S-ar putea să vă placă și

- Camels RatingDocument12 paginiCamels RatingImtiaz AhmedÎncă nu există evaluări

- Authority To Lease - TemplateDocument4 paginiAuthority To Lease - TemplateMichael Manguba100% (3)

- Financial InstrumentDocument12 paginiFinancial InstrumentYoga PeryogaÎncă nu există evaluări

- Chapter 13B Transfer TaxDocument14 paginiChapter 13B Transfer TaxMark Gilbert Quintero100% (1)

- DUBAI BusinessDocument34 paginiDUBAI BusinessHassan Md RabiulÎncă nu există evaluări

- Project Report On Aac Block Manufacturing PlantDocument7 paginiProject Report On Aac Block Manufacturing PlantEIRI Board of Consultants and PublishersÎncă nu există evaluări

- Toaz - Info Quiz On Foreign Transactions PRDocument4 paginiToaz - Info Quiz On Foreign Transactions PRoizys131Încă nu există evaluări

- Authority To Lease J&JDocument5 paginiAuthority To Lease J&JJustin R. BuensucesoÎncă nu există evaluări

- How to have a Brilliant Career in Estate Agency: The ultimate guide to success in the property industry.De la EverandHow to have a Brilliant Career in Estate Agency: The ultimate guide to success in the property industry.Evaluare: 5 din 5 stele5/5 (1)

- Consultancy Agreement and Term SheetDocument8 paginiConsultancy Agreement and Term Sheetgantasri8Încă nu există evaluări

- Lesson Plan in General Math With GAD IntegrationDocument3 paginiLesson Plan in General Math With GAD IntegrationROMAR PINGOL100% (4)

- Bank Al Habib Car FinanceDocument9 paginiBank Al Habib Car Financefatima rahimÎncă nu există evaluări

- Diminishing Musharakah: Mahmood ShafqatDocument32 paginiDiminishing Musharakah: Mahmood ShafqatAli KhanÎncă nu există evaluări

- Diminishing Musharakah Presentation 02-06-08Document32 paginiDiminishing Musharakah Presentation 02-06-08AlHuda Centre of Islamic Banking & Economics (CIBE)Încă nu există evaluări

- Diminishing MusharakahDocument42 paginiDiminishing Musharakahatiqa tanveerÎncă nu există evaluări

- MUSHARAKAH MUTANAQISAH SlideDocument9 paginiMUSHARAKAH MUTANAQISAH SlideMohzafiq NizarÎncă nu există evaluări

- Chap 9Document22 paginiChap 9charlie simoÎncă nu există evaluări

- Islamic Modes of Financing: Diminishing MusharakahDocument40 paginiIslamic Modes of Financing: Diminishing MusharakahFaizan Ch0% (1)

- 2 Dim Musharaka.Document24 pagini2 Dim Musharaka.aiman100% (1)

- 4.2 Dim MusharakaDocument24 pagini4.2 Dim MusharakaAllauddinaghaÎncă nu există evaluări

- PropertyFinancing BaitiSingleTierDocument5 paginiPropertyFinancing BaitiSingleTierTaraqallah SalehÎncă nu există evaluări

- SBP IRFCC Chughtai LabDocument5 paginiSBP IRFCC Chughtai LabKay PeeÎncă nu există evaluări

- Diminishing Musharakah DocumentationDocument4 paginiDiminishing Musharakah DocumentationSyed Muhammad Hasan BilalÎncă nu există evaluări

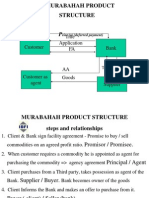

- Murabahah Product Structure: Title Application FADocument26 paginiMurabahah Product Structure: Title Application FAUmair UddinÎncă nu există evaluări

- Diminishing Musharakah MBLDocument17 paginiDiminishing Musharakah MBLAATIF IMTIAZÎncă nu există evaluări

- Diminishing Musharakah - MBL - PpsDocument17 paginiDiminishing Musharakah - MBL - Ppsgul_e_sabaÎncă nu există evaluări

- Diminishing Musharakah ConceptDocument26 paginiDiminishing Musharakah ConceptHasan Irfan SiddiquiÎncă nu există evaluări

- Meezan Bank PresentationDocument17 paginiMeezan Bank PresentationHussnain RazaÎncă nu există evaluări

- IF 2.5.2020 Diminishing MusharikahDocument17 paginiIF 2.5.2020 Diminishing MusharikahALI SHER HaidriÎncă nu există evaluări

- Test OneDocument6 paginiTest OneHemant Kumar RathodÎncă nu există evaluări

- Diminishing Musharakah MBLDocument17 paginiDiminishing Musharakah MBLUbaid ArifÎncă nu există evaluări

