S-ar putea să vă placă și

- ValueInvestorInsight Issue 284Document24 paginiValueInvestorInsight Issue 284kennethtsleeÎncă nu există evaluări

- General Principles of Economics (Module-01)Document14 paginiGeneral Principles of Economics (Module-01)Mariam KachhiÎncă nu există evaluări

- VSA Book - Volume Spread AnalysisDocument21 paginiVSA Book - Volume Spread AnalysisScriberManÎncă nu există evaluări

- Agricultural Econ Week One LectureDocument16 paginiAgricultural Econ Week One Lectureismail ahmed100% (1)

- Health EconomicsDocument227 paginiHealth EconomicsagezeÎncă nu există evaluări

- Inventory Management SystemDocument3 paginiInventory Management SystemAkash DherangeÎncă nu există evaluări

- Statistics (Unit I)Document13 paginiStatistics (Unit I)BhartiÎncă nu există evaluări

- N. Gregory Mankiw: Powerpoint Slides by Ron CronovichDocument36 paginiN. Gregory Mankiw: Powerpoint Slides by Ron CronovichTook Shir LiÎncă nu există evaluări

- Introductiontosocialscience 111008005740 Phpapp02Document26 paginiIntroductiontosocialscience 111008005740 Phpapp02Amrela OlaÎncă nu există evaluări

- International Economics Homework 1 Due On Dec. 16 in Electronic VersionDocument9 paginiInternational Economics Homework 1 Due On Dec. 16 in Electronic VersionAsmita HossainÎncă nu există evaluări

- Bussines CommunicationDocument13 paginiBussines CommunicationCezar-Mihai CueruÎncă nu există evaluări

- Introduction To Social Policy Essay 1Document6 paginiIntroduction To Social Policy Essay 1Dan HarringtonÎncă nu există evaluări

- Soshal Well Fer Hand AwtDocument46 paginiSoshal Well Fer Hand AwtTalemaw MulatÎncă nu există evaluări

- Chapter 6 Introduction To Micro and Macro EconomicsDocument13 paginiChapter 6 Introduction To Micro and Macro EconomicsVinay ShettyÎncă nu există evaluări

- Empirical Tests of Status Consumption:Evidence From Women's Cosmetics - Angela Chao and Juliet B. SchorDocument25 paginiEmpirical Tests of Status Consumption:Evidence From Women's Cosmetics - Angela Chao and Juliet B. SchorAngela ChaoÎncă nu există evaluări

- Classical Management TheoriesDocument23 paginiClassical Management TheorieszhrÎncă nu există evaluări

- Basic Concept of Economics and Introduction To Micro Economics PDFDocument35 paginiBasic Concept of Economics and Introduction To Micro Economics PDFashish69250% (2)

- Understanding Micro and Macro Economics ConceptsDocument11 paginiUnderstanding Micro and Macro Economics ConceptsmaeÎncă nu există evaluări

- Social Responsibility To ConsumersDocument12 paginiSocial Responsibility To ConsumersJeh Ubaldo0% (1)

- Economic Growth and DevelopmentDocument39 paginiEconomic Growth and DevelopmentSmileCaturasÎncă nu există evaluări

- Effective Marketing StrategiesDocument104 paginiEffective Marketing StrategiesgbendoniÎncă nu există evaluări

- Principles of Marketing: Source: "Fundamentals of Marketing" by Josiah Go and Chiqui Escareal-GoDocument33 paginiPrinciples of Marketing: Source: "Fundamentals of Marketing" by Josiah Go and Chiqui Escareal-GoVia Marielle CalubaquibÎncă nu există evaluări

- A Science and Its History: Chapter 1Document14 paginiA Science and Its History: Chapter 1dfarias1989Încă nu există evaluări

- Chapter.7 OrganisationDocument10 paginiChapter.7 OrganisationVikāso Jāyasavālo100% (1)

- InterrelatedDocument2 paginiInterrelatedRaz MahariÎncă nu există evaluări

- Rural Development Programms: A Tool For Alleviation of Rural PovertyDocument10 paginiRural Development Programms: A Tool For Alleviation of Rural PovertyIJAR JOURNALÎncă nu există evaluări

- Major Difference Between Micro and Macro EconomicsDocument7 paginiMajor Difference Between Micro and Macro EconomicsHaren ShylakÎncă nu există evaluări

- Power N PoliticsDocument24 paginiPower N Politicspuneethreddy100% (1)

- WEEK3 LESSON 4 Production FunctionDocument4 paginiWEEK3 LESSON 4 Production FunctionSixd WaznineÎncă nu există evaluări

- Sociology-Class Lecture-1Document43 paginiSociology-Class Lecture-1Akash AminulÎncă nu există evaluări

