Documente Academic

Documente Profesional

Documente Cultură

Financial Time Seur 20120619

Încărcat de

cicita1Drepturi de autor

Formate disponibile

Partajați acest document

Partajați sau inserați document

Vi se pare util acest document?

Este necorespunzător acest conținut?

Raportați acest documentDrepturi de autor:

Formate disponibile

Financial Time Seur 20120619

Încărcat de

cicita1Drepturi de autor:

Formate disponibile

World Business Newspaper

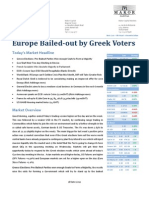

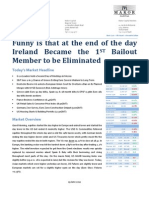

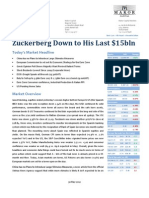

Jun 18 prev %chg

S&P 500 1347.29 1342.84 +0.33

Nasdaq Comp 2901.23 2872.8 +0.99

Dow Jones Ind 12766.04 12767.17 -0.01

FTSEurofrst 300 993.67 993.23 +0.04

Euro Stoxx 50 2155.64 2181.23 -1.17

FTSE 100 5491.09 5478.81 +0.22

FTSE All-Share UK 2847.84 2842.44 +0.19

CAC 40 3066.19 3087.62 -0.69

Xetra Dax 6248.2 6229.41 +0.30

Nikkei 8721.02 8569.32 +1.77

Hang Seng 19427.81 19233.94 +1.01

FTSE All World $ (u) 200.81 -

COMMODITIES

Jun 18 prev chg

Oil WTI $Jul 83.27 84.03 -0.76

Oil Brent $Aug 96.05 97.61 -1.56

Gold $ 1,628.40 1,623.30 5.10

price yield chg

US Gov 10 yr 101.50 1.59 0.00

UK Gov 10 yr 120.77 1.68 0.00

Ger Gov 10 yr 102.95 1.43 -0.04

Jpn Gov 10 yr 100.60 0.84 -0.02

US Gov 30 yr 106.50 2.68 -0.01

Ger Gov 2 yr 99.95 0.03 -0.04

Jun 18 prev chg

Fed Funds Ef 0.18 0.17 0.01

US 3mBills 0.08 0.09 -0.01

Euro Libor 3m 0.57 0.57 0.00

UK 3m 0.94 0.94 -

Prices are latest for edition

Jun 18 prev

$ per 1.258 1.262

$ per 1.567 1.564

per 0.803 0.807

per $ 78.9 78.7

per 123.6 123.2

$ index 81.7 81.5

SFr per 1.201 1.201

Jun 18 prev

per $ 0.795 0.792

per $ 0.638 0.639

per 1.246 1.239

per 99.26 99.40

index 83.4 83.1

index 88.35 88.58

SFr per 1.496 1.488

STOCK MARKETS CURRENCIES INTEREST RATES

World Markets

Austria 3.50 Malta 3.30

Bahrain Din1.5 Mauritius MRu90

Belgium 3.50 Morocco Dh40

Bulgaria Lev7.50 Netherlands 3.50

Croatia Kn29 Nigeria Naira715

Cyprus 3.30 Norway NKr30

Czech Rep Kc120 Oman OR1.50

Denmark DKr30 Pakistan Rupee 130

Egypt E19 Poland Zl 16

Estonia 4.00 Portugal 3.50

Finland 3.80 Qatar QR15

France 3.50 Romania Ron17

Germany 3.50 Russia 5.00

Gibraltar 2.30 Saudi Arabia Rls15

Greece 3.50 Serbia NewD370

Hungary Ft880 Slovak Rep 3.50

India Rup85 Slovenia 3.50

Italy 3.50 South Africa R28

Jordan JD3.25 Spain 3.50

Kazakhstan US$5.20 Sweden SKr34

Kenya Kshs300 Switzerland SFr5.70

Kuwait KWD1.50 Syria US$4.74

Latvia Lats3.90 Tunisia Din6.50

Lebanon LBP7000 Turkey TL7.25

Lithuania Litas15 UAE Dh15.00

Luxembourg 3.50 Ukraine 5.00

Macedonia Den220

Cover Price

9 7 7 0 1 7 4 7 3 6 1 2 8

2 5

In print and online

Tel: +44 20 7775 6000

Fax: +44 20 7873 3428

email: fte.subs@ft.com

www.ft.com/subscribetoday

Subscribe now

THE FINANCIAL TIMES

LIMITED 2012 No: 37,957

Printed in London, Liverpool, Dublin,

Frankfurt, Brussels, Stockholm, Milan,

Madrid, New York, Chicago, San Francisco,

Dallas, Orlando, Washington DC,

Johannesburg, Tokyo, Hong Kong,

Singapore, Seoul, Abu Dhabi, Sydney

Carrefour investors

block share plans

Shareholders at Carrefour

vented their anger at the

French retailers

underperformance by

blocking the allocation of

new share options to

directors at an annual

meeting in Paris. Page 15

EU banking push

A push by EU leaders to

create a single supervisor for

Europes largest banks is

rapidly gaining momentum

and could lead to an

agreement as soon as next

week. Page 2

Warships on alert

Russia is preparing two

warships to sail to Syria to

protect Russian citizens, in

a sign that it is taking

precautions against a

worsening of the security

situation there. Page 6;

www.ft.com/syria

Russian contingency

Russia is setting aside up to

$40bn to shore up the

economy in case the

eurozone crisis should

escalate and spread. Page 3

Hollandes challenge

Franois Hollande, Frances

president, will soon have to

take tough measures to

tackle the countrys public

finances. Page 2

Clean energy boost

Japan has revealed a plan to

boost investment in clean

energy sources, in a move

aimed at lowering dependence

on fossil fuels and nuclear

power. Page 7; Rich nations

must take a lead, Page 11

Fairfax to axe jobs

The Australian publisher

Fairfax Media is to cut about

a fifth of its workforce and

shrink its flagships Sydney

Morning Herald and The Age

to tabloid size as it seeks to

cut costs and halt a slide in

revenue. Page 15

Tehran talks tough

Iran engaged in intense and

tough exchanges with the

US and other world powers

as a third round of nuclear

talks began amid fears that a

peaceful resolution to the

stand-off over Tehrans

ambitions will prove elusive.

Page 6; Insurance ban, Page 26

India rejects rate cut

Indias central bank left

interest rates unchanged,

withstanding pressure from

big business and government

officials in New Delhi to give

the economy a boost. Page 3

Saudi heir apparent

King Abdullah of Saudi

Arabia has appointed his

half brother Prince Salman,

76, as the new heir apparent,

following the death of Crown

Prince Naif. Page 6

Credibility crisis

Alex Wynaendts, the chief

executive of life assurer

Aegon, has admitted that the

industry suffers from a

credibility problem because

it has sold over-complex

products to savers. Page 15

News Briefing

Separate section

Buying & investing in wine

Hopes rise again after correction

Just not cricket?

Learning from scams

Andrew Hill, Page 12

Banking union

A big but difficult eurozone fix. Analysis, Page 9

Tensions rise as MuslimBrotherhood

and old guard clash over Egypt election

By Borzou Daragahi in Cairo

Egypts Muslim Brotherhood

and the countrys old guard

stepped closer towards confron-

tation yesterday following

weekend presidential elections

and a flurry of manoeuvres by

the armed forces that appeared

to expand the militarys hold

over political life.

Although official results are

not due to be released until

Thursday, the Brotherhoods

Mohamed Morsi yesterday

claimed victory in the presiden-

tial poll, with 52 per cent of the

vote.

The announcement triggered

a heated exchange with rival

Ahmed Shafiq, former strong-

man Hosni Mubaraks last

prime minister, whose support-

ers accused the Brotherhood of

trying to steal the election.

