S-ar putea să vă placă și

- Giant Consumer ProductDocument2 paginiGiant Consumer ProductGazal GuptaÎncă nu există evaluări

- General Mills Inc Yoplait Custard Style Yogurt ADocument2 paginiGeneral Mills Inc Yoplait Custard Style Yogurt AQasim ImranÎncă nu există evaluări

- BM Simulation G12Document12 paginiBM Simulation G12Vinay KumarÎncă nu există evaluări

- Case Study - Business Strategy Game - Imperial BSGDocument10 paginiCase Study - Business Strategy Game - Imperial BSGSimrit Manihani79% (14)

- Stationery Zone Business Plan for GNIMS College MatungaDocument20 paginiStationery Zone Business Plan for GNIMS College MatungaVarun ParekhÎncă nu există evaluări

- Resolution No. 2009-001Document2 paginiResolution No. 2009-001Jerome Flojo0% (1)

- Group project report on smartphones MOJO and MOONDocument13 paginiGroup project report on smartphones MOJO and MOONjyothiÎncă nu există evaluări

- OLEBYo HX2 Jo RHX 7 XDocument7 paginiOLEBYo HX2 Jo RHX 7 XMothish Chowdary GenieÎncă nu există evaluări

- Global Compound Feed Market-By Ingredients, Supplements, Animal Type & Geography - Trends & Forecasts (2014-2020)Document13 paginiGlobal Compound Feed Market-By Ingredients, Supplements, Animal Type & Geography - Trends & Forecasts (2014-2020)Mordor IntelligenceÎncă nu există evaluări

- Submitted by - Group 4 Aakash Kumar Verma Bhini Yadav Rajat Garg Rohit Bhadola VarshikaDocument6 paginiSubmitted by - Group 4 Aakash Kumar Verma Bhini Yadav Rajat Garg Rohit Bhadola VarshikaAakash VermaÎncă nu există evaluări

- Basics Interior Design 01 - Retail Design PDFDocument186 paginiBasics Interior Design 01 - Retail Design PDFabinash Sethi100% (1)

- Markstrat Report - Company I - Nigel Quah - Yuanxin Gao - Zille HussnainDocument7 paginiMarkstrat Report - Company I - Nigel Quah - Yuanxin Gao - Zille HussnainZillay Hussnain BasijiÎncă nu există evaluări

- E Jeep Co.: Electronic Jeepney CorporationDocument30 paginiE Jeep Co.: Electronic Jeepney CorporationAshyyy123 GomezÎncă nu există evaluări

- BrandPRO Summary PDFDocument2 paginiBrandPRO Summary PDFBishruta BanerjeeÎncă nu există evaluări

- Team Scooby - BrandProDocument8 paginiTeam Scooby - BrandProAadithyan T GÎncă nu există evaluări

- Marketing Simulation Game ReportDocument5 paginiMarketing Simulation Game ReportNyein WaiÎncă nu există evaluări

- Case PanteneDocument21 paginiCase PanteneMuhammad Talha0% (2)

- Ryanair Inflight MagazineDocument29 paginiRyanair Inflight MagazineXXX100% (1)

- BrandproDocument5 paginiBrandprokarthikawarrierÎncă nu există evaluări

- Ned Bank Pay U AccountDocument4 paginiNed Bank Pay U AccountavarnÎncă nu există evaluări

- BrandPro Presentation TemplateDocument14 paginiBrandPro Presentation TemplateVansh Raj GautamÎncă nu există evaluări

- Misplaced Pride in Filipino Sachet Economy and Its Hidden CostsDocument2 paginiMisplaced Pride in Filipino Sachet Economy and Its Hidden CostspasigriveravengerÎncă nu există evaluări

- Brand Characteristics: Trendy - Declining Market Savvy Mojo 300 250 Pros Moon 570 510 Comp Was 516Document2 paginiBrand Characteristics: Trendy - Declining Market Savvy Mojo 300 250 Pros Moon 570 510 Comp Was 516karthikawarrierÎncă nu există evaluări

- Group 6 Section A MKTMG Clean EdgeDocument5 paginiGroup 6 Section A MKTMG Clean EdgeAtri RoyÎncă nu există evaluări

- Markstrat ReportDocument1 paginăMarkstrat Reportjipou59Încă nu există evaluări

- Argentina Team Coaching Practice Period 02Document28 paginiArgentina Team Coaching Practice Period 02qaisrani_1Încă nu există evaluări

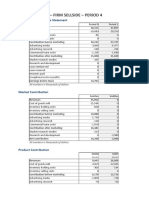

- Financial Report - Firm Sellside - Period 4: Company Profit & Loss StatementDocument73 paginiFinancial Report - Firm Sellside - Period 4: Company Profit & Loss StatementNancy suri100% (1)

- Questions. Parkin LaboratoriesDocument1 paginăQuestions. Parkin LaboratoriesRajagopalan GanesanÎncă nu există evaluări

- Global Strategic Management FrameworkDocument10 paginiGlobal Strategic Management FrameworkNavneet KumarÎncă nu există evaluări