- NLEP Newsletter Inaugural Issue PDFDocument10 paginiNLEP Newsletter Inaugural Issue PDFjmuhilanÎncă nu există evaluări

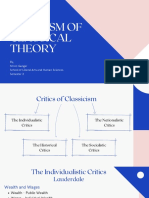

- Criticism of Classical TheoryDocument28 paginiCriticism of Classical TheoryShruti Gangar100% (1)

- Nature of EconomicsDocument12 paginiNature of EconomicsHealthyYOU100% (8)

- Factors Shaping Ethics: Culture, Faith, Upbringing & LawsDocument2 paginiFactors Shaping Ethics: Culture, Faith, Upbringing & LawsAnkit VyasÎncă nu există evaluări

- Mangerial EconomicsDocument55 paginiMangerial EconomicsSandeep GhatuaryÎncă nu există evaluări

- Running Head: Applications of Mathematics in Economics 1Document7 paginiRunning Head: Applications of Mathematics in Economics 1Akshat AgarwalÎncă nu există evaluări

- Economic Systems Multiple ChoiceDocument3 paginiEconomic Systems Multiple Choicechanese jean-pierre100% (1)

- ADDIS ABABA UNIVERSITY 2 DayDocument5 paginiADDIS ABABA UNIVERSITY 2 DayKaleb NegaÎncă nu există evaluări

- Understanding Price Elasticity for Business Pricing DecisionsDocument7 paginiUnderstanding Price Elasticity for Business Pricing DecisionsSubinÎncă nu există evaluări

- Managerial Economics MeaningDocument41 paginiManagerial Economics MeaningPaul TibbinÎncă nu există evaluări

- Applied AnthropologyDocument28 paginiApplied AnthropologyLuiz Claudio100% (1)

- C. Studies Handout - Economic ClimateDocument5 paginiC. Studies Handout - Economic ClimateChrisana LawrenceÎncă nu există evaluări

- Planning CommissionDocument12 paginiPlanning CommissionLata100% (1)

- Assignment On Intermediate Macro Economic (ECN 303) - USEDDocument6 paginiAssignment On Intermediate Macro Economic (ECN 303) - USEDBernardokpeÎncă nu există evaluări

- Origin and Definitions of EconomicsDocument2 paginiOrigin and Definitions of EconomicsRolly AbelonÎncă nu există evaluări

- Public Decision Making ProcessDocument30 paginiPublic Decision Making Processpaakwesi1015Încă nu există evaluări

- Intro to Microeconomics CourseDocument87 paginiIntro to Microeconomics Coursesewanyina muniruÎncă nu există evaluări

- The Economic Cooperation Organisation (Eco) A Short Note: Senior Economist at The SESRTCICDocument8 paginiThe Economic Cooperation Organisation (Eco) A Short Note: Senior Economist at The SESRTCICFaiza GandapurÎncă nu există evaluări

- ECN 306 - Marginalists SchoolDocument16 paginiECN 306 - Marginalists SchoolAbbieÎncă nu există evaluări

- 3) Market and ClassificationDocument28 pagini3) Market and ClassificationRanjit SatavÎncă nu există evaluări

- Chemistry ProjectDocument23 paginiChemistry Projecttwinklelee123450% (2)

- HR Chapter on Industrial Relations ConceptDocument11 paginiHR Chapter on Industrial Relations ConceptrhodaÎncă nu există evaluări

- Notes of Business Environment Unit 1Document5 paginiNotes of Business Environment Unit 1mohanraokp2279Încă nu există evaluări

- EconomicsDocument33 paginiEconomicsghazanfar_ravians623Încă nu există evaluări

- Book ChapterDocument9 paginiBook ChapterSiskawpÎncă nu există evaluări

- Microeconomics and MacroeconomicsDocument11 paginiMicroeconomics and Macroeconomicsshreyas kalekarÎncă nu există evaluări

- Chapter 10 - Lecturer Notes - Students PDFDocument12 paginiChapter 10 - Lecturer Notes - Students PDFAvneel Singh JrÎncă nu există evaluări

- Ethics TheoriesDocument55 paginiEthics TheoriesHussainMajedÎncă nu există evaluări

- Planning Commission in India MBADocument29 paginiPlanning Commission in India MBABabasab Patil (Karrisatte)100% (1)

- MBS I Sem Ch-1Document55 paginiMBS I Sem Ch-1bijay adhikari100% (2)

- Managerial Economics (Chapter 2)Document14 paginiManagerial Economics (Chapter 2)api-3703724Încă nu există evaluări

- Economics NotesDocument3 paginiEconomics NotesSushant SatyalÎncă nu există evaluări