The resulting uncertainty

alarmed investors and caused

the Egypt Stock Exchanges

benchmark EGX-30 index to

close down 3.42 per cent.

Egypts military leadership,

the Supreme Council of the

Armed Forces, insisted that it

would hand over power to civil-

ian rule at the end of June

despite recent moves that

seemed intended to consolidate

its hold on power.

The countrys Supreme Con-

stitutional Court, which

remains dominated by Mubarak

appointees, last week ordered

the dissolution of an elected

parliament controlled by the

Brotherhood and other Islam-

ists. On Sunday, after presiden-

tial polls closed, the military

issued a constitutional declara-

tion seeking to enshrine its

right to veto many presidential

decisions and maintain control

over the militarys own budget.

That declaration drew an

alarmed response from the US

defence department, which has

long had close ties to the Egyp-

tian armed forces.

We are deeply concerned

about the new amendments to

the constitutional declaration,

the Pentagon said. We support

the Egyptian people in their

expectation that the Supreme

Council of the Armed Forces

will transfer full power to a

democratically elected civilian

government.

In a televised press confer-

ence that appeared in part a

response to alarm over recent

developments among western

diplomats and domestic elites, a

spokesman for the military

leadership said it would not

interfere with the elected presi-

dents work. A new constitution

would be drafted by October

and new parliamentary elec-

tions held by December if

there are no obstacles or prob-

lems, the spokesman said.

The Brotherhood has refused

to recognise the constitutional

declaration, saying it is null

and void, and vowed to con-

vene the Islamist-dominated

constitutional assembly.

An administrative court was

scheduled to hold a hearing

yesterday on the legality of the

Brotherhood, which was out-

lawed under Mr Mubarak.

Military tightens grip, Page 4

We are deeply

concerned about the

new amendments to

the constitutional

declaration

Jubilant: supporters of the Muslim Brotherhood celebrate in Tahrir Square after Mohamed Morsi claimed victory yesterday Epa

By Robin Wigglesworth

in London, Chris Giles in

Los Cabos, Mexico and

Kerin Hope in Athens

The election victory for pro-

austerity parties in Greece

failed to assuage fears over the

eurozones future, as investors

ratcheted up the pressure on

policy makers by sending

Spains benchmark borrowing

costs to a new euro-era high.

Markets initially rallied on

news that New Democracy and

Pasok, two mainstream parties

that support the austerity condi-

tions of the eurozones bailout,

gained enough seats to form a

parliamentary majority in Ath-

ens. But the optimism was

swiftly deflated by dismal bad

bank loan figures in Spain that

underlined the countrys woes.

Data from the Bank of Spain

showed that the non-performing

loan ratio of Spanish banks rose

to 8.7 per cent of their outstand-

ing portfolios in April the

highest in almost two decades.

The eurozone has already

promised 100bn to help recapi-

talise Spains banks, but inves-

tors are concerned that it could

merely increase Madrids debt

burden and eventually lead to a

full sovereign rescue. Spains 10-

year bond yields, which move

inversely to prices, rose as high

as 7.28 per cent yesterday, while

the euro fell sharply against

most other key currencies.

Italys 10-year bond yields again

rose above the 6 per cent mark.

The Greek election merely

postpones a consideration of the

underlying problems, said

Sushil Wadhwani, a hedge fund

manager and former member of

the Bank of Englands Monetary

Policy Committee. The markets

are tiring of things that buy a

little time and do not deal with

the underlying issues.

At the start of the Group of 20

summit in Mexico, Jos Manuel

Barroso, European Commission

president, indicated that the

terms of Spains banking rescue

were still up for negotiation and

acknowledged fears that the

banking and fiscal crises are

increasingly intertwined: We

have been in favour, as far as

possible, in avoiding any kind of

contamination of financial debt

and sovereign debt.

While the commission and

many eurozone countries have

been in favour of using the con-

tinents rescue fund, the Euro-

pean Stability Mechanism, to

inject equity directly into failing

eurozone banks, Germany

remains opposed and has a

blocking vote on the ESM board.

Investors have begun to focus

their concerns on an EU summit

scheduled for the end of the

month, with many hoping pol-

icy makers will make progress

towards some form of banking

union to prevent the bloc from

unravelling. Hopes have centred

on proposals to create a com-

mon European bank supervisor

and rescue fund that would

shore up banks too big and too

weak to be rescued by their

national governments.

Eurozone woes, Page 2

Editorial Comment, Page 10

Comment, Page 11

Lex, Page 14

The Short View, Page 15

Markets, Pages 2628

www.ft.com/euro

Eurozones

Greek poll

honeymoon

shortlived

Spains borrowing costs at euroera high

Morgan Stanley discusses penance

with Irish nuns over bond lawsuit

By Jane Croft in London

A group of Irish nuns is close to

reaching a settlement with Mor-

gan Stanley after suing the US

bank in a dispute about losses

they incurred from an invest-

ment in euro-denominated

notes.

The Sisters of Charity of Jesus

and Mary, the Holy Faith Sisters

and the Irish Veterinary Benev-

olent Fund are among a group

of 132 Irish investors suing Mor-

gan Stanley and Saturns Invest-

ments Europe, a special-purpose

vehicle set up by the New York-

based bank.

The nuns and other investors

bought so-called Saturn notes

worth about 20m linked to

Dresdner Bank bonds in 2005

and 2006.

The lawsuit centres around

allegations that Morgan Stanley

failed to redeem the debt when

a mandatory redemption was

triggered in early 2009 after the

German banks credit rating

was cut below an agreed point.

The investors allege that Mor-

gan Stanley postponed redeem-

ing the notes until the value of

Dresdner Bank debt had recov-

ered to a level where the US

bank would incur no losses, but

caused the investors substan-

tial losses.

A trial was due to start at the

High Court in London yesterday

but was adjourned to allow both

parties more time for settlement

talks. Andrew Sutcliffe QC, rep-

resenting the claimants, told the

court the case has not yet set-

tled but we anticipate it may

and asked the judge to allow the

parties until later in the week to

resolve the terms.

Bloxham, the Irish stockbro-

ker that sold the notes to the

nuns and other investors, has

been added as a defendant.

The court heard that even if

the settlement was agreed, there

was still outstanding litigation

between Morgan Stanley and

Bloxham.

The US bank said in a filing

last year that it had no dealings

with any of the noteholders,

since it sold the notes directly to

Bloxham.

Morgan Stanley declined to

comment yesterday.

Bloxham, one of Irelands old-

est stockbrokers, was last

month forced to cease trading

after the Central Bank of Ire-

land discovered financial irregu-

larities. The Irish broker has

transferred its asset manage-

ment unit to Davy, Irelands

largest stockbroker.

Lawyers say that they expect

further litigation relating to

structured products sold at the

height of the economic boom,

because there is a six-year time

limit for starting such proceed-

ings in the UK.

Discord expected

Canada, the Holy See and

dozens of other countries have

raised pet objections before

this weeks Rio+20 sustainable

development conference, which

the UN says is the biggest

event it has organised. They

underline the doubts that many

have about what will be

achieved by the 100plus

leaders expected to fly in for

the meeting in Brazil by the

time it ends on Friday.

Report, Page 7

EUROPE Tuesday June 19 2012

JUNE 19 2012 Section:FrontBack Time: 18/6/2012 - 20:30 User: millern Page Name: 1FRONT EUR, Part,Page,Edition: EUR, 1, 1

2

FINANCIAL TIMES TUESDAY JUNE 19 2012

FINANCIAL TIMES

Number One Southwark Bridge, London SE1 9HL

SUBSCRIPTIONS AND CUSTOMER

SERVICE:

Tel: +1 44 207 775 6000

fte.subs@ft.com

www.ft.com/subscribetoday

LETTERS TO THE EDITOR:

Fax: +44 20 7873 5938

letters.editor@ft.com

ADVERTISING:

Tel: +44 20 7873 3794

emeaads@ft.com

EXECUTIVE APPOINTMENTS:

Tel: +971 4299 754

www.execappointments.com

Published by: The Financial Times Limited, Number One Southwark Bridge, London SE1 9HL, United

Kingdom. Tel: +44 20 7873 3000; Fax: +44 20 7407 5700. Editor: Lionel Barber.

