoring in valuation, volatility and the risks (both

known and unknown), our equity weightings are modestly lower than normal; the US is our largest regional position, and we

remain very underweight Europe. In this document, we walk through our views on Europe, the US and Asia, and our

investment priorities for 2012. Its a narrative in pictures; when many things are at their widest extremes in decades (equity

valuations, government debt, central bank balance sheets, depressed labor incomes, housing inventory, etc.), pictures are better

than words. In the appendix, some thoughts on Iran, and a history of European austerity and its connection to social unrest.

On the December EU summit. The European debt bubble will be unwound more slowly given the decision by the ECB and

member central banks to finance just about every asset held by EU banks, and the pressure on banks from governments to buy

more sovereign debt. Bilateral lending facilities for sovereigns may also be expanded if necessary. The risk of a 2012 Europe

meltdown may have melted, but what remains is a slow burn from a recession, a credit contraction and investors possibly selling

all theyve got to the ECB and other non-economic buyers.

Michael Cembalest

Chief Investment Officer

300

400

500

600

700

800

20

40

60

80

100

120

140

160

180

1972 1974 1976 1978 1980 1982

(c1) 1970s post-recovery equity

market wilderness

S&P 500 level Germany DAX level

Period of extreme

monetary and fiscal

uncertainty

Bull market

begins

30%

40%

50%

60%

70%

80%

90%

100%

110%

1970 1976 1982 1988 1994 2000 2006 2012

(c2) OECD debt levels

Percent of GDP, gross

30%

32%

34%

36%

38%

40%

42%

44%

46%

1970 1976 1982 1988 1994 2000 2006 2012

(c3) OECD budget deficits

Percent of GDP

Public revenues

Public expenditure

30

35

40

45

50

55

60

65

2007 2008 2009 2010 2011

(c4) Global manufacturing surveys

Purchasing Managers Index, sa

Euro area

US

Asia

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

5% 35% 65% 95%

Currency Devaluation, %

G

D

P

G

r

o

w

t

h

,

%

(c5) Fiscal adjustments, then & now

Prior

European

and Latin

adjustments

1975-2000

Europe

today

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

1956 1965 1974 1983 1992 2001 2010

(c6) Real S&P 500 earnings yield

Trailing earnings yield less core CPI

As of

12/16/11

Assuming a 15%

decline in earnings

(g1) Selvageria dos mercados acionrios

ps-recuperao na dcada de 1970

Nvel do S&P 500 Alemanha - Nvel do DAX

(g2) Nveis de endividamento dos pases da OCDE

% do PIB (bruto)

(g3) Dfcits oramentrios dos pases da OCDE

% do PIB

(g4) Pesquisas da produo global

Purchasing Managers Index, sa

(g5) Ajustes fscais, antes e agora

Desvalorizao cambial, %

(g6) Rendimento real do S&P 500

Rendimento histrico menos IPC bsico

C

r

e

s

c

i

m

e

n

t

o

d

o

P

I

B

,

%

* No 4 trimestre de 2011, a porcentagem de pr-anncios de lucros negativos do S&P 500 correspondeu ao seu pico de 2001 e 2008. Outro

sinal: as empresas que prestaram informaes antes da Alcoa superaram os lucros consensuais para os ltimos 9 trimestres, ao passo que,

no 4 trimestre, fcaram atrs das estimativas em 2%.

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

2

EUROPA: exame de conscincia em meio a recesso

Um ano atrs, observamos que Jacques Delors (um dos principais arquitetos do euro) afrmou que a Europa precisava encontrar sua alma.

No momento em que estas palavras so escritas, ainda est procurando. Na ltima entrevista com Delors, ele admitiu que o euro j comeou

falho. Um de nossos grfcos usados com mais frequncia (g7) mostra como: veja o hiato na produo industrial entre Alemanha e Itlia,

que comeou em perfeita sincronia com a Unio Monetria Europeia. Em notas anteriores, destacamos como as disparidades nas taxas de

crescimento e emprego entre norte e sul da Europa nunca estiveram to evidentes como esto agora, mesmo durante a era da desvalorizao e

infao frequentes no sul do continente. Um projeto idealizado para promover a integrao acabou por compromet-la.

Evitarei os infndveis diagnsticos dos problemas, para ir direto ao desfecho: uma reformulao do euro com o barco andando, j que

os mercados perderam a confana na moeda (g8). Embora Grcia, Irlanda e Portugal estejam sob a tutela do estado, as necessidades de

emprstimo de pases maiores em 2012 tambm esto em questo (g9). S no 1 trimestre de 2012, a Itlia precisa emitir 112 bilhes em

notas do tesouro e obrigaes. O balano patrimonial do BCE (g10) pode ter de aumentar em 1 trilho para custear dvidas soberanas (g11)

e bancos subcapitalizados com reservas insufcientes (g12, g13), a despeito da oposio da Alemanha

1

. No se trata apenas de uma crise da

dvida soberana/bancria, conforme observado pelo avano da dvida das empresas, sobretudo na Espanha e em Portugal (g14). O grfco g5

mostra que o caminho normalmente seguido a desvalorizao externa. A Europa est tomando o rumo da desvalorizao interna mas, at o

momento, a Irlanda o nico pas que fez progresso (g15). Quanto Irlanda, seramos mais otimistas se no fosse por um acachapante ndice

de dvida/PIB de 140%, consequncia de sua deciso de socorrer os depositantes da UE nos bancos irlandeses.

1

O garoto batendo os ps no grfco do BCE retirado de Die Geschichte vom Suppen-Kaspar (Struwwelpeter).

2012 Outlook

2

January 1, 2012

EUROPE: soul-searching into a recession

A year ago, we noted that Jacques Delors (a principal architect of the Euro) said that Europe needed to find its soul. As of the

time of this writing, they are still looking for it. In Delors latest interview, he conceded that the Euro was flawed from the start.

One of our most frequently used charts (c7) shows how: look at the gap in industrial production between Germany and Italy,

which began like clockwork with the European Monetary Union. In prior notes, we highlighted how European North-South

disparities in growth and employment have never been larger than they are now, even during the era of frequent devaluation and

inflation in Southern Europe. A project designed to foster integration has ended up jeopardizing it.