- Islamic Banking PresentationDocument50 paginiIslamic Banking PresentationPranay SahuÎncă nu există evaluări

- Islamic Financial ProductDocument13 paginiIslamic Financial ProductKelvin Lim Wei QuanÎncă nu există evaluări

- ISBF NotesDocument13 paginiISBF Notesmuneebmateen01Încă nu există evaluări

- Diminishing MusharakahDocument45 paginiDiminishing MusharakahIbn Bashir Ar-Raisi0% (1)

- (Lecture 5) - Other Investment Appraisal DecisionsDocument21 pagini(Lecture 5) - Other Investment Appraisal DecisionsAjay Kumar Takiar100% (1)

- Project Financing Program - VN QuestionnairesDocument3 paginiProject Financing Program - VN QuestionnairesAZHAR HASANÎncă nu există evaluări

- ATS TriumphDocument4 paginiATS TriumphsandeeprazzÎncă nu există evaluări

- Tijara CaseDocument5 paginiTijara CaseHammadÎncă nu există evaluări

- 07 Affin - Home - Invest I - ENG - v4 7 (1) (090819) Amended PDFDocument8 pagini07 Affin - Home - Invest I - ENG - v4 7 (1) (090819) Amended PDFMrHohoho97Încă nu există evaluări

- Pag-Ibig 2Document6 paginiPag-Ibig 2gdisenÎncă nu există evaluări

- Mvtfi PdsDocument9 paginiMvtfi PdsRoselind NadieraÎncă nu există evaluări

- Islamic Financing in PracticeDocument85 paginiIslamic Financing in PracticeAishiterru Gurl'sÎncă nu există evaluări

- Module 1 LeasesDocument12 paginiModule 1 LeasesMon RamÎncă nu există evaluări

- Lecture 6 Musharakah MutanaqisahDocument2 paginiLecture 6 Musharakah MutanaqisahGAN YU LINÎncă nu există evaluări

- Assignment Topic: Hire PurchaseDocument7 paginiAssignment Topic: Hire PurchaseusvathÎncă nu există evaluări

- Tijara CaseDocument5 paginiTijara CaseHammad Ahmad0% (1)

- Proposal Paper of Islamic Banking Facili PDFDocument14 paginiProposal Paper of Islamic Banking Facili PDFSayed Sharif HashimiÎncă nu există evaluări

- Meaning of The LoanDocument26 paginiMeaning of The LoanHarmanjot Singh RiarÎncă nu există evaluări

- IHF 18 19 Feb MUL 2013Document44 paginiIHF 18 19 Feb MUL 2013Habib Sultan KhelÎncă nu există evaluări

- PDS Equity Home Financing-IDocument8 paginiPDS Equity Home Financing-IAlan BentleyÎncă nu există evaluări

- Hire Purchase, Lease, and Instalment Purchase SystemDocument10 paginiHire Purchase, Lease, and Instalment Purchase SystemVipin Mandyam KadubiÎncă nu există evaluări

- An Utlook Into Particle Board Furniture Production in NigeriaDocument1 paginăAn Utlook Into Particle Board Furniture Production in NigeriaAyodeji AjideÎncă nu există evaluări

- Diminishing MusharakahDocument13 paginiDiminishing MusharakahMuhammad Farooq SiddiquiÎncă nu există evaluări

- PDS SMART Mortgage Flexi TawarruqDocument8 paginiPDS SMART Mortgage Flexi TawarruqNUR AQILAH NUBAHARIÎncă nu există evaluări

- Financing Land and Development Project QuestionsDocument12 paginiFinancing Land and Development Project QuestionsPrince EG DltgÎncă nu există evaluări

- VN Projects - S.Resources - QuestionnairesDocument3 paginiVN Projects - S.Resources - QuestionnairesAZHAR HASANÎncă nu există evaluări

- Islamic EconomicDocument16 paginiIslamic EconomicHatta SuperÎncă nu există evaluări

- Construction Loan GuaranteeDocument11 paginiConstruction Loan GuaranteeGeorgeÎncă nu există evaluări

- By: Deepti ChadhaDocument19 paginiBy: Deepti ChadhaDeepti ChadhaÎncă nu există evaluări

- Product Disclosure Sheet-Vehicle Financing-IDocument4 paginiProduct Disclosure Sheet-Vehicle Financing-IZainurul Farah ZainolÎncă nu există evaluări

- Arvind BankDocument24 paginiArvind BankDarshan GedamÎncă nu există evaluări

- Diminishing Musharaka IjarahBasedDocument22 paginiDiminishing Musharaka IjarahBasedArsalan AqeeqÎncă nu există evaluări

- Hire and PurcaseDocument40 paginiHire and PurcaseNeha SharmaÎncă nu există evaluări

- Islamic Housing FinanceDocument26 paginiIslamic Housing FinanceAbdelnasir HaiderÎncă nu există evaluări