Printed by: (Belgium) BEA Printing sprl, 16 Rue de Bosquet, Nivelles 1400; (Germany) Dogan Media

Group, Hurriyet AS Branch Germany, An der Brucke 2022, 64546 Morfelden Walldorf; (Italy) Poligrafica

Europa, S.r.l, Villasanta (MB), Via Enrico Mattei 2, Ecocity Building No.8. Milan; (South Africa) Caxton

Printers a division of CTP Limited, 16 Wright Street, Industria, Johannesburg; (Spain) Fabripress, C/ Zeus

12, Polgono Industrial MecoR2, 28880 Meco, Madrid. (Sweden) Bold Printing Group/ Boras Tidning

Tryckeri AB, Odegardsgatan 2, S504 94, Boras. (Abu Dhabi) United Printing & Publishing Company LLC,

Muroor Road, PO Box 39955, Abu Dhabi

France: Publishing Director, Adrian Clarke, 40 Rue La Boetie, 75008 Paris, Tel. +33 (0)1 5376 8250; Fax:

+33 (01) 5376 8253; Commission Paritaire N 0909 C 85347; ISSN 11482753. Germany: Responsible

Editor, Lionel Barber. Responsible for advertising content, Adrian Clarke. Italy: Owner, The Financial Times

Limited; Rappresentante e Direttore Responsabile in Italia: I.M.D.SrlMarco Provasi Via Guido da Velate 11

20162 Milano Aut.Trib. Milano n. 296 del 08/05/08 Poste Italiane SpASped. in Abb.Post.DL. 353/2003

(conv. L. 27/02/2004n.46) art. 1 comma 1, DCB Milano. Spain: Legal Deposit Number (Deposito Legal)

M325961995; Publishing Director, Lionel Barber; Publishing Company, The Financial Times Limited,

registered office as above. Local Representative office; Castellana, 66, 28046, Madrid. ISSN 11358262.

Sweden: Responsible Publisher, Bradley Johnson; Telephone +46 414 20320. UAE: Publisher, Adrian

Clarke, Tel: +33 (0)1 5376 8250; origin of publication, twofour54, Free Zone, Abu Dhabi.

Copyright The Financial Times 2012. Reproduction of the contents of this newspaper in any manner is

not permitted without the publishers prior consent. Financial Times and FT are registered trade marks

of The Financial Times Limited.

The Financial Times adheres to the selfregulation regime overseen by the UKs Press Complaints

Commission. The PCC takes complaints about the editorial content of publications under the Editors Code

of Practice (www.pcc.org.uk). The FTs own code of practice is on www.ft.com/codeofpractice.

Reprints are available of any FT article with your company logo or contact details inserted if required

(minimum order 100 copies). Phone +44 20 7873 4871. For oneoff copyright licences for reproduction

of FT articles phone +44 20 7873 4816. For both services, email syndication@ft.com

A hungry bear will not

dance, says the Greek

proverb. Twenty-four

hours after national

elections that revealed a

deeply fractured political

landscape and a society

close to psychological

exhaustion, it is an image

Greeces foreign creditors

will need to keep in mind.

Temporarily, the victory

of the centre-right New

Democracy party will

keep at bay the forces of

Syriza, the radical leftist

party determined to break

the stranglehold that it

accuses the creditors of

imposing on Greece as

their price for emergency

financial help. In this

narrow sense, the

eurozone lives to breathe

another day.

But the sickness of the

Greek economy is so far

advanced that it is

inconceivable that the

next government will

meet the economic and

fiscal targets set by other

European countries and

the International

Monetary Fund. The

Greek state is within

weeks of running out of

cash to meet its wages

and pensions bills, tax

collection has slumped

and private sector

economic activity is

grinding to a halt.

The once well-fed Greek

bear cannot dance to the

eurozone-IMF tune

because it is lying on a

stretcher in the intensive

care ward. It is hungrier

than ever for jobs, living

wages, business credit,

medical supplies and

plain hope. Turnout in

Greek elections is usually

high by European

standards but on Sunday,

despite being warned that

the nations destiny hung

in the balance, barely

60 per cent of registered

voters cast ballots.

To satisfy its creditors,

Greece is required in

coming weeks to make

public spending cuts of

up to 11.5bn and

implement the bulk of

them by the end of 2013.

But the desperate

condition of Greeces

economy and the post-

election alignment of

political forces in

parliament make it an

open question whether

the next government will

be able or willing to

honour this commitment.

Like a previous,

inconclusive election on

May 6, Sundays vote did

nothing to resolve the

paradox at the heart of

Greeces plight: the nation

wants to stay in the

eurozone but bursts with

despair and resentment at

the terms demanded of it

to do so.

The two elections have

accelerated the

disintegration of the

political order established

in Greece after the fall of

the 1967-74 military junta.

But Sundays result left

little option but to

reinstall in power the two

parties New Democracy

and the socialist Pasok

party most closely

identified with that

discredited order. It is not

a recipe either for

resolute government or

for the general publics

readiness to accept more

economic ordeals.

Greece is not the only

eurozone country whose

political structures are

buckling under the

pressure of economic

recession, unemployment

and welfare state cuts.

Irelands leftwing Sinn

Fin party exploited a

referendum on a

European fiscal treaty

last month to strengthen

its position as the main

anti-government voice, at

the expense of the Fianna

Fil party.

Silvio Berlusconis

People of Freedom party

and Umberto Bossis

Northern League are

losing their grip on

conservative voters in

Italy, and Beppe Grillos

idiosyncratic Five Star

movement is climbing in

the polls. For seven

months Italy has been

under the rule of

non-party technocrats.

Populist and xenophobic

parties flourish. Apart

from Syriza and the

hardline Communist party

on the far left, Greeces

two elections catapulted

the neo-fascist Golden

Dawn into parliament.

If there is a crumb of

comfort for the starved

Greek bear, it lies in the

erosion of the corrupt

clientelism that was the

hallmark of politics and

state administration

under Pasok and New

Democracy. Economic

collapse dictates there are

fewer jobs and favours for

politicians to distribute in

exchange for votes.

So far, however, Syriza

the bte noire of

European governments

is the only political

movement to have truly

capitalised on the

implosion of the old

order. Syriza now waits

restlessly in the wings for

its chance. Without a

revision of Greeces

financial rescue terms, it

may be only a matter of

time before Syriza moves

to centre stage.

Few crumbs of

comfort left for

starved Greek

bear after vote

It is inconceivable

that the next

government will

meet economic

and fiscal targets

GLOBAL INSIGHT

Tony Barber

in Athens

By Alex Barker in Brussels

A push by EU leaders to

create a single supervisor

for Europes largest banks

is rapidly gaining momen-

tum as support builds for

giving the European Cen-

tral Bank fresh oversight

powers in a big step

towards banking union.

The leaders of France,

Germany, Italy, Spain and

Austria are willing to back

a powerful supranational

supervisor, and a decision

to relinquish national con-

trol over cross-border banks

is being prepared for next

weeks EU summit, accord-

ing to senior officials

involved. One said the new-

found political impetus was

astonishing.

But political obstacles

remain, including the cen-

tral supervisors remit over

smaller banks and its

ability to deploy the EUs

bailout fund to inject capi-

tal directly into failing

institutions.

Currently, EU bank res-

cue loans must go through

national governments, add-

ing to their sovereign debt.