I will avoid the endless diagnoses of the problems, and skip to the endgame: a mid-flight redesign of the Euro since markets

have lost confidence in it (c8). While Greece, Ireland and Portugal are wards of the state, 2012 borrowing needs of larger

countries are in question as well (c9). In Q1 2012 alone, Italy must issue 112 billion in bills and bonds. The ECB balance sheet

(c10) may have to grow by 1 trillion to support sovereigns (c11) and under-capitalized, under-reserved banks (c12, c13), despite

opposition from Germany

1

. This is not just a sovereign/banking crisis, as noted by the rise in corporate debt, particularly in

Spain and Portugal (c14). Chart c5 shows that external devaluation is the road typically taken. Europe is taking the internal

devaluation route, but so far, Ireland is the only country that has made progress (c15). As for Ireland, wed be more optimistic if

it werent for a crippling 140% debt to GNP ratio, a consequence of its decision to bail out EU depositors in Irish banks.

1

The boy stamping his feet in the ECB chart is from Die Geschichte vom Suppen-Kaspar (Struwwelpeter).

70

80

90

100

110

120

130

140

1982 1986 1990 1994 1998 2002 2006 2010

(c7) Death in Venice

Industrial Production Index, 1998 = 100, sa

Italy

Germany

Euro exchange

rate fixed

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

Jan-10 Jun-10 Nov-10 Apr-11 Sep-11

(c8) Sovereign 10-year yields

Percent

Belgium

Spain

Italy

France

0%

5%

10%

15%

20%

25%

30%

France Italy Spain

Maturing debt and interest

Primary deficit

(c9) Maturing debt, interest due and

primary deficits in 2012, Percent of GDP

355bn

327bn

203bn

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011

(c10) Central bank balance sheets

Percent of GDP

US

ECB

UK

Japan

ECB plus 1 trillion

20%

40%

60%

80%

100%

120%

140%

160%

1861 1886 1911 1936 1961 1986 2011

(c11) Italian debt/GDP, Total gross

general government debt/GDP, percent

WW I

WW II

0x

1x

2x

3x

4x

5x

6x

7x

U

S

P

O

L

I

T

G

R

G

E

R

B

E

F

R

S

P

A

T

D

K

U

K

I

R

L

(c12) Europe: bigger banks, bigger

problems, Liabilities, multiple of GDP

Foreign banks

Domestic banks

0%

1%

2%

3%

4%

5%

USbanks EUbanks

(c13) Loan loss provisions on

performing credit loans, Percent

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

S

P

B

E

P

R

T

U

K

F

R

I

T

D

K

N

O F

I

A

T

G

R

U

S

G

E

R

A

U

S

W

E

C

A

J

P

N

N

L

(c14) Change in non-financial corp.

debt from 2000-2010, Percent of GDP

90

95

100

105

110

115

120

125

130

135

140

2000 2002 2004 2006 2009 2011

(c15) Long road to convergence

Unit labor cost, index, Q1 2000 = 100, sa

Spain

Italy

Germany

France

Ireland

(g7) Morte em Veneza

ndice da produo industrial, 1998 = 100, sa

(g8) Rendimento dos ttulos soberanos de 10 anos

Percentual

(g9) Dvida vincenda, juros devidos e dfcits

primrios em 2012, % do PIB

2012 Outlook

2

January 1, 2012

EUROPE: soul-searching into a recession

A year ago, we noted that Jacques Delors (a principal architect of the Euro) said that Europe needed to find its soul. As of the

time of this writing, they are still looking for it. In Delors latest interview, he conceded that the Euro was flawed from the start.

One of our most frequently used charts (c7) shows how: look at the gap in industrial production between Germany and Italy,

which began like clockwork with the European Monetary Union. In prior notes, we highlighted how European North-South

disparities in growth and employment have never been larger than they are now, even during the era of frequent devaluation and

inflation in Southern Europe. A project designed to foster integration has ended up jeopardizing it.

I will avoid the endless diagnoses of the problems, and skip to the endgame: a mid-flight redesign of the Euro since markets

have lost confidence in it (c8). While Greece, Ireland and Portugal are wards of the state, 2012 borrowing needs of larger

countries are in question as well (c9). In Q1 2012 alone, Italy must issue 112 billion in bills and bonds. The ECB balance sheet

(c10) may have to grow by 1 trillion to support sovereigns (c11) and under-capitalized, under-reserved banks (c12, c13), despite

opposition from Germany

1

. This is not just a sovereign/banking crisis, as noted by the rise in corporate debt, particularly in

Spain and Portugal (c14). Chart c5 shows that external devaluation is the road typically taken. Europe is taking the internal

devaluation route, but so far, Ireland is the only country that has made progress (c15). As for Ireland, wed be more optimistic if

it werent for a crippling 140% debt to GNP ratio, a consequence of its decision to bail out EU depositors in Irish banks.

1

The boy stamping his feet in the ECB chart is from Die Geschichte vom Suppen-Kaspar (Struwwelpeter).

70

80

90

100

110

120

130

140

1982 1986 1990 1994 1998 2002 2006 2010

(c7) Death in Venice

Industrial Production Index, 1998 = 100, sa

Italy

Germany

Euro exchange

rate fixed

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

Jan-10 Jun-10 Nov-10 Apr-11 Sep-11

(c8) Sovereign 10-year yields

Percent

Belgium

Spain

Italy

France

0%

5%

10%

15%

20%

25%

30%

France Italy Spain

Maturing debt and interest

Primary deficit

(c9) Maturing debt, interest due and

primary deficits in 2012, Percent of GDP

355bn

327bn

203bn

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011

(c10) Central bank balance sheets

Percent of GDP

US

ECB

UK

Japan

ECB plus 1 trillion

20%

40%

60%

80%

100%

120%

140%

160%

1861 1886 1911 1936 1961 1986 2011

(c11) Italian debt/GDP, Total gross

general government debt/GDP, percent

WW I

WW II

0x

1x

2x

3x

4x

5x

6x

7x

U

S

P

O

L

I

T

G

R

G

E

R

B

E

F

R

S

P

A

T

D

K

U

K

I

R

L

(c12) Europe: bigger banks, bigger

problems, Liabilities, multiple of GDP

Foreign banks

Domestic banks

0%

1%

2%

3%

4%

5%

USbanks EUbanks

(c13) Loan loss provisions on

performing credit loans, Percent

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

S

P

B

E

P

R

T

U

K

F

R

I

T

D

K

N

O F

I

A

T

G

R

U

S

G

E

R

A

U

S

W

E

C

A

J

P

N

N

L

(c14) Change in non-financial corp.

debt from 2000-2010, Percent of GDP

90

95

100

105

110

115

120

125

130

135

140

2000 2002 2004 2006 2009 2011

(c15) Long road to convergence

Unit labor cost, index, Q1 2000 = 100, sa

Spain

Italy

Germany

France

Ireland

(g11) Relao dvida/PIB da Itlia, Relao

endividamento pblico bruto total/PIB (%)

(g12) Europa: bancos maiores, problemas

maiores, Passivos, mltiplo do PIB

(g13) Provises de perdas sobre a realizao de

emprstimos a vencer, %

(g14) Variao na dvida no fnanceira das

empresas no perodo 2000-2010, % do PIB

(g15) O longo caminho at a convergncia

Custo unitrio da mo-de-obra, ndice,

T1 2000 = 100, sa

2012 Outlook

2

January 1, 2012

EUROPE: soul-searching into a recession

A year ago, we noted that Jacques Delors (a principal architect of the Euro) said that Europe needed to find its soul. As of the

time of this writing, they are still looking for it. In Delors latest interview, he conceded that the Euro was flawed from the start.

