S-ar putea să vă placă și

- Statement of Cash Flows: Preparation, Presentation, and UseDe la EverandStatement of Cash Flows: Preparation, Presentation, and UseÎncă nu există evaluări

- Type Answers On This Side of The Page OnlyDocument40 paginiType Answers On This Side of The Page Only嘉慧Încă nu există evaluări

- BiiiimplmoniwbDocument34 paginiBiiiimplmoniwbShruti DubeyÎncă nu există evaluări

- Financial ModellingDocument39 paginiFinancial ModellingSaugat MahetaÎncă nu există evaluări

- Financial Analyst Modeling Budgeting in Denver CO Resume Preston BandyDocument2 paginiFinancial Analyst Modeling Budgeting in Denver CO Resume Preston BandyPrestonBandyÎncă nu există evaluări

- Cma of HostelDocument128 paginiCma of HostelkolnureÎncă nu există evaluări

- Gail India Oil and GasDocument38 paginiGail India Oil and GasKumar SinghÎncă nu există evaluări

- Untitled SpreadsheetDocument816 paginiUntitled SpreadsheetrakhalbanglaÎncă nu există evaluări

- Eclerx Services (Eclser) : Chugging Along..Document6 paginiEclerx Services (Eclser) : Chugging Along..shahavÎncă nu există evaluări

- Excel SampleDocument8 paginiExcel SampleVõ Văn PhúcÎncă nu există evaluări

- FULLIFRS Vs IFRSforSMES BAGSITDocument220 paginiFULLIFRS Vs IFRSforSMES BAGSITVidgezxc LoriaÎncă nu există evaluări

- 3.NPER Function Excel Template 1Document9 pagini3.NPER Function Excel Template 1w_fibÎncă nu există evaluări

- Financial ModellingDocument22 paginiFinancial ModellingSyam MohanÎncă nu există evaluări

- Different Types of Financial Models For Financial ModellingDocument4 paginiDifferent Types of Financial Models For Financial Modellingshivansh nangiaÎncă nu există evaluări

- Performance ApppraidDocument81 paginiPerformance ApppraidManisha LatiyanÎncă nu există evaluări

- Best Answer 3Document14 paginiBest Answer 3Chelsi Christine TenorioÎncă nu există evaluări

- Mapping New Expert-KEUDocument37 paginiMapping New Expert-KEUApdev OptionÎncă nu există evaluări

- SBDC Valuation Analysis ProgramDocument8 paginiSBDC Valuation Analysis ProgramshanÎncă nu există evaluări

- Income Statement: Khybey Tobacco Company LTDDocument15 paginiIncome Statement: Khybey Tobacco Company LTDMuzamil Ur rehmanÎncă nu există evaluări

- Eco ProjectDocument29 paginiEco ProjectAditya SharmaÎncă nu există evaluări

- FCFEDocument7 paginiFCFEbang bebetÎncă nu există evaluări

- Tata Steel - Financial Model - 2016-2025Document95 paginiTata Steel - Financial Model - 2016-2025Prabhdeep DadyalÎncă nu există evaluări

- Balanced ScorecardDocument13 paginiBalanced Scorecardatulmir50% (2)

- 2022 - Chapter09 Reorganizing UpdatedDocument21 pagini2022 - Chapter09 Reorganizing UpdatedElias MacherÎncă nu există evaluări

- Business Application System Development, Acquisition, Implementation, and MaintenanceDocument111 paginiBusiness Application System Development, Acquisition, Implementation, and MaintenanceSudhir PatilÎncă nu există evaluări

- Valuation Cash Flow A Teaching NoteDocument5 paginiValuation Cash Flow A Teaching NotesarahmohanÎncă nu există evaluări

- KTML Annual 2011Document364 paginiKTML Annual 2011Mian Asif BashirÎncă nu există evaluări

- Case AnalysisDocument29 paginiCase AnalysisLiza NabiÎncă nu există evaluări

- 1.FV Function Excel Template 1Document6 pagini1.FV Function Excel Template 1w_fibÎncă nu există evaluări

- Inventory Excel UploadDocument36 paginiInventory Excel Uploadaadi1012Încă nu există evaluări

- European World-Class Results Are Close To Overall Results, But Fewer Top Performers On CostDocument35 paginiEuropean World-Class Results Are Close To Overall Results, But Fewer Top Performers On Costkapnau007Încă nu există evaluări