The European Commis-

sion is pressing for the

banking union to be estab-

lished for all 27 member

states a push backed by

some smaller countries out-

side the euro, whose econo-

mies are dominated by

eurozone-based banks and

who worry about handing

more power to the ECB.

We are not there yet

where every member state

supports a single supervi-

sor, said an EU official.

Diplomats say in the

short term, progress is less

likely on moves towards

common deposit insurance,

where EU or eurozone

states would share the risks

of underwriting some 5tn

of household deposits.

Angela Merkel, the Ger-

man chancellor, has made

plain her objections to

apparently simple ideas

about mutualisation.

The potential for break-

through on bank supervi-

sion and bailout rules has

been partly spurred by neg-

ative market reaction to a

proposed 100bn bailout of

Spains banks.

Because the rescue will

add senior debt to Madrids

books, the bailout loans

have spooked the Spanish

bond market, pushing up

borrowing rates to euro-era

highs again yesterday. Offi-

cials believe the Spanish

rescue highlighted flaws in

the eurozones crisis fight-

ing tools. Franois Hol-

lande, the French president,

is leading calls for the ECB

to take oversight of banks

and, when necessary, use

the new 500bn eurozone

rescue fund, the European

Stability Mechanism, to buy

direct stakes in struggling

banks.

Several ECB officials have

backed the thrust of the pro-

posal. Benot Coeur, an

ECB executive board mem-

ber, this weekend said: If

the ESM could inject capital

directly into banks, with

strong conditionality and

control, this would also

help to break the bank-

sovereign loop.

Ms Merkel has said she

is open to pan-European

supervision of Germanys

two biggest banks but has

been resisting changes in

the bailout scheme. Berlin

has long insisted that bank

rescue funds are directed

via sovereign loans, so that

national governments can

be held responsible for the

rescues conditions.

But some officials believe

giving the ECB supervision

powers, which can be

enacted under the EU trea-

ties through a unanimous

vote of member states,

would establish the pan-Eu-

ropean control structure

needed to handle bailouts.

Additional reporting by

Ralph Atkins in Frankfurt

Antonis Samaras, Greeces

centre-right leader, was try-

ing last night to stitch

together a coalition govern-

ment out of three disparate

parties united only by their

determination to keep the

country in the euro.

Mr Samaras held back-to-

back meetings with party

leaders in an effort to wrap

up a coalition agreement in

principal by today, after his

New Democracy edged the

anti-austerity leftwing Syr-

iza party into second place

in Sundays election.

Greece needs to show its

renewed commitment by

having a cabinet, and espe-

cially a finance minister, in

place before the eurogroup

[of eurozone finance minis-

ters] meets this week, said

a New Democracy official.

Sundays vote, the second

in six weeks, produced

another stand-off, although

New Democracy increased

its share of the vote by

almost 12 percentage points

and Syriza made similar

gains. The once formidable

PanHellenic Socialist Move-

ment (Pasok) finished a dis-

tant third, after more than

a third of its voter base,

mainly public sector work-

ers and pensioners,

switched to Syriza.

Final results gave New

Democracy 29.7 per cent of

the vote to 26.9 per cent for

Syriza and 12.3 per cent for

Pasok. The conservatives

won by a bigger margin

than pollsters had forecast

but, with 129 seats, were

left well short of a majority

in the 300-member parlia-

ment, even after receiving a

50-seat bonus awarded to

the winning party.

The moderate Democratic

Left, a potential third part-

ner in a conservative-led

administration, won 6.3 per

cent and 17 seats.

Mr Samarass chances of

forming a viable govern-

ment to continue imple-

menting Greeces second

174bn bailout improved

after Evangelos Venizelos,

the Pasok leader, backed

him for prime minister in a

late-night telephone call,

according to a conservative

adviser.

Two popular socialist

former ministers, Michalis

Chrysohoides and Andreas

Loverdos, then made a sur-

prise pitch for cabinet jobs

in a New Democracy-Pasok

coalition, even though their

party leader had not agreed

to a deal, the adviser said.

In theory, New Democ-

racy and Pasoks combined

162 seats would be enough

to govern without another

party, but Mr Samaras has

made clear he wants

broader backing, including

from a leftwing party,

before he starts further

unpopular fiscal and struc-

tural reforms.

Alexis Tsipras, the Syriza

leader, yesterday rejected

Mr Samarass suggestion

that he join a government

of national salvation, say-

ing his party preferred to

serve as the official parlia-

mentary opposition.

The government must be

formed by New Democracy,

since that is what the peo-

ple chose . . . and history

will judge their choice, Mr

Tsipras said. Continuing

the bailout is not going to

work, either for Europe or

Greece.

Although Syriza officials

voiced disappointment over

finishing second, they were

the only party to make sig-

nificant gains.

While support for New

Democracy and Pasok col-

lapsed from the level of

only a few years ago, Syr-

izas has seen its popularity

soar, reflecting rising popu-

lar anger with the old politi-

cal system built on patron-

age relationships and a fail-

ure to prevent Greeces eco-

nomic collapse.

The political order is

crumbling . . . there is a vac-

uum and for the time being

it tends to be filled by popu-

lists, said Loukas Tsouka-

lis, head of Athens think-

tank Eliamep. There are

people who want a radical

change, and there is no

other vehicle [than Syriza].

Some observers believe

Syriza will now become

a government-in-waiting,

watching from the sidelines

as Mr Samaras takes his

turn at trying to crack

down on tax evasion,

relaunch a stalled privatisa-

tion programme and mod-

ernise the public adminis-

tration after the failed

attempts of two previous

governments.

Despite Mr Tsiprass

pledge that his party will

serve as a responsible oppo-

sition, he may have trouble

preventing Syrizas far-left

factions, including a small

minority of old-fashioned

revolutionaries, from taking

to the streets.

Syrizas capacity for stag-

ing demonstrations that can

bring Athens to a halt has

increased as a result of the

election, thanks to having

attracted a new following

from the Stalinist Greek

communist party (KKE).

The KKE saw its vote halve

after Aleka Paparriga, its

leader, rejected Mr Tsiprass

proposal that the two par-

ties co-operate in a future

government of the left.

Mr Tsoukalis remained

doubtful that Syriza would

make a positive contribu-

tion to solving Greeces

problems. Syriza has some

healthy elements in it but

the core is former dogmatic

communists. Can you rely

on them to change the

country?

Fresh from securing an

emphatic parliamentary

majority, Franois Hollande

will shortly face a decisive

moment in his young presi-

dency when he confronts

the state of Frances public

finances.

A report due in two

weeks by the Cour des

Comptes, the national audi-

tor, is set to lay bare the

large gap that will have to

be bridged for Mr Hollande

to meet his commitment to

reduce the budget deficit to

3 per cent of gross domestic

product next year and

eliminate it in 2017.

The challenge is particu-

larly acute for Mr Hollande,

who has laid so much store

by his calls for Europe to

shift from a German-led

emphasis on austerity to

generating growth as the

way out of the eurozone

crisis.

His Socialist government,

emboldened by achieving

an outright majority in the

National Assembly, was

pushing that agenda again

yesterday. We need to

mobilise our European part-

ners because piling more

austerity on top of austerity

will lead to tragedy and a

deep rift between the peo-

ples of Europe and their

politicians, said Manuel

Valls, interior minister.

Mr Hollandes potential

difficulty is that this anti-

austerity rhetoric, a con-

tributor to his victory in

the presidential and parlia-

mentary elections, will soon

have to be reconciled with

the need to take tough

measures at home to square

the budget deficit.

With the election over,

even his allies are demand-

ing clarity. Nicolas Demo-

rand, editor of the leftist

newspaper Liberation,

wrote: The commitment to

return the public accounts

to balance, taken in front of

our European partners,

leaves little doubt over the

destination. The fog starts

with the rest: the route, the

method, the means. The

moment has come to clear

it.