One of our most frequently used charts (c7) shows how: look at the gap in industrial production between Germany and Italy,

which began like clockwork with the European Monetary Union. In prior notes, we highlighted how European North-South

disparities in growth and employment have never been larger than they are now, even during the era of frequent devaluation and

inflation in Southern Europe. A project designed to foster integration has ended up jeopardizing it.

I will avoid the endless diagnoses of the problems, and skip to the endgame: a mid-flight redesign of the Euro since markets

have lost confidence in it (c8). While Greece, Ireland and Portugal are wards of the state, 2012 borrowing needs of larger

countries are in question as well (c9). In Q1 2012 alone, Italy must issue 112 billion in bills and bonds. The ECB balance sheet

(c10) may have to grow by 1 trillion to support sovereigns (c11) and under-capitalized, under-reserved banks (c12, c13), despite

opposition from Germany

1

. This is not just a sovereign/banking crisis, as noted by the rise in corporate debt, particularly in

Spain and Portugal (c14). Chart c5 shows that external devaluation is the road typically taken. Europe is taking the internal

devaluation route, but so far, Ireland is the only country that has made progress (c15). As for Ireland, wed be more optimistic if

it werent for a crippling 140% debt to GNP ratio, a consequence of its decision to bail out EU depositors in Irish banks.

1

The boy stamping his feet in the ECB chart is from Die Geschichte vom Suppen-Kaspar (Struwwelpeter).

70

80

90

100

110

120

130

140

1982 1986 1990 1994 1998 2002 2006 2010

(c7) Death in Venice

Industrial Production Index, 1998 = 100, sa

Italy

Germany

Euro exchange

rate fixed

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

Jan-10 Jun-10 Nov-10 Apr-11 Sep-11

(c8) Sovereign 10-year yields

Percent

Belgium

Spain

Italy

France

0%

5%

10%

15%

20%

25%

30%

France Italy Spain

Maturing debt and interest

Primary deficit

(c9) Maturing debt, interest due and

primary deficits in 2012, Percent of GDP

355bn

327bn

203bn

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011

(c10) Central bank balance sheets

Percent of GDP

US

ECB

UK

Japan

ECB plus 1 trillion

20%

40%

60%

80%

100%

120%

140%

160%

1861 1886 1911 1936 1961 1986 2011

(c11) Italian debt/GDP, Total gross

general government debt/GDP, percent

WW I

WW II

0x

1x

2x

3x

4x

5x

6x

7x

U

S

P

O

L

I

T

G

R

G

E

R

B

E

F

R

S

P

A

T

D

K

U

K

I

R

L

(c12) Europe: bigger banks, bigger

problems, Liabilities, multiple of GDP

Foreign banks

Domestic banks

0%

1%

2%

3%

4%

5%

USbanks EUbanks

(c13) Loan loss provisions on

performing credit loans, Percent

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

S

P

B

E

P

R

T

U

K

F

R

I

T

D

K

N

O F

I

A

T

G

R

U

S

G

E

R

A

U

S

W

E

C

A

J

P

N

N

L

(c14) Change in non-financial corp.

debt from 2000-2010, Percent of GDP

90

95

100

105

110

115

120

125

130

135

140

2000 2002 2004 2006 2009 2011

(c15) Long road to convergence

Unit labor cost, index, Q1 2000 = 100, sa

Spain

Italy

Germany

France

Ireland

(g10) Balano patrimonial dos bancos centrais

% do PIB

(g11) Relao dvida/PIB da Itlia, Relao

endividamento pblico bruto total/PIB (%)

(g12) Europa: bancos maiores, problemas

maiores, Passivos, mltiplo do PIB

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

3

2012 Outlook

3

January 1, 2012

The irony of Italy in the eye of the storm is that since 1991, its primary budget has been in surplus (c16). However, Italy has no

choice given its debt burden of 1.9 trillion Euros (c11), a by-product of its 1980s fiscal crises. Italy has paid a price for this

austerity (and its low productivity), generating almost the lowest growth rate in the OECD over the last 20 years, ahead of only

Japan (c17). Its going to take a lot of work to convince markets that Italy is solvent, and that its debt is declining. We dont

think it is: c18 shows an optimistic and pessimistic case, although neither represents possible extremes. We assume near-term

funding costs of ~6%, which as Italian debt matures, bring its overall average cost of debt from 3.9% to 4.4% by 2014.

Will Maastricht 2.0 work, promising deficit limits that turn Italy and Spain into a Mediterranean Germany?

Germanys long-term plan appears to be: a heavy dose of austerity to reduce sovereign debt trajectories; commitments to run

German fiscal policy; a Franco-German governance framework to enforce it; after all of that, a lot more help from the ECB; a

lower Euro; and then, eventually, some kind of federalism (Eurobonds or other quasi-permanent transfers).

Its a risky strategy given the risk of a prolonged recession, superimposed on a region with 20 trillion in sovereign and

financial sector debt outstanding (c19). Spains economy, for example, is in free fall. See Appendix A for charts on how bad

things are in Spain, and a history of austerity and unrest in Europe over the last century.

Its not clear that the only difference between Germany and Italy/Spain is a slate of structural reforms. Even if reforms are

put in motion, they have a short-term growth cost, particularly when applied to labor markets (c20). So far, Italys proposed

adjustment is based more on higher taxes than lower spending; there has been less of a focus on addressing Italys yawning

productivity gaps vs. Germany, which are also noticeable in France (c21). On the matter of France, it is difficult to believe that it

will live by a 0.5% structural budget deficit limit; as shown a couple of weeks ago, it flies in the face of French budgetary history.

Investors are unconvinced: in 2011, US money market funds cut exposure to EU banks in half, and dollar bond issuance by EU

banks fell by 70%. Stress tests applied to EU banks, whose gross leverage is 26:1, are seen by many investors as unrealistic (e.g.,

the latest round stressed sovereign debt, but not household or corporate debt). As the EFSF, the IMF and other non-economic

buyers increase exposure, private investors may see this as an opportunity to exit (see Appendix C for some history).

