S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (120)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (73)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- Case #1 BMWDocument3 paginiCase #1 BMWAmir ShahÎncă nu există evaluări

- IC Award No 946 of 2011Document21 paginiIC Award No 946 of 2011Wahab ChikÎncă nu există evaluări

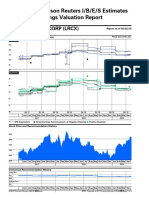

- Thomson Reuters IBES Estimates LRCXDocument4 paginiThomson Reuters IBES Estimates LRCXscribd_tsanÎncă nu există evaluări

- 2018 C ClassDocument31 pagini2018 C ClassI amÎncă nu există evaluări

- MY16 C Sedan PDFDocument37 paginiMY16 C Sedan PDFscribd_tsanÎncă nu există evaluări

- MY16 C Sedan PDFDocument37 paginiMY16 C Sedan PDFscribd_tsanÎncă nu există evaluări

- MY16 C Sedan PDFDocument37 paginiMY16 C Sedan PDFscribd_tsanÎncă nu există evaluări

- BigGold September 2011Document3 paginiBigGold September 2011scribd_tsanÎncă nu există evaluări

- Debunking The Gold Bubble Myth: By: Eric Sprott & Andrew MorrisDocument4 paginiDebunking The Gold Bubble Myth: By: Eric Sprott & Andrew Morrisscribd_tsan100% (1)

- A Quick History of Real Estate InvestingDocument7 paginiA Quick History of Real Estate Investingpetertumaini44Încă nu există evaluări

- Types of UnemploymentDocument22 paginiTypes of UnemploymentKusantha Rohan WickremasingheÎncă nu există evaluări

- Evaluation of Erp Implementation On Firm Performance A Case Study of AtntDocument8 paginiEvaluation of Erp Implementation On Firm Performance A Case Study of AtntrehankalsekarÎncă nu există evaluări

- Draft Resolution (Saudi Arabia, Usa, Japan)Document2 paginiDraft Resolution (Saudi Arabia, Usa, Japan)Aishwarya PotdarÎncă nu există evaluări

- The Slovak Spectator 15 - 40Document16 paginiThe Slovak Spectator 15 - 40The Slovak SpectatorÎncă nu există evaluări

- Impact of Information Technology On The Supply Chain Function of E-BusinessesDocument33 paginiImpact of Information Technology On The Supply Chain Function of E-BusinessesAbs HimelÎncă nu există evaluări

- BULATSDocument32 paginiBULATSVictorMartínezÎncă nu există evaluări

- Impact of Demonetizatio On Indian EconomyDocument5 paginiImpact of Demonetizatio On Indian EconomySuman sharmaÎncă nu există evaluări

- Text of The UnitDocument20 paginiText of The UnitvaleryÎncă nu există evaluări

- Who Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)Document294 paginiWho Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)dev guptaÎncă nu există evaluări

- Econom Is Survey Eng 1011Document178 paginiEconom Is Survey Eng 1011Goldi NegiÎncă nu există evaluări

- Barrall Irene Business Partner b2 Workbook Answer KeyDocument6 paginiBarrall Irene Business Partner b2 Workbook Answer KeyCyprusÎncă nu există evaluări

- Business Cycle: Is The Economy Getting Better or Worse?Document22 paginiBusiness Cycle: Is The Economy Getting Better or Worse?Earl Russell S PaulicanÎncă nu există evaluări

- 2011 HSC Exam EconomicsDocument20 pagini2011 HSC Exam Economicshappiinesslahxd0% (1)

- The Value of Project ManagementDocument6 paginiThe Value of Project ManagementRolly SocorroÎncă nu există evaluări

- Chapter 01: Globalization: Critical Thinking and Discussion QuestionsDocument3 paginiChapter 01: Globalization: Critical Thinking and Discussion QuestionsSulaima Asif100% (1)

- 13 - 34 The Influence of Monetary and Fiscal Policy On Aggregate DemandDocument36 pagini13 - 34 The Influence of Monetary and Fiscal Policy On Aggregate DemandDy AÎncă nu există evaluări

- 2012 BIMCO ISF Manpower StudyDocument6 pagini2012 BIMCO ISF Manpower StudycashelleÎncă nu există evaluări

- The Next Consumer Recession: Preparing NowDocument22 paginiThe Next Consumer Recession: Preparing NowPanther MelchizedekÎncă nu există evaluări

- Teks Economic EnglishDocument2 paginiTeks Economic EnglishRiri GustinÎncă nu există evaluări

- Mba Interntional Business: Analysing The Tourism Industry in MauritiusDocument39 paginiMba Interntional Business: Analysing The Tourism Industry in MauritiusVaishali SeechurnÎncă nu există evaluări

- 2233 AnnualRpt PDFDocument396 pagini2233 AnnualRpt PDFWilliam O OkolotuÎncă nu există evaluări

- LNTDocument202 paginiLNTKumar AbhishekÎncă nu există evaluări

- Macro Module 1 1Document126 paginiMacro Module 1 1Haileluel WondimnehÎncă nu există evaluări

- Introduction To Macroeconomics: DR - Leena A. KaushalDocument44 paginiIntroduction To Macroeconomics: DR - Leena A. KaushalHrangbung DarthangÎncă nu există evaluări

- Malaysia: Consumer Goods and Retail ReportDocument12 paginiMalaysia: Consumer Goods and Retail ReportAnand AgrawalÎncă nu există evaluări

- Menghadapi PersainganDocument36 paginiMenghadapi PersainganArief JuliandriÎncă nu există evaluări

- AIA Quarterly Investment InsightsDocument10 paginiAIA Quarterly Investment InsightsdesmondÎncă nu există evaluări