Tullia Bucco, economist

at UniCredit Research, said:

It will require cuts in

expenditure and that will

be the most tricky part.

There is no place to hide.

The size of Mr Hollandes

majority should give him

the room for manoeuvre he

needs. The Socialists won

314 seats in the 577-seat

assembly, with their Green

allies taking a further 17.

The anti-austerity Left

Front slipped back to 10

seats, undermining the

Communi s t - domi nat ed

groups ability to influence

the government.

The government has indi-

cated it will have to find

extra savings of 10bn just

to meet this years deficit

target of 4.5 per cent of

GDP, because the stalled

economy has hit receipts: a

supplementary budget is

due in July. But an even

bigger task looms in fram-

ing next years budget, due

in September, with savings

of 25bn or more required

to meet the 3 per cent goal

more if growth remains

weak.

Pierre Moscovici, finance

minister, said last week

that this years deficit

shortfall would mainly be

made up by raising taxes,

with savings for next year

shared between tax

increases and spending

cuts.

Jean-Marc Ayrault, prime

minister, warned on Sunday

of the immense task

ahead. But he has also said

much of the burden will be

borne by the wealthiest

households.

Mr Hollandes pledge to

raise marginal tax to 75 per

cent on incomes above 1m

a year is set to be deployed

later this year along with

increases in wealth and

inheritance taxes, sur-

charges on banks and

energy companies and

moves to raise taxes on cap-

ital earnings to match

income tax rates.

The government is also

set to target Frances abun-

dant tax spending end-

ing tax breaks that cost the

state dearly, such as the

exemptions on social

charges and income tax on

overtime introduced by

Nicolas Sarkozy, Mr Hol-

landes predecessor.

Mr Moscovici said: I

think we can reach our

objectives without auster-

ity. But with public

expenditure accounting for

56 per cent of GDP and the

tax burden at a high level,

independent economists

believe painful cuts are

inevitable, albeit not to the

extent suffered in stricken

economies such as Greece

and Ireland.

You cannot have no aus-

terity and reduce the deficit

to 3 per cent next year

and to zero in 2017 with-

out people feeling it. It

would be better to admit

it, said Laurence Boone,

Europe economist at Bank

of America Merrill Lynch.

EU banking push gains ground

Step towards

union expected

Political impetus

astonishing

Samaras scrambles to agree coalition pact

Postelection talks

Centreright victor

is keen to appoint

ministers before

eurozone finance

ministers meet,

writes Kerin Hope

Democratic Left

KKE

Golden

Dawn

Greek result

Source: Greek interior ministry

*

Includes 50 extra seats for coming first

Seats

20

17

18

12

Syriza

71

Pasok

33

New

Democracy

129*

Independents

Antonis Samaras (left) speaks to Alexis Tsipras, Syrizas leader, at the Greek parliament. Mr Tsipras rejected the New Democracy leaders call to join a government of national salvation AP

Hollande faces decisive moment with austerity challenge

On other pages and at FT.com

Analysis, Page 9

Editorial Comment, Page 10

Gideon Rachman, Lawrence

Summers, Aristides Hatzis,

Page 11

Greece video

Election fails to resolve the

eurozones deeper problems

www.ft.com/greece

Lex video

An opportunity for the rest

of the bloc to concentrate

on its real problems

www.ft.com/lexvideo

AList

Stephen King: Greek

relief but no answers

www.ft.com/alist

EUROZONE WOES

Source: Thomson Reuters Datastream

Government expenditure

(as a % of GDP, 2012)

0 20 40 60

Denmark

France

Finland

Belgium

Sweden

Netherlands

Italy

UK

Germany

OECD total

Spain

Big spenders

Public finances

French president

will have to take

tough measures

to square budget

deficit, writes

Hugh Carnegy

Franois Hollande has been

emboldened by poll results

JUNE 19 2012 Section:World Time: 18/6/2012 - 19:19 User: jamesa Page Name: WORLD1 USA, Part,Page,Edition: EUR, 2, 1

FINANCIAL TIMES TUESDAY JUNE 19 2012

3

By Catherine Belton

in Moscow

Russia is setting aside up to

$40bn for this year and next

to shore up the economy in

case the eurozone crisis

should escalate and spread.

At the same time, Mos-

cow is dusting off a plan

that would allow the gov-

ernment to recapitalise the

banking system.

In his first interview with

a foreign newspaper since

his appointment as finance

minister last year, Anton

Siluanov said the govern-

ment had agreed to create a

reserve mechanism worth

Rbs500bn ($15.4bn) for next

year for the direct financ-

ing of anti-crisis measures.

Those would include sup-

port for socially needy peo-

ple and systemically imp-

ortant enterprises, and the

revival of a scheme pro-

posed, but not imple-

mented, in 2009 to issue

government bonds to recap-

italise banks in exchange

for shares, he said.

This year, up to Rbs800bn

earmarked for one of Rus-

sias rainy day windfall

funds the Reserve Fund, a

repository for oil revenue

could be spent on meeting

any potential shortfall for

budget obligations should

the oil price stay below the

average $117 a barrel at

which the budget breaks

even.

Separately, up to $4.4bn

in state guarantees for

loans to enterprises has

already been earmarked for

this years budget, with

$800m already disbursed a

continuation of crisis meas-

ures introduced in 2009.

We have practically pre-

pared all the necessary

measures so we can quickly

implement them in case of

a worsening of the situa-

tion, Mr Siluanov said.

The problem with the

last crisis at the beginning

of 2009 was that we spent

time getting into the swing

of it . . . Because of this we

lost a significant amount of

speed in carrying out the

measures and we lost the

chance to react quickly.

Russias main stock mar-

kets are down more than 20

per cent since highs in

March. The rouble is down

13 per cent because of fears

over the eurozone crisis and

the drop in the oil price to

about $100, stoking jitters

that a further fall would

hurt the Russian economy.

Although Russia has debt

of a mere 10 per cent of

gross domestic product and

hard currency reserves of

$500bn, it is heavily depend-

ent on oil and gas revenues.

The crisis of 2008-09 saw it

lose $200bn of its reserves

in a matter of months as it

defended a run on the rou-

ble. Even as Russia is call-

ing on European countries

to stick to austerity meas-

ures, Mr Siluanov is facing

huge pressure to loosen

budget policy at home.

In the job for just over

eight months since his pred-

ecessor Alexei Kudrin

resigned, Mr Siluanov, a

career finance ministry offi-

cial, is battling on two

fronts. Not only must he set

aside funds in case of poten-

tial crisis but spending

promises made by Vladimir

Putin in the run-up to presi-

dential election in March

could also add significantly

to outlays.

The populist pledges,

including higher wages for

teachers and doctors, could

add an additional 2 per cent

of GDP to spending in the

medium term. But Mr Silu-

anov insisted that his min-

istry would keep the budget

deficit at 1.6 per cent of

GDP for 2013 and 0.7 per

cent in 2014 already fixed

under a three-year plan

and would compensate for

the spending rises proposed

by Mr Putin by saving else-

where.

Among the budget man-

oeuvres being plotted to

keep spending in line are

the delay of certain major

spending items, while

items of lesser priority

could be cut, he said. The

delays in spending could

include the $700bn military

spending programme that

Mr Kudrin cited as posing a

risk when he resigned, Mr

Siluanov said. Increasing

taxes is the worst thing we

could do, he added.

Speaking before the G20

meeting in Mexico, Mr Silu-

anov called on the group of

wealthy nations to make

faster progress on agreeing

International Monetary

Fund voting reform to

increase the power wielded

by the Bric group of emerg-

ing nations.

We, just like the other

Bric countries [Brazil, India

and China] are interested in

making sure the question of

reforming [voting] quotas is

not forgotten, he said.

[But] we dont want to tie

the question of aid and quo-

tas . . . No one is interested

in the crisis growing in the

eurozone. We will take part

in adding to the resources

of the fund. There is no talk

of conditionality.