Europe will try to finance budget deficits through the use of bilateral and ECB facilities. But they dont address the regions large

current account deficits which finance domestic consumption, particularly in France, Italy and Spain.

A lot of master plans look good on paper; so did Maastricht 1.0. Our sense is that Germany and other AAA countries will not

be able or willing to bear the ultimate cost

2

. If so, Mr. Delors will have to look for Europes soul someplace other than Berlin.

2

Debt to GDP levels in France (85%) and Germany (81%) are already elevated. Based on estimates of growth and govt deficits, the

German ratio is projected to decline, while the French one peaks at 87% in 2014. After including pro rata shares of existing and future

bilateral guarantees, assumed guarantees of Central Bank SMP purchases and risk of deficit slippage, both ratios rise well over 90%.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1970 1977 1984 1991 1998 2005 2012

(c16) Italian primary balance

Surplus/deficit before interest, % of GDP

Cyclically

adjusted

As reported

0%

1%

2%

3%

4%

5%

6%

7%

S

G

P

K

O

R

T

W

I

R

L

H

K

A

U

N

Z

C

A

U

S

N

O

I

C

E

F

I

S

P

S

W

E

N

L

U

K

A

T

G

R

B

E

D

K

P

R

T

F

R

S

W

Z

G

E

R

I

T

J

P

N

(c17) 20-year growth rates, 1991-2011

Percent

Italy

116%

119%

122%

125%

128%

131%

134%

2009 2010 2011 2012 2013 2014

(c18) Can Italy's debt stabilize?

Government debt, percent of GDP

Optimistic case:

Real GDP of 0.5%/0.5%

Primary balance: 2.6%/4.1%

Pessimistic case:

Real GDP of -1.5%/-0.5%

Primary balance:

1.3%/2.2%

5.0

6.5

8.0

9.5

11.0

12.5

14.0

2001 2003 2005 2007 2009 2011

(c19) Outstanding debt in Euro Area

Trillions, EUR

Financial

corporations

General

government

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

0 3 6 9 12

(c20) Growth response to structural

reforms, Cumulative percent change in

real GDP per capita

Tax Reform

Labor Reform

Financial

Reform

Trade Reform

Years

39%

44%

49%

54%

59%

64%

1970 1978 1986 1994 2002 2010

(c21) Vive la difference!

Real exports, France as a percent of Germany

A ironia de ver a Itlia no olho do furaco que, desde 1991, seu oramento tem apresentado supervit primrio (g16). Contudo, a Itlia no

tem escolha, tendo em vista o nus de sua dvida de 1,9 trilho de euros (g11), resultado de suas crises fscais da dcada de 1980. A Itlia pagou

um preo por essa austeridade (e sua baixa produtividade), quase gerando o mais baixo ndice de crescimento da OCDE nos ltimos 20 anos,

na frente apenas do Japo (g17). Ser muito trabalhoso convencer os mercados de que a Itlia solvente, e que sua dvida est caindo. Achamos

que no est: g18 mostra um caso otimista e um caso pessimista, muito embora nenhum dos dois represente possveis extremos. Consideramos

os custos de fnanciamento de curto prazo em cerca de 6%, o que, com o vencimento da dvida italiana, faz seu custo mdio geral da dvida

saltar de 3,9% para 4,4% at 2014.

Ser que o Maastricht 2.0 ir funcionar, prometendo limites de dfcit que transformem a Itlia e a Espanha em uma Alemanha

mediterrnea?

O plano de longo prazo da Alemanha parece ser o seguinte: uma forte dose de austeridade para reduzir a evoluo da dvida soberana; compromissos

para a gesto da poltica fscal alem; um marco de governana franco-alemo para aplic-la; depois de tudo isso, muito mais ajuda do BCE;

um euro mais baixo; e ento, fnalmente, algum tipo de federalismo (obrigaes europeias ou outras transferncias semipermanentes).

uma estratgia arriscada, considerando o risco de recesso prolongada, imposto a uma regio com 20 trilhes em dvida soberana e

do setor fnanceiro em aberto (g19). A economia da Espanha, por exemplo, est em queda livre. Ver, no Anexo A, grfcos sobre o quanto as

coisas vo mal na Espanha, e um histrico de austeridade e agitao na Europa nos ltimos cem anos.

No est claro se a nica diferena entre Alemanha e Itlia/Espanha uma leva de reformas estruturais. Mesmo que as reformas

sejam defagradas, elas apresentam um custo de crescimento de curto prazo, principalmente quando aplicadas aos mercados de trabalho

(g20). At o momento, a proposta de ajuste da Itlia se baseia mais no aumento dos impostos do que na reduo dos gastos; houve um foco

menor na soluo dos hiatos escancarados da produtividade em comparao com a Alemanha, que tambm so notveis na Frana (g21). E

por falar na Frana, difcil acreditar que ir sobreviver com um limite de dfcit oramentrio estrutural de 0,5%; conforme mostrado h

algumas semanas, uma afronta ao histrico oramentrio da Frana.

Os investidores no esto convencidos: em 2011, os fundos de curtssimo prazo norte-americanos cortaram a exposio aos bancos da

UE pela metade, e a emisso de obrigaes em dlar pelos bancos da UE sofreu queda de 70%. Testes de estresse aplicados aos bancos da

UE, cuja alavancagem bruta de 26 para 1, so considerados por muitos investidores como irrealistas (por exemplo, a ltima rodada testou

a dvida soberana, mas no a dvida das residncias ou das empresas). Com o aumento da exposio por parte do EFSF, do FMI e de outros

compradores no econmicos, os investidores privados podem encarar isso como uma oportunidade para sair (ver histrico no Anexo C).

A Europa tentar fnanciar os dfcits oramentrios com o uso de linhas bilaterais e do BCE. Porm, estes no solucionam os enormes

dfcits em transaes correntes que fnanciam o consumo interno, sobretudo na Frana, Itlia e Espanha.

Vrios planos diretores fcam lindos no papel; assim como o Maastricht 1.0. Nossa sensao que a Alemanha e outros pases de

classifcao AAA no tero condies ou interesse de arcar com o custo fnal

2

. Nesse caso, o Sr. Delors ter de procurar a alma da Europa

em algum lugar que no Berlim.