- Multilateral BilateralDocument15 paginiMultilateral BilateralNada AntarÎncă nu există evaluări

- Eco - Ed. 428 Nepalese EconomyDocument7 paginiEco - Ed. 428 Nepalese EconomyHari PrasadÎncă nu există evaluări

- Banking Sector ReformsDocument13 paginiBanking Sector ReformsSahil NayyarÎncă nu există evaluări

- 01.chapter 1Document23 pagini01.chapter 1Mahbub Uz ZamanÎncă nu există evaluări

- Chapter 1 Intro To Economics - 9914937e c0f1 4fa8 9418 Bb9f4270ae76Document34 paginiChapter 1 Intro To Economics - 9914937e c0f1 4fa8 9418 Bb9f4270ae76riteshhpatel0945Încă nu există evaluări

- EconomicsDocument18 paginiEconomicsAbhay KuteÎncă nu există evaluări

- The Article Discusses 4th GenerationDocument3 paginiThe Article Discusses 4th GenerationYaswanth Kumar KolliparaÎncă nu există evaluări

- A Novel Hybrid Isolated GeneratingDocument7 paginiA Novel Hybrid Isolated GeneratingYaswanth Kumar KolliparaÎncă nu există evaluări

- Interference and Its ImportanceDocument21 paginiInterference and Its ImportanceYaswanth Kumar KolliparaÎncă nu există evaluări

- NATFM SyllabusDocument3 paginiNATFM SyllabusYaswanth Kumar KolliparaÎncă nu există evaluări

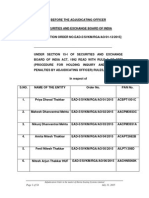

- Adjudication Order in The Matter of Harita Seating Systems Ltd.Document54 paginiAdjudication Order in The Matter of Harita Seating Systems Ltd.Shyam SunderÎncă nu există evaluări

- Stages of The Shipping CycleDocument2 paginiStages of The Shipping Cycleyesuplus2100% (3)

- PyndickDocument33 paginiPyndickAdeel ShaikhÎncă nu există evaluări

- Practice Exam 1Document4 paginiPractice Exam 1JamieÎncă nu există evaluări

- Marketing at Dashen PDFDocument29 paginiMarketing at Dashen PDFantehen0% (1)

- International Financial Markets GuideDocument49 paginiInternational Financial Markets GuidebalochmetroÎncă nu există evaluări

- Hq03 SalesDocument19 paginiHq03 SalesClarisaJoy SyÎncă nu există evaluări

- Parol Evidence Rule Final Exam OutlineDocument18 paginiParol Evidence Rule Final Exam OutlinelawgirleeÎncă nu există evaluări

- Avila Energy: Established and DiversifiedDocument23 paginiAvila Energy: Established and DiversifiedJames HudsonÎncă nu există evaluări

- Sample Format ThesisDocument38 paginiSample Format ThesisNonay BananÎncă nu există evaluări

- Carrier pricing strategies guideDocument6 paginiCarrier pricing strategies guideDua50% (2)

- Bid Document Drinking WaterDocument264 paginiBid Document Drinking Watersagarmohan123Încă nu există evaluări

- Microeconomics ALL IN ONE SOURCEDocument173 paginiMicroeconomics ALL IN ONE SOURCELoche AdraeneÎncă nu există evaluări

- Defination of M.EDocument6 paginiDefination of M.EGhulam AliÎncă nu există evaluări

- EPS R34 Export - 03.05 PDFDocument12 paginiEPS R34 Export - 03.05 PDFShehzad VayaniÎncă nu există evaluări

- RFQ BPA Architectural Design Supervision Services PDFDocument13 paginiRFQ BPA Architectural Design Supervision Services PDFcabdi saf safÎncă nu există evaluări

- Supply Contract Jafar Ag: 1. The Subject of The AgreementDocument10 paginiSupply Contract Jafar Ag: 1. The Subject of The AgreementJafar AGÎncă nu există evaluări

- Mathematics: Profit, Loss, Discount and AverageDocument9 paginiMathematics: Profit, Loss, Discount and AverageVishal JainÎncă nu există evaluări

- Marine Fish Marketing in IndiaDocument15 paginiMarine Fish Marketing in IndiaPrakash KcÎncă nu există evaluări

- Feenstra Taylor Econ CH06Document64 paginiFeenstra Taylor Econ CH06Arlene DaroÎncă nu există evaluări

- Concave ProgrammingDocument10 paginiConcave Programmingcharles luisÎncă nu există evaluări

- Assignment 1 - FinalDocument10 paginiAssignment 1 - FinalarafatÎncă nu există evaluări