- Banking and NBFC - Module 5 NBFC Produtcs Lending BasedDocument89 paginiBanking and NBFC - Module 5 NBFC Produtcs Lending Basednandhakumark152Încă nu există evaluări

- Islamic BankingDocument110 paginiIslamic BankingFaruk AbdullahÎncă nu există evaluări

- Foreign Exchange ProductsDocument1 paginăForeign Exchange ProductsFaruk AbdullahÎncă nu există evaluări

- Resolutions of Shariah Advisory Council of BNMDocument38 paginiResolutions of Shariah Advisory Council of BNMmuslimvillagesÎncă nu există evaluări

- Resolutions of Shariah Advisory Council of BNMDocument38 paginiResolutions of Shariah Advisory Council of BNMmuslimvillagesÎncă nu există evaluări

- Al-Wañd (Unilateral Promise) and ItsDocument24 paginiAl-Wañd (Unilateral Promise) and ItsFaruk Abdullah100% (1)

- Assets Liabilities and EquityDocument19 paginiAssets Liabilities and EquityTiyas KurniaÎncă nu există evaluări

- Microsoft Excel FunctionsDocument4 paginiMicrosoft Excel Functionssuri1700Încă nu există evaluări

- Bac 408 ModuleDocument54 paginiBac 408 ModuleJustus MasambaÎncă nu există evaluări

- ACJC Prelim H2 (Essays)Document26 paginiACJC Prelim H2 (Essays)lammofjvl0% (1)

- Case Analysis-Sasan Power LTDDocument19 paginiCase Analysis-Sasan Power LTDpranjaligÎncă nu există evaluări

- Retail Research: Systematic Investment Plan in Hybrid - Equity Oriented Funds vs. Recurring DepositDocument3 paginiRetail Research: Systematic Investment Plan in Hybrid - Equity Oriented Funds vs. Recurring DepositDhuraivel GunasekaranÎncă nu există evaluări

- Nama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZDocument5 paginiNama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZFikky Chandra SilabanÎncă nu există evaluări

- All-America Economic Survey 2Q17 Topline DataDocument16 paginiAll-America Economic Survey 2Q17 Topline DataCNBC.com100% (1)

- Proposal Form For LIC's Jeevan Akshay - II (Table No. 163) 1Document6 paginiProposal Form For LIC's Jeevan Akshay - II (Table No. 163) 1Anonymous W9VINoTzaÎncă nu există evaluări

- Statement of Cash Flows: Question InformationDocument48 paginiStatement of Cash Flows: Question InformationOKTAVIANAHURINGÎncă nu există evaluări

- Doing Business With DominicaDocument23 paginiDoing Business With DominicaOffice of Trade Negotiations (OTN), CARICOM SecretariatÎncă nu există evaluări

- Rate of Return One Project: Engineering EconomyDocument22 paginiRate of Return One Project: Engineering Economyann94bÎncă nu există evaluări

- Fin 201 Term Paper (Group L)Document33 paginiFin 201 Term Paper (Group L)omarsakib19984Încă nu există evaluări

- Deloitte - IFRS in Real EstateDocument13 paginiDeloitte - IFRS in Real EstateRD100% (1)

- India Bank Ifsc CodeDocument3.466 paginiIndia Bank Ifsc CodespakumaranÎncă nu există evaluări

- Feasibility Research On Rice Production For Zamboanga CooperativeDocument40 paginiFeasibility Research On Rice Production For Zamboanga Cooperativejeffrey ordonezÎncă nu există evaluări

- JulianDocument4 paginiJulianBhavesh GelaniÎncă nu există evaluări

- Googlefinance - Docs Editors HelpDocument7 paginiGooglefinance - Docs Editors HelpdkjogeÎncă nu există evaluări

- AS 37 (IAS Plus)Document6 paginiAS 37 (IAS Plus)SarmadÎncă nu există evaluări

- Fitch Affs Grupo ElektraDocument2 paginiFitch Affs Grupo ElektraSonia VasquezÎncă nu există evaluări

- Ifrs at A Glance IAS 21 The Effects of Changes In: Foreign Exchange RatesDocument4 paginiIfrs at A Glance IAS 21 The Effects of Changes In: Foreign Exchange Ratesمعن الفاعوريÎncă nu există evaluări

- Alpha Picks: Catching The Late Ray of Sunshine: Regional Morning NotesDocument5 paginiAlpha Picks: Catching The Late Ray of Sunshine: Regional Morning NotesFong Kah YanÎncă nu există evaluări

- F M Accounting - Lesson.1Document58 paginiF M Accounting - Lesson.1Versha ThakurÎncă nu există evaluări

- Fei 2123 PS3Document4 paginiFei 2123 PS3MarcoÎncă nu există evaluări