2

Os nveis de endividamento/PIB na Frana (85%) e Alemanha (81%) j esto elevados. Com base em estimativas de crescimento e dfcits pblicos, projeta-se queda para

o ndice alemo, ao passo que o ndice francs atinge seu pico em 87% no ano de 2014. Aps incluir parcelas proporcionais de garantias bilaterais existentes e futuras,

supostas garantias de compras do Banco Central por intermdio do SMP e o risco de derrapagem do dfcit, os dois ndices sobem bem acima de 90%.

2012 Outlook

3

January 1, 2012

The irony of Italy in the eye of the storm is that since 1991, its primary budget has been in surplus (c16). However, Italy has no

choice given its debt burden of 1.9 trillion Euros (c11), a by-product of its 1980s fiscal crises. Italy has paid a price for this

austerity (and its low productivity), generating almost the lowest growth rate in the OECD over the last 20 years, ahead of only

Japan (c17). Its going to take a lot of work to convince markets that Italy is solvent, and that its debt is declining. We dont

think it is: c18 shows an optimistic and pessimistic case, although neither represents possible extremes. We assume near-term

funding costs of ~6%, which as Italian debt matures, bring its overall average cost of debt from 3.9% to 4.4% by 2014.

Will Maastricht 2.0 work, promising deficit limits that turn Italy and Spain into a Mediterranean Germany?

Germanys long-term plan appears to be: a heavy dose of austerity to reduce sovereign debt trajectories; commitments to run

German fiscal policy; a Franco-German governance framework to enforce it; after all of that, a lot more help from the ECB; a

lower Euro; and then, eventually, some kind of federalism (Eurobonds or other quasi-permanent transfers).

Its a risky strategy given the risk of a prolonged recession, superimposed on a region with 20 trillion in sovereign and

financial sector debt outstanding (c19). Spains economy, for example, is in free fall. See Appendix A for charts on how bad

things are in Spain, and a history of austerity and unrest in Europe over the last century.

Its not clear that the only difference between Germany and Italy/Spain is a slate of structural reforms. Even if reforms are

put in motion, they have a short-term growth cost, particularly when applied to labor markets (c20). So far, Italys proposed

adjustment is based more on higher taxes than lower spending; there has been less of a focus on addressing Italys yawning

productivity gaps vs. Germany, which are also noticeable in France (c21). On the matter of France, it is difficult to believe that it

will live by a 0.5% structural budget deficit limit; as shown a couple of weeks ago, it flies in the face of French budgetary history.

Investors are unconvinced: in 2011, US money market funds cut exposure to EU banks in half, and dollar bond issuance by EU

banks fell by 70%. Stress tests applied to EU banks, whose gross leverage is 26:1, are seen by many investors as unrealistic (e.g.,

the latest round stressed sovereign debt, but not household or corporate debt). As the EFSF, the IMF and other non-economic

buyers increase exposure, private investors may see this as an opportunity to exit (see Appendix C for some history).

Europe will try to finance budget deficits through the use of bilateral and ECB facilities. But they dont address the regions large

current account deficits which finance domestic consumption, particularly in France, Italy and Spain.

A lot of master plans look good on paper; so did Maastricht 1.0. Our sense is that Germany and other AAA countries will not

be able or willing to bear the ultimate cost

2

. If so, Mr. Delors will have to look for Europes soul someplace other than Berlin.

2

Debt to GDP levels in France (85%) and Germany (81%) are already elevated. Based on estimates of growth and govt deficits, the

German ratio is projected to decline, while the French one peaks at 87% in 2014. After including pro rata shares of existing and future

bilateral guarantees, assumed guarantees of Central Bank SMP purchases and risk of deficit slippage, both ratios rise well over 90%.

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

1970 1977 1984 1991 1998 2005 2012

(c16) Italian primary balance

Surplus/deficit before interest, % of GDP

Cyclically

adjusted

As reported

0%

1%

2%

3%

4%

5%

6%

7%

S

G

P

K

O

R

T

W

I

R

L

H

K

A

U

N

Z

C

A

U

S

N

O

I

C

E

F

I

S

P

S

W

E

N

L

U

K

A

T

G

R

B

E

D

K

P

R

T

F

R

S

W

Z

G

E

R

I

T

J

P

N

(c17) 20-year growth rates, 1991-2011

Percent

Italy

116%

119%

122%

125%

128%

131%

134%

2009 2010 2011 2012 2013 2014

(c18) Can Italy's debt stabilize?

Government debt, percent of GDP

Optimistic case:

Real GDP of 0.5%/0.5%

Primary balance: 2.6%/4.1%

Pessimistic case:

Real GDP of -1.5%/-0.5%

Primary balance:

1.3%/2.2%

5.0

6.5

8.0

9.5

11.0

12.5

14.0

2001 2003 2005 2007 2009 2011

(c19) Outstanding debt in Euro Area

Trillions, EUR

Financial

corporations

General

government

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

0 3 6 9 12

(c20) Growth response to structural

reforms, Cumulative percent change in

real GDP per capita

Tax Reform

Labor Reform

Financial

Reform

Trade Reform

Years

39%

44%

49%

54%

59%

64%

1970 1978 1986 1994 2002 2010

(c21) Vive la difference!

Real exports, France as a percent of Germany

(g16) Saldo primrio da Itlia

Supervit/dfcit antes dos juros, % do PIB

(g17) ndices de crescimento de 20 anos, 1991-2011

Percentual

(g18) A dvida da Itlia capaz de se estabilizar?

Dvida pblica, % do PIB

(g19) Dvida em aberto na Zona do Euro

Trilhes de euros

(g20) Resposta do crescimento s reformas

estruturais, Variao percentual acumulada no PIB

real per capita

Anos

(g21) Vive la difference!

Exportaes reais, participao da Frana na Alemanha (%)

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

4

2012 Outlook

4

January 1, 2012

UNITED STATES: some decoupling from Europe and Asia, and the kindness of strangers

The US has generated better than expected news recently, including surveys of manufacturing (c22), light truck sales, consumer

spending, etc. Household balance sheets continue to heal, noted by the decline in credit card delinquency rates (c23). But the

strong spending data is a bit of a mystery. Some of it can be explained by the decline in debt service (rather than debt levels;

c24). But housing isnt contributing much of a boost, given negative pricing trends and massive shadow inventory (c25).

Theres also the question of how much spending can rise when disposable income is weak (c26); the income measure below

includes government transfers, and would look much weaker without them(c57 vs. c58). Perhaps the fact that the wealthiest

10% account for 30%-40% of spending explains its resilience. It looks like parts of the labor market are recovering (c27); if job

losses in construction, government and finance stop getting worse, the jobs picture would look much better. Labor incomes are

at multi-decade lows relative to corporate sales and GDP, but prospects for the large number of unemployed may be getting

better on the margin, based on jobless claims, manpower surveys, the household survey, and a survey of small business (NFIB).