- Industrial Organization How Is The U.S. American Fast Food Industry StructuredDocument10 paginiIndustrial Organization How Is The U.S. American Fast Food Industry StructuredLaura SchulzÎncă nu există evaluări

- Tinplate Company of India LTDDocument10 paginiTinplate Company of India LTDVikram AgarwalÎncă nu există evaluări

- Scope: Procter and GambleDocument30 paginiScope: Procter and GambleIrshad AhamedÎncă nu există evaluări

- General Mills Inc-Yoplait BDocument2 paginiGeneral Mills Inc-Yoplait BSabyasachi SahuÎncă nu există evaluări

- Markstrat Sample ReportDocument29 paginiMarkstrat Sample Reportananth080864Încă nu există evaluări

- Group 3 - Optical DistortionDocument15 paginiGroup 3 - Optical DistortionsrivatsaÎncă nu există evaluări

- MRS. BECTORS FOOD SPECIALITIES LTD. IPO DETAILSDocument7 paginiMRS. BECTORS FOOD SPECIALITIES LTD. IPO DETAILSJayantSinghJeenaÎncă nu există evaluări

- Changing Mindsets in Consumption Pattern of SOFT DRINK in Rural MarketDocument36 paginiChanging Mindsets in Consumption Pattern of SOFT DRINK in Rural MarketgouravawanishraviÎncă nu există evaluări

- Rural Marketing: M&M Tractors Vs TAFE TractorsDocument17 paginiRural Marketing: M&M Tractors Vs TAFE Tractorssiddharth_s91Încă nu există evaluări

- Clean Edge Razor-Case PPT-SHAREDDocument10 paginiClean Edge Razor-Case PPT-SHAREDPoorvi SinghalÎncă nu există evaluări

- PI Industries Ltd. - Initiating CoverageDocument19 paginiPI Industries Ltd. - Initiating Coverageequityanalystinvestor100% (1)

- Compare NPD Process With Cucina Fresca NPD ProcessDocument3 paginiCompare NPD Process With Cucina Fresca NPD ProcessNishwrathÎncă nu există evaluări

- Apple Iphone Life Cycle ManagementDocument8 paginiApple Iphone Life Cycle Managementrazvan6b49Încă nu există evaluări

- Dabur Case StudyDocument19 paginiDabur Case StudyMrunal MehtaÎncă nu există evaluări

- Introduction to the Markstrat ChallengeDocument35 paginiIntroduction to the Markstrat ChallengeSumeet MadwaikarÎncă nu există evaluări

- Capsim Core 2018 - Competition - Free 2018Document60 paginiCapsim Core 2018 - Competition - Free 2018ADITI SONIÎncă nu există evaluări

- General Mills Inc.Document7 paginiGeneral Mills Inc.uslumustafaÎncă nu există evaluări

- Supply Chain Coordination - The Bullwhip Effect: 3/14/2019 Rakesh V - IIM Lucknow 1Document11 paginiSupply Chain Coordination - The Bullwhip Effect: 3/14/2019 Rakesh V - IIM Lucknow 1neha bhatiaÎncă nu există evaluări

- Chester Capsim Report I Professor FeedbackDocument8 paginiChester Capsim Report I Professor Feedbackparamjit badyal100% (1)

- Introduction To Indian Detergent MarketDocument3 paginiIntroduction To Indian Detergent MarketAditya PrasadÎncă nu există evaluări

- Manage Marketing StrategyDocument36 paginiManage Marketing StrategyTaanÎncă nu există evaluări

- Strategy: Strategy and Tactics Differ Mainly Around Time ScaleDocument18 paginiStrategy: Strategy and Tactics Differ Mainly Around Time Scalemash68Încă nu există evaluări

- Pintura's Lena Powder Coating StrategyDocument9 paginiPintura's Lena Powder Coating StrategyRitika Sharma0% (1)

- Dettol Marketing Research For Understanding Consumer Evaluations of Brand ExtensionsDocument9 paginiDettol Marketing Research For Understanding Consumer Evaluations of Brand ExtensionsNaveen OraonÎncă nu există evaluări

- Marketing Strategy for Sonite and Vodite ProductsDocument9 paginiMarketing Strategy for Sonite and Vodite ProductsShashwat ShrivastavaÎncă nu există evaluări

- Colgate Case StudyDocument13 paginiColgate Case StudyRicha Vijayvargiya100% (1)

- Interrobang Season 6 Case Challenge - Defining B Natural's Brand Strategy & PositioningDocument9 paginiInterrobang Season 6 Case Challenge - Defining B Natural's Brand Strategy & PositioningNaveen TegarÎncă nu există evaluări

- Bajaj Electricals LimitedDocument9 paginiBajaj Electricals LimitedSivaraman P. S.Încă nu există evaluări

- Sun Pharma ReportDocument10 paginiSun Pharma ReportVijayalakshmi Kannan100% (1)

