S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Grievance Redrassal ManagementDocument71 paginiGrievance Redrassal ManagementAzaruddin Shaik B Positive0% (1)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- Niraj-LSB CatalogueDocument8 paginiNiraj-LSB CataloguenirajÎncă nu există evaluări

- New 7 QC ToolsDocument106 paginiNew 7 QC ToolsRajesh SahasrabuddheÎncă nu există evaluări

- Programming in Excel VBADocument97 paginiProgramming in Excel VBAVladimir KojicÎncă nu există evaluări

- Combination Resume SampleDocument2 paginiCombination Resume SampleDavid SavelaÎncă nu există evaluări

- LG Market AnalysisDocument6 paginiLG Market AnalysisPrantor ChakravartyÎncă nu există evaluări

- 5 Things You Can't Do in Hyperion Planning: (And How To Do Them - . .)Document23 pagini5 Things You Can't Do in Hyperion Planning: (And How To Do Them - . .)sen2natÎncă nu există evaluări

- Annotated Glossary of Terms Used in The Economic Analysis of Agricultural ProjectsDocument140 paginiAnnotated Glossary of Terms Used in The Economic Analysis of Agricultural ProjectsMaria Ines Castelluccio100% (1)

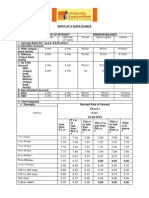

- Interest Fees Rates at A GlanceDocument10 paginiInterest Fees Rates at A GlanceRamji SimhadriÎncă nu există evaluări

- GATE'WAY To Maharatna NTPC: For Graduate EngineersDocument4 paginiGATE'WAY To Maharatna NTPC: For Graduate EngineersKsr ReddyÎncă nu există evaluări

- Basmati Patent Not MisunderstandingDocument3 paginiBasmati Patent Not MisunderstandingRamji SimhadriÎncă nu există evaluări

- RBI Report2010Document126 paginiRBI Report2010Ramji SimhadriÎncă nu există evaluări

- S L - T F: Ources OF ONG ERM InanceDocument16 paginiS L - T F: Ources OF ONG ERM InanceRamji SimhadriÎncă nu există evaluări

- Hotel ReportDocument6 paginiHotel ReportRamji SimhadriÎncă nu există evaluări

- Hotel IndustryDocument47 paginiHotel Industrysreenivasulu_5100% (3)

- IndianhotelindustryDocument6 paginiIndianhotelindustryRamji SimhadriÎncă nu există evaluări

- Sample Club BudgetsDocument8 paginiSample Club BudgetsDona KaitemÎncă nu există evaluări

- BBP TrackerDocument44 paginiBBP TrackerHussain MulthazimÎncă nu există evaluări

- TOGAF An Open Group Standard and Enterprise Architecture RequirementsDocument17 paginiTOGAF An Open Group Standard and Enterprise Architecture RequirementssilvestreolÎncă nu există evaluări

- AE - Teamcenter Issue Management and CAPA PDFDocument3 paginiAE - Teamcenter Issue Management and CAPA PDFsudheerÎncă nu există evaluări

- Notes On b2b BusinessDocument7 paginiNotes On b2b Businesssneha pathakÎncă nu există evaluări

- PriceListHirePurchase Normal6thNov2019Document56 paginiPriceListHirePurchase Normal6thNov2019Jamil AhmedÎncă nu există evaluări

- MKT 460 CH 1 Seh Defining Marketing For The 21st CenturyDocument56 paginiMKT 460 CH 1 Seh Defining Marketing For The 21st CenturyRifat ChowdhuryÎncă nu există evaluări

- SAP ISR Course ContentDocument1 paginăSAP ISR Course ContentSandeep SharmaaÎncă nu există evaluări

- BSC Charting Proposal For Banglar JoyjatraDocument12 paginiBSC Charting Proposal For Banglar Joyjatrarabi4457Încă nu există evaluări

- Retail Store Operations Reliance Retail LTD: Summer Project/Internship ReportDocument48 paginiRetail Store Operations Reliance Retail LTD: Summer Project/Internship ReportRaviRamchandaniÎncă nu există evaluări

- Ble Assignment 2019 21 BatchDocument2 paginiBle Assignment 2019 21 BatchRidwan MohsinÎncă nu există evaluări

- Business Plan RealDocument16 paginiBusiness Plan RealAjoy JaucianÎncă nu există evaluări

- 782 Sap SD Credit or Risk ManagementDocument12 pagini782 Sap SD Credit or Risk Managementrohit sharmaÎncă nu există evaluări

- Aplicatie Practica Catapulta TUVDocument26 paginiAplicatie Practica Catapulta TUVwalaÎncă nu există evaluări

- Importance of Human Resource ManagementDocument9 paginiImportance of Human Resource Managementt9inaÎncă nu există evaluări

- ISA 701 MindMapDocument1 paginăISA 701 MindMapAli HaiderÎncă nu există evaluări

- Walmart GRRDocument174 paginiWalmart GRRPatricia DillonÎncă nu există evaluări

- Save Capitalism From CapitalistsDocument20 paginiSave Capitalism From CapitalistsLill GalilÎncă nu există evaluări

- G12 ABM Marketing Lesson 1 (Part 1)Document10 paginiG12 ABM Marketing Lesson 1 (Part 1)Leo SuingÎncă nu există evaluări

- Southspin FASHION AWARDS-Title SponsorDocument32 paginiSouthspin FASHION AWARDS-Title SponsorManikanth Raja GÎncă nu există evaluări

- ITP - AutomationDocument43 paginiITP - AutomationidontlikeebooksÎncă nu există evaluări

- Coin Sort ReportDocument40 paginiCoin Sort ReportvishnuÎncă nu există evaluări

- CS 214 - Chapter 6: Architectural DesignDocument31 paginiCS 214 - Chapter 6: Architectural DesignAriel Anthony Fernando GaciloÎncă nu există evaluări