This years 8% jump in capital spending (c28) was not a surprise. Since 2009 was the first year since 1932 in which the net

capital stock declined (c29), the rise was catch-up for a period of underinvestment. We have seen conflicting surveys regarding

capex intentions for 2012, with some higher (Citi) and some lower (ISM). We expect a positive contribution from the business

sector in 2012, and an economy-wide growth rate of ~2.25%. Commercial and industrial loan growth has been rising (c30),

offsetting continued weakness in residential loan demand, which supports some optimism on business spending for next year.

20

30

40

50

60

70

2001 2003 2005 2007 2009 2011

(c22) Some better news from

manufacturing surveys, Index, sa

New orders

Total

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2006 2007 2008 2009 2010 2011

(c23) Credit card delinquencies

Percent, 90+ days delinquent

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

60%

70%

80%

90%

100%

110%

120%

130%

140%

1980 1990 2000 2010

(c24) Household debt and debt

service, Percent of disposable income

Household

debt (LHS)

Debt service

(RHS)

0

1

2

3

4

5

6

7

8

9

2003 2005 2007 2009 2011

(c25) Shadow housing inventory

Millions of units

90+days

delinquent

Foreclosed

Bank-ownedreal estate

Existing

Current but underwater

-10%

-6%

-2%

2%

6%

10%

1990 1994 1998 2002 2006 2010

(c26) Spending vs. income

Percent change, QoQ, real, annualized, sa

Disposable income,

including govt. transfers

Consumption

91

92

93

94

95

96

97

98

99

100

33

34

35

36

37

38

39

1998 2001 2004 2007 2010

(c27) Bipolar labor market

Millions

Construction +

government +

finance (LHS)

Total excluding construction +

government + finance (RHS)

8

9

10

11

12

2003 2005 2007 2009 2011

(c28) Capital spending recovery

Billions of 2005 USD

-2%

0%

2%

4%

6%

8%

10%

'50 '60 '70 '80 '90 '00 '10

(c29) Capital stock

Percent change, YoY

Estimate for 2011

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011

(c30) C&I loan growth

Percent change, YoY

ESTADOS UNIDOS: certa desvinculao da Europa e da sia, e a bondade de estranhos

Os EUA geraram ultimamente notcias melhores do que o esperado, inclusive pesquisas da produo (g22), vendas de caminhonetes, consumo,

etc. As fnanas domsticas continuam a se recuperar, conforme indicado pela queda nos ndices de inadimplncia dos cartes de crdito (g23).

Mas o vigor dos dados de consumo um pouco misterioso. Parte deles pode ser explicada pelo recuo no servio da dvida (e no dos nveis

da dvida; g24). Mas a moradia no est contribuindo muito, dadas as tendncias negativas e o imenso estoque-sombra (g25). H tambm a

questo de quanto o consumo capaz de aumentar quando a renda disponvel estiver fraca (g26); a medida da renda abaixo inclui repasses

governamentais, e pareceria muito mais fraca sem esses repasses (g57 vs. g58). Talvez o fato de os 10% mais ricos responderem por 30 a 40%

do consume explique sua resilincia. Aparentemente, setores do mercado de trabalho esto se recuperando (g27); se as perdas de empregos na

construo, governo e fnanas parassem de piorar, a situao dos empregos teria aspecto muito melhor. Os salrios encontram-se nas mnimas

de vrias dcadas em relao ao faturamento das empresas e ao PIB, mas as perspectivas para o grande nmero de desempregados podem estar

melhorando na margem, com base nos pedidos de auxlio desemprego, pesquisas sobre a mo-de-obra, pesquisa das residncias e uma pesquisa

das pequenas empresas (NFIB).

O salto de 8% nos gastos de capital este ano (g28) no foi uma surpresa. Como 2009 foi o primeiro ano desde 1932 em que houve queda

do estoque de capital lquido (g29), o aumento foi uma compensao por um perodo de subinvestimentos. Constatamos pesquisas confitantes

no que diz respeito s intenes de investimentos em bens de capital para 2012, com algumas mais elevadas (Citi) e outros mais baixas (ISM).

Prevemos uma contribuio positiva do setor privado em 2012, e uma taxa de crescimento de cerca de 2,25% para a economia como um todo.

O crescimento dos emprstimos comerciais e industriais vem subindo (g30), compensando a defcincia contnua da demanda por emprstimos

para imveis residenciais, o que justifca certo otimismo com o gasto das empresas para o prximo ano.

2012 Outlook

4

January 1, 2012

UNITED STATES: some decoupling from Europe and Asia, and the kindness of strangers

The US has generated better than expected news recently, including surveys of manufacturing (c22), light truck sales, consumer

spending, etc. Household balance sheets continue to heal, noted by the decline in credit card delinquency rates (c23). But the

strong spending data is a bit of a mystery. Some of it can be explained by the decline in debt service (rather than debt levels;

c24). But housing isnt contributing much of a boost, given negative pricing trends and massive shadow inventory (c25).

Theres also the question of how much spending can rise when disposable income is weak (c26); the income measure below

includes government transfers, and would look much weaker without them(c57 vs. c58). Perhaps the fact that the wealthiest

10% account for 30%-40% of spending explains its resilience. It looks like parts of the labor market are recovering (c27); if job

losses in construction, government and finance stop getting worse, the jobs picture would look much better. Labor incomes are

at multi-decade lows relative to corporate sales and GDP, but prospects for the large number of unemployed may be getting

better on the margin, based on jobless claims, manpower surveys, the household survey, and a survey of small business (NFIB).

This years 8% jump in capital spending (c28) was not a surprise. Since 2009 was the first year since 1932 in which the net

capital stock declined (c29), the rise was catch-up for a period of underinvestment. We have seen conflicting surveys regarding

capex intentions for 2012, with some higher (Citi) and some lower (ISM). We expect a positive contribution from the business

sector in 2012, and an economy-wide growth rate of ~2.25%. Commercial and industrial loan growth has been rising (c30),

offsetting continued weakness in residential loan demand, which supports some optimism on business spending for next year.