Moscow sets

aside $40bn to

guard against

euro contagion

By Chris Giles and

George Parker in Los Cabos

Europes leaders came

under severe pressure from

the rest of the world to act

decisively to resolve the

eurozone crisis at the start

of the Group of 20 summit,

adding to tensions before a

meeting that is unlikely to

agree clear steps to ease the

crisis.

As leaders of the most

powerful countries gathered

in Los Cabos, Mexico, some

European leaders hit back

at criticism of their

response, saying that

Europe was not the cause of

the original crisis in 2008

and was making continuous

progress in dealing with

new issues.

Jose Manuel Barroso,

European Commission pres-

ident, was in defiant mood

when questioned on the

criticism of Europe by other

G20 countries some of

which, he noted, were not

democracies: We are not

coming here to take lessons

on democracy and how to

handle our economy. We

are not complacent about

our difficulties.

Mr Barroso was respond-

ing to a chorus of voices in

Los Cabos blaming Europe

for the deteriorating global

growth outlook.

Angel Gurria, secretary

general of the Organisation

for Economic Cooperation

and Development, accused

the eurozone of not using

its existing tools to the

fullest. The fire is in

Europe right now and it is

affecting the system as a

whole. It is no longer just a

European issue, he said.

Jim Flaherty, Canadian

finance minister, continued

to rile European leaders,

insisting there would be no

support for the eurozone

until it sorted out its own

problems.

The situation is not that

were dealing with impover-

ished countries here, he

told Canadian television.

The reality is that we have

non-European G20 coun-

tries that have a lot of hesi-

tation in dedicating

resources to the wealthy

European countries.

The election results in

Greece at least offered

world leaders the opportu-

nity to urge Europe to get

to grips with the crisis.

Barack Obama, the US pres-

ident, said there was now a

positive prospect of form-

ing a stable Greek govern-

ment and making progress.

But the G20 is not

expected to do more than

urge the eurozone to

resolve the crisis. A draft of

the communiqu, leaked to

the Reuters news agency,

suggested there would be

no specific new commit-

ments made this week, only

a renewed commitment to

ensure the crisis does not

spiral out of control. The

draft communiqu states:

The euro area member

states at the G20 will take

all necessary policy meas-

ures to safeguard the integ-

rity and stability of the

euro area, including the

functioning of financial

markets and breaking the

feedback loop between sov-

ereigns and banks.

These words, although

hinting at a banking union,

are not much different from

those of the Cannes G20

communiqu last Novem-

ber, when the leaders of

economies representing

almost 90 per cent of global

income welcomed the euro-

zones determination to

bring its full resources and

entire institutional capacity

to bear in restoring confi-

dence and financial stabil-

ity, and in ensuring the

proper functioning of

money and financial mar-

kets.

The G20 meeting is seen

by non-eurozone leaders as

a chance to put pressure on

Angela Merkel, the German

chancellor, to intervene

more decisively to resolve

the single currency crisis,

but there is also an accept-

ance among diplomats that

public criticism of Ms Mer-

kel is starting to become

counter-productive.

David Cameron, the UK

prime minister, said: Its

also very difficult for Ger-

many. We have to under-

stand the German difficul-

ties. It is very difficult polit-

ically to take the steps that

are required economi-

cally . . . But nonetheless if

you want a functioning sin-

gle currency you have to

take at least some of those

steps. You need to have ele-

ments of banking union, fis-

cal transfers and so on.

Comment, Page 11

G20 adds to pressure on Europes leaders

OECD chief blames

eurozones policies

Barroso defiant

in face of criticism

No one is

interested in the

crisis growing

in the eurozone

Anton Siluanov

Finance minister

$117

Price of oil at which Russian

budget breaks even

India resists

call to cut rates

Indias central bank opted

to leave interest rates

unchanged yesterday,

withstanding pressure

from big business and

government officials in

New Delhi to give the

slowing economy a boost,

writes Rahul Jacob in

New Delhi.

The Reserve Bank of

India in its monetary

policy review meeting left

the key interest rate

unchanged at 8 per cent,

pointing to a rise in

inflation in May as a key

constraint for the

economy. The bank had

cut interest rates by 50

basis points in April.

The government

announced last week that

the wholesale prices index

rose 7.55 per cent

annually in May, up from

7.23 per cent in April, as

food and fuel prices rose

10.74 per cent and 11.53

per cent respectively last

month.

Further reduction in the

policy interest rate at this

juncture, rather than

supporting growth, could

exacerbate inflationary

pressures, the RBI wrote

in its policy review.

In full: www.ft.com/india

Summit issues: activists urge world leaders to take action on global concerns as they meet in Los Cabos yesterday AFP

G20 SUMMIT

Russian economy

JUNE 19 2012 Section:World Time: 18/6/2012 - 19:41 User: powelln Page Name: WORLD2 USA, Part,Page,Edition: EUR, 3, 1

4

FINANCIAL TIMES TUESDAY JUNE 19 2012

By Roula Khalaf in London

The Egyptian daily

newspaper al-Masr

al-Youm summed up the

countrys predicament

brilliantly yesterday.

The military transfers

power to the military,

read the headline.

While Mohamed Morsi,

the Muslim Brotherhood

presidential candidate, and

Ahmed Shafiq, the

generals favourite, battled

it out all day, each

claiming to have won

the weekend presidential

vote, the ruling military

council had already

decided who would be the

real rulers: the generals

themselves.

Not even bothering to

wait for the outcome of the

election, they issued a

constitutional declaration

on Sunday night handing

the Supreme Council of the

Armed Forces (Scaf) all

legislative authority and

empowering it to set up a

constitutional panel to

draft the new constitution.

That came after parliament

was dissolved in a

dubiously timed legal

decision on the eve of the

presidential vote and after

the generals gave

themselves sweeping new

powers to arrest civilians.

The most outrageous

part of the new declaration

is that Scaf (which will

pick the members of the

constitutional panel) will

also have the right (along

with the president and the

prime minister) to object to

the draft if it is not in

accordance with the goals

of the revolution and the

principles safeguarding the

higher interests of the

country.

Presumably, protecting

the militarys interests

including its economic and

business empire and its

lack of accountability

will be deemed in the

higher interests of the

country.

Given the widening

gap between what the

military says and what it

does, the generals might

even proclaim that

enshrining a special status

for the army in the

constitution is in keeping

with the objectives of the

revolution.

Although Scafs moves

become more blatantly

counter-revolutionary by

the day, the generals are

maintaining the pretence.

Maj-Gen Mohammed al-

Assar, a senior member

of Scaf, held a press

conference to explain the

new declaration.

According to the

government news agency,

he said the generals would

transfer power to the

president, as promised, and

the handover would be

marked by a grand

ceremony at the end of

the month.

Generals put themselves in charge

A constitutional declaration

issued by Egypts military

has made it clear the gener-

als will continue to have

the biggest say in shaping

the political order before a

winner has even been

declared in the countrys

presidential election.

Both Mohamed Morsi, a

leader of the long-repressed

Muslim Brotherhood, and

Ahmed Shafiq, a military

man and insider of the

former regime, say they

have won Egypts first ever

free presidential election.

But the ruling military

councils move yesterday,

which gave the army broad

powers over the presidency,

appeared calculated to limit

the powers of a potential

Brotherhood president if

Mr Morsi is declared

the winner and to ensure

the army avoids civilian

control under any new

arrangement.

It sets the scene for a

power struggle between the

Islamists and the military,

which has ruled the coun-

try since 1952, opening up

the possibility of fresh tur-

moil in a country battered

by 16 months of a chaotic

transition that has brought

the economy to a halt and

increased already high lev-

els of poverty.