- Ajanta PackagingDocument2 paginiAjanta PackagingRajatÎncă nu există evaluări

- Week 8 - Team Erie Final PaperDocument14 paginiWeek 8 - Team Erie Final PaperSamantha TedejaÎncă nu există evaluări

- Sunfeast Yippee Noodle Brand Extension AnalysisDocument10 paginiSunfeast Yippee Noodle Brand Extension AnalysisHimanshu KumarÎncă nu există evaluări

- Markstrat Questionnaire - Suggested AnswersDocument6 paginiMarkstrat Questionnaire - Suggested AnswersHafizkamranashrafÎncă nu există evaluări

- MGFC10 Cheat SheetDocument5 paginiMGFC10 Cheat SheetĐức Hải NguyễnÎncă nu există evaluări

- Ome Merged PDFDocument311 paginiOme Merged PDFNavya MohankaÎncă nu există evaluări

- Global Marketing Management - SlidesDocument13 paginiGlobal Marketing Management - SlidesNoct PottsdamÎncă nu există evaluări

- Markstrat Report Round 0-3 Rubicon BravoDocument4 paginiMarkstrat Report Round 0-3 Rubicon BravoDebadatta RathaÎncă nu există evaluări

- Triumph-Germany Rnhyound 1Document6 paginiTriumph-Germany Rnhyound 1Mayank Neel GuptaÎncă nu există evaluări

- AIMA BizLab Report on Alpha Technologies LtdDocument23 paginiAIMA BizLab Report on Alpha Technologies LtdBhakti PatelÎncă nu există evaluări

- Consumers Firms and MarketsDocument4 paginiConsumers Firms and MarketsR rksÎncă nu există evaluări

- Hul ChannelauditDocument15 paginiHul ChannelauditKunal KumarÎncă nu există evaluări

- Franchise of Raftaar Delivery ServiceDocument14 paginiFranchise of Raftaar Delivery ServicedraqbhattiÎncă nu există evaluări

- Quiz Feedback - Coursera Week 4 Intro To FinanceDocument7 paginiQuiz Feedback - Coursera Week 4 Intro To FinanceVictoriaLukyanova0% (1)

- Retail Management Project on World of Titan and Fossil Watches StoresDocument14 paginiRetail Management Project on World of Titan and Fossil Watches StoresPuneet DhingraÎncă nu există evaluări

- Sony's Battle For Video Game Supremacy: John Sterman, Kahn Jekarl, Cate ReavisDocument24 paginiSony's Battle For Video Game Supremacy: John Sterman, Kahn Jekarl, Cate ReavissomÎncă nu există evaluări

- Pax 2 Vaporizer User ManualDocument14 paginiPax 2 Vaporizer User ManualTodd KnappÎncă nu există evaluări

- The Deep Focus 2015 Marketing Outlook ReportDocument30 paginiThe Deep Focus 2015 Marketing Outlook ReportDeepFocusNY100% (2)

- Roger Dawson - Ask For More Than You Expect To GetDocument4 paginiRoger Dawson - Ask For More Than You Expect To GetSuciu Lucian-RaresÎncă nu există evaluări

- Tanishq Case Study RetailDocument2 paginiTanishq Case Study RetailAnjali JainÎncă nu există evaluări

- Rose CultivationDocument16 paginiRose Cultivationani2sysÎncă nu există evaluări

- Rbi-Guidelines - Prepaid-Payments-Medianama - ComDocument7 paginiRbi-Guidelines - Prepaid-Payments-Medianama - Commixedbag100% (2)

- CGB Sample Test PDFDocument4 paginiCGB Sample Test PDFWaqas TayyabÎncă nu există evaluări

- Akhilesh (10 0)Document4 paginiAkhilesh (10 0)Roman ReignesÎncă nu există evaluări

- CASE: Wal-Mart Changes Tactics To Meet International Tastes: Chap 9: Global Logistics and Risk ManagementDocument5 paginiCASE: Wal-Mart Changes Tactics To Meet International Tastes: Chap 9: Global Logistics and Risk ManagementLinh LêÎncă nu există evaluări

- Gold Jewellery MarketDocument14 paginiGold Jewellery MarketKiranjot KaurÎncă nu există evaluări

- ICICI Bank HPCL Visa Contactless Credit Card: Membership GuideDocument20 paginiICICI Bank HPCL Visa Contactless Credit Card: Membership GuideRajat ChandelÎncă nu există evaluări

- A Strategic Analysis Project of Target CorporationDocument8 paginiA Strategic Analysis Project of Target CorporationJam EsÎncă nu există evaluări

- Interview Case Study - ElectroDocument6 paginiInterview Case Study - Electroeh07Încă nu există evaluări

- The Bullwhip Effect in HPs Supply ChainDocument9 paginiThe Bullwhip Effect in HPs Supply Chainsoulhudson100% (1)

- Chap 1Document14 paginiChap 1Gerald De SierraÎncă nu există evaluări

- Sample Business LettersDocument11 paginiSample Business LettersShyam MishraÎncă nu există evaluări