- Sensitivity Analysis TableDocument3 paginiSensitivity Analysis TableBurhanÎncă nu există evaluări

- DCF Application - Asian PaintsDocument6 paginiDCF Application - Asian PaintsKashish PopliÎncă nu există evaluări

- L&T 4Q Fy 2013Document15 paginiL&T 4Q Fy 2013Angel BrokingÎncă nu există evaluări

- IPTC CMA Bank FormatDocument12 paginiIPTC CMA Bank FormatRadhesh BhootÎncă nu există evaluări

- Appropriations Dividend To Shareholders of Parent CompanyDocument30 paginiAppropriations Dividend To Shareholders of Parent Companyavinashtiwari201745Încă nu există evaluări

- Financial Modelling Cement CompanyDocument17 paginiFinancial Modelling Cement CompanyAdarsh KumarÎncă nu există evaluări

- Internal Audit Manager in San Jose CA Resume Andrew KatcherDocument4 paginiInternal Audit Manager in San Jose CA Resume Andrew KatcherAndrewKatcherÎncă nu există evaluări

- Ultimate Financial ModelDocument33 paginiUltimate Financial ModelTulay Farra100% (1)

- Verification of Assets and LiabilitiesDocument62 paginiVerification of Assets and Liabilitiesanon_672065362Încă nu există evaluări

- Financial Projections WorkbookDocument5 paginiFinancial Projections WorkbookIkram BelhajÎncă nu există evaluări

- Cash Budget Model Cash Budget Model - Case Study: InflowsDocument1 paginăCash Budget Model Cash Budget Model - Case Study: Inflowsayu nailil kiromahÎncă nu există evaluări

- YüklemeDocument58 paginiYüklemeCenk KurterÎncă nu există evaluări

- AuditSampleForms Master Sept 27 2011Document92 paginiAuditSampleForms Master Sept 27 2011Marta OsorioÎncă nu există evaluări

- PRM Self Assessment ToolDocument26 paginiPRM Self Assessment ToolBinson VargheseÎncă nu există evaluări

- Excel Power MovesDocument28 paginiExcel Power Moveslovingbooks1Încă nu există evaluări

- Mis Application in FinanceDocument28 paginiMis Application in Financeprakash_malickal100% (6)

- 03 Financial ModelDocument32 pagini03 Financial Modelromyka0% (1)

- Apv PDFDocument10 paginiApv PDFSam Sep A SixtyoneÎncă nu există evaluări

- ProjectDocument24 paginiProjectAayat R. AL KhlafÎncă nu există evaluări

- Mixed Use JK PDFDocument9 paginiMixed Use JK PDFAnkit ChaudhariÎncă nu există evaluări

- Cost of Capital Study 2011-2012-KPMGDocument52 paginiCost of Capital Study 2011-2012-KPMGanil14bits87Încă nu există evaluări

- REBNY Financial Statement Co-Op Condo - 2011Document3 paginiREBNY Financial Statement Co-Op Condo - 2011Jordan BeeberÎncă nu există evaluări

- TCS ValuationDocument264 paginiTCS ValuationSomil Gupta100% (1)

- FCFE CalculationDocument23 paginiFCFE CalculationIqbal YusufÎncă nu există evaluări

- Cold Storage Finance RohitDocument11 paginiCold Storage Finance RohitRohitGuleriaÎncă nu există evaluări

- 2GO Excel Calculation 1Document60 pagini2GO Excel Calculation 1w_fibÎncă nu există evaluări

- Existing Building AnalysisDocument15 paginiExisting Building AnalysisAmir H.TÎncă nu există evaluări

- FM HardDocument9 paginiFM HardKiran DalviÎncă nu există evaluări

- Financial Management 1Document36 paginiFinancial Management 1nirmljn100% (1)

- Democracy in Pakistan Hopes and HurdlesDocument3 paginiDemocracy in Pakistan Hopes and HurdlesAftab Ahmed100% (1)

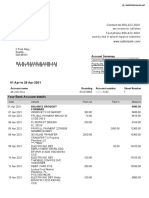

- Sutton Bank StatementDocument2 paginiSutton Bank StatementNadiia AvetisianÎncă nu există evaluări