20

30

40

50

60

70

2001 2003 2005 2007 2009 2011

(c22) Some better news from

manufacturing surveys, Index, sa

New orders

Total

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2006 2007 2008 2009 2010 2011

(c23) Credit card delinquencies

Percent, 90+ days delinquent

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

14.0%

60%

70%

80%

90%

100%

110%

120%

130%

140%

1980 1990 2000 2010

(c24) Household debt and debt

service, Percent of disposable income

Household

debt (LHS)

Debt service

(RHS)

0

1

2

3

4

5

6

7

8

9

2003 2005 2007 2009 2011

(c25) Shadow housing inventory

Millions of units

90+days

delinquent

Foreclosed

Bank-ownedreal estate

Existing

Current but underwater

-10%

-6%

-2%

2%

6%

10%

1990 1994 1998 2002 2006 2010

(c26) Spending vs. income

Percent change, QoQ, real, annualized, sa

Disposable income,

including govt. transfers

Consumption

91

92

93

94

95

96

97

98

99

100

33

34

35

36

37

38

39

1998 2001 2004 2007 2010

(c27) Bipolar labor market

Millions

Construction +

government +

finance (LHS)

Total excluding construction +

government + finance (RHS)

8

9

10

11

12

2003 2005 2007 2009 2011

(c28) Capital spending recovery

Billions of 2005 USD

-2%

0%

2%

4%

6%

8%

10%

'50 '60 '70 '80 '90 '00 '10

(c29) Capital stock

Percent change, YoY

Estimate for 2011

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2007 2008 2009 2010 2011

(c30) C&I loan growth

Percent change, YoY

(g24) Endividamento das famlias e servio da

dvida, % da renda disponvel

(g27) Mercado de trabalho bipolar

Milhes

(g22) Algumas notcias melhores das pesquisas

de produo, ndice, sa

(g25) Estoque de imveis residenciais-sombra

Milhes de unidades

(g23) Inadimplncia dos cartes de crdito

%, vencido h mais de 90 dias

(g26) Consumo vs. renda

Variao percentual, trimestral, real, anualizada, sa

(g27) Mercado de trabalho bipolar

Milhes

(g30) Crescimento dos emprstimos comerciais e

industriais, Variao percentual anual

(g25) Estoque de imveis residenciais-sombra

Milhes de unidades

(g28) Recuperao nos gastos de capital

Bilhes de dlares (2005)

(g26) Consumo vs. renda

Variao percentual, trimestral, real, anualizada, sa

(g29) Estoque de capital

Variao percentual anual

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

5

2012 Outlook

5

January 1, 2012

The elephant in the room: US government debt

The failure of the Super Committee to agree to a deficit reduction plan cannot be dismissed by saying, at least they will have

mandatory sequestered cuts instead. The Super Committee was supposed to be the beginning of a process, not the end. If it

ends here, the government debt burden is not stabilized (c31), and another $5 trillion in deficit reduction over 10 years would

still be needed to reach the sustainable debt levels projected in the latest CBO estimate. The problem: almost all government

revenues are already spoken for through mandatory programs or interest (c32), and the 2012 budget deficit is still projected at

6%-8%. As a result, there is not that much fiscal democracy left, as described by Eugene Steuerle of Brookings, leaving most

members of Congress with little to do but fight over the scraps that remain. US gross debt to GDP passed 100% for only the

second time in its history last month (c33). The last time this happened, the US was fighting a two-front war and preparing a

land invasion of Japan (Operation Downfall). As Walt Kellys Pogo once said, We have met the enemy, and he is us.

An extension of the payroll tax cut that is not fully funded reduces the austerity burden next year (c34), and leaves the Federal

debt issue to be dealt with in the future. So far, the US Treasury has survived based on the kindness of strangers: foreign

central banks increasing their holdings (c35), and purchases by the Fed (c36). It pays to be the worlds reserve currency (c37),

which is helping prevent the kind of market revolt that sent European debt markets reeling. However, with the backdrop below,

I am reminded of the following remark from late MIT economist Rudiger Dornbusch: Crisis takes a much longer time coming

than you think, and then it happens much faster than you would have thought.

30%

40%

50%

60%

70%

80%

90%

100%

110%

2004 2007 2010 2013 2016 2019

(c31) Long-term debt scenarios

Net debt to GDP, percent

CBOAugust Baseline

Budget Control Act Phases 1 & 2

CBO June Alternative case

$5 trillion

gap

-10%

0%

10%

20%

30%

40%

50%

60%

70%

1962 1971 1980 1989 1998 2007 2016

(c32) Percent of gov't. revenue not

committed to mandatory spending

0%

20%

40%

60%

80%

100%

120%

1900 1922 1944 1966 1988 2010

(c33) The US reaches its Pogo

moment, Gross debt to GDP, percent

100%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

1963 1971 1979 1987 1995 2003 2011

(c34) Fiscal adj. in 2012, Change in

cyclically-adjusted fiscal deficit, % of GDP

Fiscal tightening

Fiscal easing

Assuming payroll tax cuts

&unemployment insurance

benefits are extended

5%

10%

15%

20%

25%

30%

35%

1994 1998 2002 2006 2010

(c35) Foreign holdings of US debt

Percent of total net debt outstanding

Official sector

Private sector

6%

8%

10%

12%

14%

16%

18%

1994 1998 2002 2006 2010

(c36) Fed holdings of US debt

Percent of total net debt outstanding

1400 1575 1750 1925 2100

Portugal

Spain

Netherl

France

Britain

US

(c37) Reserve currency status does

not last forever

Year

-18

-14

-10

-6

-2

2

6

10

14

18

1999 2003 2007 2011

(c38) Quarterly state tax revenue

growth, Percent change, YoY

Some good news for municipal bond

buyers: state tax revenues have picked

up after some tax rate increases, and

states have also been shrinking their

payrolls and capex plans to balance

budgets. This has a broader economic

cost, but in isolation, supports the

credit risk of many state and local

issuers, particularly general obligation

and essential service revenue bonds.

O elefante na sala: a dvida pblica dos EUA

A incapacidade do Super Comit em chegar a um acordo sobre um plano de reduo do dfcit no pode ser ignorada afrmando-se que, ao

invs disso, pelo menos haver isolados cortes compulsrios. O Super Comit deveria ser o incio de um processo, e no o fm. Se acabar

aqui, o nus da dvida pblica deixa de ser estabilizado (g31), e outros US$ 5 trilhes em reduo do dfcit ao longo de 10 anos ainda seriam

necessrios para se alcanar os nveis de endividamento sustentvel projetados na mais recente estimativa da Comisso de Oramento do

Congresso (CBO). O problema: a quase totalidade das receitas pblicas j est comprometida por meio de programas compulsrios ou juros

(g32), e o dfcit oramentrio de 2012 ainda est projetado na faixa de 6 a 8%. Consequentemente, no resta tanta democracia fscal,

conforme descrito por Eugene Steuerle, da Brookings, deixando a maioria dos membros do Congresso com pouco a fazer a no ser brigar pelas

migalhas. A relao dvida bruta/PIB dos EUA ultrapassou a marca de 100% apenas pela segunda vez na histria no ms passado (g33). Da

ltima vez que isso aconteceu, os EUA estavam travando uma guerra em duas frentes e preparando uma invaso por terra ao Japo (Operao

Downfall). Como disse certa vez Pogo, de Walt Kelly: Encontramos o inimigo, e ele somos ns.