The military council will

maintain authority over its

own budget and broad pow-

ers over the country,

including veto power over

any new presidents ability

to declare war and over any

article in a future constitu-

tion it deems counter to the

countrys interests. It has

also empowered itself to

appoint a panel to draft the

constitution.

This comes after a court

ruling last week dissolved

the Brotherhood-dominated

parliament, placing legisla-

tive powers in the hands of

the military council until a

new assembly has been

elected in six months.

The largest political force

in Egypt, the Muslim Broth-

erhood has been preparing

itself to govern for decades.

But now the organisation

appears close to achieving

its ambition, the declara-

tion deals a blow to its

plans.

The dissolution of parlia-

ment is illegal, said

Mourad Ali, a spokesman

for Mr Morsi. The new con-

stitutional declaration is

also of dubious legality. The

military council is trying to

impose a fait accompli. How

can it give itself the right to

draft the constitution con-

fiscating the right of the

people to write their own

charter? We will defend the

rights of the people, he

said.

Saad al-Katatni, the

Brotherhood speaker of the

dissolved parliament, said

legislators would meet in

the assembly today, and if

prevented by the security

services blockading the

building, they would con-

vene elsewhere.

Brotherhood MPs also

insisted that the body that

they assembled to write a

new constitution will meet

and begin work this week,

despite being subject to a

legal challenge.

Shadi Hamid, director of

research at the Brookings

Institute in Doha, said the

Brotherhood and the mili-

tary were playing a fright-

ening game of brinkman-

ship.

The constitutional decla-

ration makes for a power

grab by the military, he

said. It does not get more

blatant than this, but [a

Morsi win would mean] the

Brotherhood and the young

revolutionary groups [who

supported it] will be

emboldened by defeating

the old regime in the elec-

tion. They can confront the

military now and they have

become more equal in any

new negotiations with the

army.

He added that if Mr Morsi

became president, he would

be able to leverage his posi-

tion to rally support domes-

tically and address the

international community to

put pressure on the mili-

tary, even with the limita-

tions on his power.

As the prospect of further

political turmoil looms,

business confidence has

again dropped.

The benchmark EGX-30

index fell by 3.42 per cent

last night, sending a nega-

tive signal about market

sentiment.

Investors want a govern-

ment and a parliament and

someone to lay down eco-

nomic policy, said

Mohamed Ebeid, head of

brokerage at EFG-Hermes,

the Cairo-based regional

investment bank. If the

military will legislate, at

the end of the day their

capability will be limited.

You cant tell equity inves-

tors that we wont be fully

stable for another six

months.

Commenting on the disso-

lution of parliament,

Moodys, the credit rating

agency, said last night that

heightened political uncer-

tainty will likely prove a

setback to the economy,

which was just regaining

domestic and foreign credi-

tor confidence.

It noted that foreign sup-

port for the Egyptian econ-

omy remained uncertain

because a much-needed

loan from the International

Monetary Fund was condi-

tional on the stabilisation of

domestic politics and the

formulation of an economic

reform plan.

Indepth

www.ft.com/egypt

Egypt risks turmoil as military tightens grip

Election aftermath

Move giving army

wide powers seems

calculated to curb a

potential Islamist

president, writes

Heba Saleh

Mohamed Morsi supporters in Cairo yesterday. The Muslim Brotherhood candidate and his opponent have both claimed victory in the presidential poll Reuters

WORLD NEWS

THE WORLD BLOG

For more posts from our

international affairs blog

www.ft.com/theworld

World blog

You cant tell

equity investors we

wont be stable for

another six months

Mohamed Ebeid

EFGHermes

JUNE 19 2012 Section:World Time: 18/6/2012 - 19:50 User: jonesl Page Name: WORLD3 USA, Part,Page,Edition: USA, 4, 1

6

FINANCIAL TIMES TUESDAY JUNE 19 2012

WORLD NEWS

By Abeer Allam

King Abdullah of Saudi

Arabia has appointed his

half-brother, Prince Salman,

76, as the heir apparent.

The announcement yes-

terday followed the death of

Crown Prince Naif on Sat-

urday, the Saudi press

agency reported, citing a

royal decree.

The appointment of

Prince Salman, one of the

most influential senior

members of the al-Saud

family, surprised few Saudi

observers. He becomes the

third crown prince since

King Abdullah ascended the

throne in 2005 and the sec-

ond in eight months, high-

lighting concern over the

line of succession in the

worlds biggest oil exporter.

Prince Salman was

appointed defence minister

in 2011 after the death of

Sultan bin Abdelaziz, the

former crown prince and

defence minister. Along

with Prince Naif, the power-

ful interior minister who

died in Geneva and was

buried in Mecca on Sunday,

Prince Salman is one of the

so-called Sudairi seven,

seven full brothers born of

the kingdoms founder,

Abdelaziz al-Saud, and his

wife Hussa al-Sudairi. They

formed a strong bloc within

the royal family, controlling

key ministerial posts.

Despite promoting him in

November, King Abdullah

had not appointed Prince

Salman as second deputy

prime minister, a post tradi-

tionally reserved for the

third in line. Some observ-

ers suggested that this sig-

nalled underlying tensions.

As governor of Riyadh

province since 1965, Prince

Salman oversaw the capi-

tals dramatic transforma-

tion from a mud-brick

desert town into a sprawl-

ing city with modern infra-

structure, manicured land-

scapes and high-rise towers.

Diplomats describe Prince

Salman as diligent and well

respected within Saudi Ara-

bia and hope his appoint-

ment will allow for a period

of stability at the highest

levels of Saudi decision

making.

They noted that Prince

Salman has had health con-

cerns but he can travel and

fulfil his duties and has a

conciliatory and diplomatic

nature. The prince enjoys

close ties with the religious

establishment and with

intellectuals and journal-

ists.

He is also well regarded

as father of Prince Sultan

bin Salman, who accompa-

nied a US space shuttle mis-

sion and now heads the

Saudi tourism and antiqui-

ties commission.

Prince Salman is also

regarded as potentially less

hostile to reform than his

brother, who had publicly

expressed reservations

about changes rights for

women. However, Prince

Salman is known as a

staunch supporter of the

Saudi interpretation of

Islam, Wahhabism. Many

Saudis regard Riyadh as

being unusually conserva-

tive compared with the cit-

ies of the eastern and west-

ern provinces.

King Abdullah also

appointed Prince Salmans

younger brother, Prince

Ahmed, to the position of

interior minister.

Salman named as Saudi

Arabias heir apparent

By Charles Clover in Moscow

and Abigail FieldingSmith

in Beirut

Russia has announced it is

preparing two warships to

sail to Syria to protect Rus-

sian citizens, in a sign that

it is taking precautions

against a worsening of secu-

rity there.

A spokesman for the

Black Sea fleet told Russias

Interfax news agency the

mission would be under-

taken in case of necessity.

His comments appeared

designed to clarify specula-

tion that warships had

already set sail for Syria.

Interfax had quoted an

anonymous official as say-

ing that was the case ear-

lier yesterday.

One of the warships, the

spokesman said, carries a

150-strong contingent of

marines, in addition to 25

tanks, but he did not give

details of the other ship.

Russia is taking the pre-

cautions as fresh fighting

across Syria killed 50 people

yesterday. Activists said

government forces were

continuing to pound opposi-

tion strongholds in various

parts of the country.

We are under siege,

said one activist in Homs,

who said some districts had

been cut off for 10 days by

intense bombardment. We

have not enough medical

equipment and medical

crew. Most are volunteers,

the activist said. We have

a lot of wounded people and

we dont know what to do

with them.

Heavy violence was also

reported in Damascus prov-

ince. According to the Syr-

ian Observatory for Human

Rights, an opposition-

affiliated monitoring group

based in the UK, the regime

launched mortars on the

Damascus suburb of Douma

yesterday, where rebels

have been clashing with

government forces.

At least 56 people were

killed throughout the coun-

try in yesterdays violence,

the Observatory said,

including 19 soldiers or

members of the security

forces.