- Joint Venture AgreementDocument7 paginiJoint Venture AgreementFirman HamdanÎncă nu există evaluări

- Poverty Alleviation Programmes in IndiaDocument4 paginiPoverty Alleviation Programmes in IndiaDEEPAK GROVERÎncă nu există evaluări

- Case AnalysisDocument3 paginiCase AnalysisAnurag KhandelwalÎncă nu există evaluări

- Rethinking Foreign Aid, SetaDocument5 paginiRethinking Foreign Aid, SetaAteki Seta CaxtonÎncă nu există evaluări

- Apollo Tyre Company: A Project Report ONDocument55 paginiApollo Tyre Company: A Project Report ONMOHITKOLLI100% (1)

- Poland Eastern Europe's Economic MiracleDocument1 paginăPoland Eastern Europe's Economic MiracleJERALDINE CANARIAÎncă nu există evaluări

- Court of Tax Appeals First Division: Republic of The Philippines Quezon CityDocument2 paginiCourt of Tax Appeals First Division: Republic of The Philippines Quezon CityPaulÎncă nu există evaluări

- AgricultureDocument40 paginiAgricultureLouise Maccloud100% (2)

- The Importance of Public TransportDocument1 paginăThe Importance of Public TransportBen RossÎncă nu există evaluări

- Contingent Liabilities For Philippines, by Tarun DasDocument62 paginiContingent Liabilities For Philippines, by Tarun DasProfessor Tarun DasÎncă nu există evaluări

- Lecture 3 Profit Maximisation and Competitive SupplyDocument36 paginiLecture 3 Profit Maximisation and Competitive SupplycubanninjaÎncă nu există evaluări

- U.S. Customs Form: CBP Form 7552 - Delivery Certificate For Purposes of DrawbackDocument2 paginiU.S. Customs Form: CBP Form 7552 - Delivery Certificate For Purposes of DrawbackCustoms FormsÎncă nu există evaluări

- What Are The Difference Between Governme PDFDocument2 paginiWhat Are The Difference Between Governme PDFIndira IndiraÎncă nu există evaluări

- Evio Productions Company ProfileDocument45 paginiEvio Productions Company ProfileObliraj KrishnarajÎncă nu există evaluări

- WHC Is Acquiring The Taxi Businesses From Transdev North AmericaDocument3 paginiWHC Is Acquiring The Taxi Businesses From Transdev North AmericaPR.comÎncă nu există evaluări

- ch07 Godfrey Teori AkuntansiDocument34 paginich07 Godfrey Teori Akuntansiuphevanbogs100% (2)

- Economy of Pakistan Course OutlineDocument2 paginiEconomy of Pakistan Course OutlineFarhan Sarwar100% (1)

- Mediclaim Format 1Document1 paginăMediclaim Format 1Urvashi JainÎncă nu există evaluări

- Triton Valves LTDDocument5 paginiTriton Valves LTDspvengi100% (1)

- Updated PJBF PresentationDocument16 paginiUpdated PJBF PresentationMuhammad FaisalÎncă nu există evaluări

- IB Economics SL8 - Overall Economic ActivityDocument6 paginiIB Economics SL8 - Overall Economic ActivityTerran100% (1)

- GLOBANT S.A. Globs of Exaggerated Growth and Accounting ShenanigansDocument26 paginiGLOBANT S.A. Globs of Exaggerated Growth and Accounting ShenanigansWarren TrumpÎncă nu există evaluări

- Chapter 6Document26 paginiChapter 6ANGEL MELLINDEZÎncă nu există evaluări

- Ethiopia Profile Enhanced Final 7th October 2021Document6 paginiEthiopia Profile Enhanced Final 7th October 2021sarra TPIÎncă nu există evaluări

- Neelam ReportDocument86 paginiNeelam Reportrjjain07100% (2)

- CookBook 08 Determination of Conformance - 09-2018Document4 paginiCookBook 08 Determination of Conformance - 09-2018Carlos LópezÎncă nu există evaluări

- China in Africa Research ProposalDocument20 paginiChina in Africa Research ProposalFrancky VincentÎncă nu există evaluări

- 2013-09-23 Rudin Management Company - James Capalino NYC Lobbyist & Client Search ResultDocument4 pagini2013-09-23 Rudin Management Company - James Capalino NYC Lobbyist & Client Search ResultConnaissableÎncă nu există evaluări