Uma ampliao do corte de impostos sobre a folha de pagamentos que no seja integralmente fundeada acaba por reduzir o nus da austeridade

no ano que vem (g34), deixando a questo da dvida do governo federal para ser resolvida no futuro. At o momento, o Tesouro dos EUA

sobreviveu com base na bondade de estranhos: bancos centrais estrangeiros aumentando seus investimentos (g35), e aquisies por parte

do Fed (g36). Vale a pena ser a moeda de reserva do mundo (g37), o que ajuda a impedir o tipo de insurreio que deixou os mercados de

dvida europeus cambaleantes. Entretanto, com o pano de fundo abaixo, sou relembrado acerca da seguinte observao do saudoso Rudiger

Dornbusch, economista do MIT: A crise leva bem mais tempo para se instalar do que se imagina, e a acontece bem mais rpido do que se

teria imaginado.

Algumas boas notcias para os compradores de

ttulos municipais: as arrecadaes de impostos

estaduais registraram recuperao aps alguns

aumentos nas alquotas dos impostos, e os

estados tambm vm promovendo cortes em

suas folhas de pagamento e capex a fm de

equilibrar os oramentos. Isso traz um custo

econmico mais amplo mas, de forma isolada,

apoia o risco de crdito de muitos emissores

estaduais e municipais, sobretudo em relao

a ttulos de obrigao geral e de receitas de

servios essenciais.

(g31) Cenrios de endividamento de longo prazo

ndice de endividamento lquido sobre o PIB (%)

(g33) EUA atingem seu momento Pogo,

Endividamento bruto/PIB (%)

(g32) % de receitas pblicas no empenhadas em

gastos compulsrios

(g34) Ajuste fscal em 2012, Variao do dfcit fscal

ajustado ciclicamente, % do PIB

(g35) Posies estrangeiras em dvida dos EUA

% da dvida lquida total em aberto

(g36) Posies do Fed na dvida dos EUA

% da dvida lquida total em aberto

(g37) O status de moeda de reserva no dura

para sempre

(g38) Crescimento trimestral das arrecadaes de

impostos estaduais, Variao percentual, anual

Eye on the Market

|

PERSPECTIVAS PARA 2012 1 de janeiro de 2012

6

2012 Outlook

6

January 1, 2012

ASIA: finding out what growth looks like without all the stimulus

2011 should have been a good year for Asian financial assets; after all, Asia generated the best combination of real GDP growth

and corporate profits growth of the three major regions (c39). We had positioned for this, but were not rewarded for it, as Asian

equities underperformed. The first problem: Asia over-stimulated, bringing policy rates net of headline inflation to zero. While

the recovery in GDP growth was V-shaped, it also brought with it much higher inflation (c40). Blunt policy measures were then

needed to rein it in. China is one illustrative example: money supply growth had to fall by more than half (from 30% to 13%) in

order to bring inflation under control (c41). The good news is that inflation is now in retreat, with the latest reading close to 4%.

The rate of Chinese RMB appreciation will probably slow, as it did from July 2008 to July 2010 when growth slowed down.

The second problem is European bank deleveraging, which runs the risk of a credit contraction in Asia, as the region was the

primary beneficiary of the expansion in EU and UK bank balance sheets (c42). While organic growth in Asia is real, in places

like China, growth has become more reliant on more and more credit (c43). The impact of monetary tightening, credit

tightening and slower growth in Europe can been seen in the decline in Chinese exports and manufacturing surveys (c44).

We are still optimistic on the region for the long haul. Consumer spending in China is growing at a rapid pace: pay attention to

growth rates in spending, rather than its share of GDP (c45). The region has been running current account surpluses for years,

reducing sensitivity to external shocks (c46). Reduced financing from Europe will be felt, but can be made up by domestic

sources given high saving rates. We expect 2012 to be an improvement over 2011, even at lower projected growth rates (c47).

0%

2%

4%

6%

8%

10%

12%

14%

16%

Real GDP Earnings

(c39) 2011 real GDP and earnings

growth, Percent change, YoY

US

Dev.

Europe

Asia ex.

Japan

0%

1%

2%

3%

4%

5%

6%

7%

8%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

2001 2003 2005 2007 2009 2011

(c40) Asia over-stimulated

Percent change, YoY

Headline CPI

(RHS)

Real GDP

(LHS)

-2%

0%

2%

4%

6%

8%

10%

10%

15%

20%

25%

30%

1998 2000 2003 2006 2009 2011

(c41) Chinese inflation comes down as

money supply tightens

%, YoY, lagging 6 months %, YoY

M2

(LHS)

CPI

(RHS)

100

200

300

400

500

600

700

800

900

1,000

2005 2006 2007 2008 2009 2010 2011

(c42) Bankenstein's Monster

Billions, USD

European

bank claims

on Asia ex.

Japan

US bank claims on

Asia ex. Japan

100%

120%

140%

160%

180%

200%

220%

240%

2002 2003 2005 2006 2008 2009 2011

(c43) Heavy reliance on credit, China's

society-wide credit as % of nominal GDP

40

42

44

46

48

50

52

54

56

58

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2005 2007 2009 2011

(c44) Chinese exports & manufacturing

survey, Percent change, YoY Index, sa

Exports

(LHS)

PMI

(RHS)

32%

35%

38%

41%

44%

47%

50%

1993 1996 1999 2002 2005 2008

1,300

3,300

5,300

7,300

9,300

11,300

13,300

(c45) Chinese consumer: watch the

level, not the share, % of GDP Yuan

Household

consumption/GDP

(LHS)

Annual retail

sales per capita

(RHS)

-2%

0%

2%

4%

6%

1990 1993 1996 1999 2002 2005 2008 2011

(c46) Asia's current account balance

Percent of GDP

Asia ex.

China/Japan

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

1994 1997 2000 2003 2005 2008 2011

(c47) Asia ex. Japan real GDP growth

rates, Percent change, YoY

Historical

Consensus

forecast

IMF

forecast

2012 Outlook

6

January 1, 2012

ASIA: finding out what growth looks like without all the stimulus

2011 should have been a good year for Asian financial assets; after all, Asia generated the best combination of real GDP growth