Russias security relation-

ship with Syria has come

under scrutiny as Damas-

cus becomes ever more

dependent on Moscow fol-

lowing EU and US sanc-

tions. The port of Tartous

in Syria is a key Russian

naval base, which experts

estimate has about 50 Rus-

sian staff working there.

Meanwhile, Russian tech-

nicians continue to work in

Syria under contract to

maintain Russian arms pur-

chased by the regime.

Sergei Lavrov, Russias

foreign minister, has denied

that Russia is selling arms

to Syria that can be used

against civilians. Russia

says it is not violating any

UN sanctions or treaty obli-

gations in doing so. Last

year, Russia sold anti-

aircraft missiles to Syria, as

well as missile batteries

designed to fend off sea-

borne attacks. It also signed

a contract to supply 36 Yak-

130 trainer aircraft for

$550m. Recently it signed a

contract to supply 24

MiG-29 advanced fighter

bombers.

Russia has admitted it is

repairing a number of heli-

copter gunships for the Syr-

ian army that were origi-

nally sold in Soviet times.

According to news reports,

those helicopters are en

route to Syria from the Rus-

sian port of Kaliningrad,

though Russias defence

minister declined to com-

ment on the story yester-

day.

In addition, on May 26 a

Russian cargo ship called

the Professor Katsman

docked in Tartous harbour

in the face of allegations by

human rights agencies that

it was carrying a cargo of

arms for Syria.

Indepth, www.ft.com/syria

Russian

warships

made ready

for Syria

Move to protect

naval base and staff

Clashes kill 50

across country

Opposition fighters train near Homs, which was reported to be under siege yesterday Reuters

By Charles Clover

in Moscow, James Blitz

in London and Najmeh

Bozorgmehr in Tehran

Iran engaged in intense

and tough exchanges with

the US and other world

powers the 5+1 group as

a third round of negotia-

tions began yesterday amid

fears a peaceful resolution

to the stand-off over

Tehrans nuclear ambitions

will prove elusive.

Iran will meet senior dip-

lomats from the EU and six

world powers again today

to see if confidence-building

measures can be agreed to

avert a conflict over the

Iranian nuclear programme.

But last night the mood

among diplomats was

downbeat, after signs both

parties were unprepared to

make compromises on the

first day of two-day talks.

We had an intense and

tough exchange of views,

said Michael Mann, spokes-

man for EU policy chief

Lady Ashton, co-ordinating

the negotiations with Iran.

Mr Mann said discussions

were more substantive than

last month in Baghdad, add-

ing: Iran engaged in detail

on our proposal but not in a

way wed like them to.

His pessimism was ech-

oed by Sergei Ryabkov,

Russias deputy foreign

minister, who said after the

talks last night that he

hoped there would be a new

round, implying he did not

envisage a breakthrough.

Mr Ryabkov said the

main stumbling block had

been the complexity and

incompatibility of the

delegations positions. An

Iranian delegate added to

the grim mood, saying that

the talks do not have the

most positive atmosphere

and that the second day of

talks are likely to be the

most significant.

Saeed Jaleeli, the Iranian

chief negotiator, was due to

attend a dinner last night

with Nikolai Patrushev,

chairman of Russias

National Security Council

and a close confidant of

Vladimir Putin, president.

That prompted specula-

tion Mr Patrushev would

put fresh pressure on Mr

Jaleeli to accept a deal

before the negotiations

wind up today.

As diplomats met, a

report on Iranian TV said

Iran would not consider

curtailing the enrichment

of uranium to 20 per cent

a goal for international

mediators unless the six

powers acknowledged it had

the right to enrich uranium

and lifted sanctions.

Ayatollah Ali Khamenei,

Irans supreme leader, gave

a tacit warning to western

powers at the talks, declar-

ing in dealing with the Ira-

nian nation, stubbornness,

arrogance, self-conceit and

irrelevant expectations . . .

will go nowhere.

An EU diplomat said Iran

responded to our package

of proposals from Baghdad

but, in doing so, brought up

lots of questions and well-

known positions, including

past grievances. We agreed

to reflect overnight on each

others positions.

See Markets

Envoys downbeat

after Irans tough

nuclear stance

We have a lot of

wounded and we

dont know what

to do with them

Homs resident

JUNE 19 2012 Section:World Time: 18/6/2012 - 19:35 User: wayn Page Name: WORLD4 USA, Part,Page,Edition: USA, 6, 1

FINANCIAL TIMES TUESDAY JUNE 19 2012

7

Canada is worried about an

unconditional declaration

that access to safe drinking

water is a human right. The

Holy See is against using

family planning to advance

gender equality. And doz-

ens of countries are wary

about getting rid of fossil

fuel subsidies.

These are just some of the

objections negotiators have

raised ahead of this weeks

Rio+20 sustainable develop-

ment conference, which the

UN says is the biggest event

it has organised.

They underline the grow-

ing doubts many have

about what the 100-plus

leaders expected to fly in

for the meeting will

achieve by the time it ends

on Friday. Its like a rally

race of back seat drivers,

said Lasse Gustavsson,

head of the World Wildlife

Fund International delega-

tion. Everyone is sitting in

the back seat and no one is

taking responsibility.

The summit gets its name

from being held 20 years

after the 1992 Rio earth

summit that launched a

number of landmark trea-

ties, including ones to limit

the extinction of species

and climate change.

But progress has been so

slow that only four of the

worlds 90 most important

green goals and objectives

have seen significant

progress, a UN Environ-

ment Programme report

said this month, and there

has been little or no

improvement on goals to

address 24 problems includ-

ing decimated fish stocks,

climate change and deterio-

rating coral reefs.

Yet despite months of

negotiations leading up to

the summit, officials have

struggled even to finalise

the wording of a far less

ambitious final text docu-

ment on the eve of the for-

mal conference opening

tomorrow.

At other global green

summits, the US might

have been blamed. But this

year, Canada is under fire

for what environmental

campaigners like to call a

blocking mentality.

A commitment recognis-

ing the human right to safe

drinking water has sur-

vived to the latest draft

text, but only with the

added condition that it does

not relate to transbound-

ary water issues.

Water-rich Canada

insisted on this, say people

close to the negotiations,

adding it appeared Ottawa

was concerned about poten-

tial legal problems sur-

rounding any effort to

export water abroad.

Canadas environment

ministry told the Financial

Times that Canada sup-

ported the human right of

everyone to safe drinking

water. But it added: We

recognise that the right to

safe drinking water and

basic sanitation does not

encompass transboundary

water issues including bulk

water trade, nor any man-

datory allocation of interna-

tional development assist-

ance.

The Vaticans efforts to

influence negotiations at a

summit trying to address

the effect of forecast popu-

lation increases on pressed

natural resources and pov-

erty has also proved conten-

tious in some quarters.

I am baffled that the

Holy See is taken seriously

and allowed real influence

in this field, said Roger

Martin, a former British

diplomat who chairs the

Population Matters cam-

paign group. That a body

representing a group of old,

celibate men should set

themselves up as a

world authority on all mat-

ters sexual is surely ludi-

crous.

One of the most hotly

contested sections of the

summit text has been the

paragraph on phasing out

environmentally harmful

fossil fuels a move the G20

backed three years ago that

has proved difficult to

implement.

The latest draft Rio text

says the summit should

recognise the need for fur-

ther action on such subsi-

dies, taking fully into

account the specific condi-

tions and different levels of

development of individual

countries, but adds: Note:

placement of paragraph still

to be determined.

The EU, one of the pushi-

est advocates at global

green summits, has mean-

while been distracted by the

Greek elections impact on

the eurozone crisis, prompt-

ing something of a parlour

game about which of its

leaders will make it to

Rio+20.

Franois Hollande, the

newly elected French presi-

dent, is expected, as are the