S-ar putea să vă placă și

- Nassim Taleb Anti-Fragile Portfolio ResearchDocument24 paginiNassim Taleb Anti-Fragile Portfolio Researchplato363Încă nu există evaluări

- Csec Mathematics January 2018 p2 PDFDocument33 paginiCsec Mathematics January 2018 p2 PDFglennÎncă nu există evaluări

- CSS Analytics Minimum Correlation AlgorithmDocument91 paginiCSS Analytics Minimum Correlation Algorithmcssanalytics100% (1)

- Strategic Risk TakingDocument18 paginiStrategic Risk TakingvikbitÎncă nu există evaluări

- The Thorny Way of Truth Part7 MarinovDocument340 paginiThe Thorny Way of Truth Part7 MarinovEvaldas StankeviciusÎncă nu există evaluări

- Ishares Portfolio Analytics Coskew and CoKurt VBA3Document178 paginiIshares Portfolio Analytics Coskew and CoKurt VBA3Peter Urbani100% (1)

- Howard Marks Letters: Risk Revisited AgainDocument21 paginiHoward Marks Letters: Risk Revisited AgainKyithÎncă nu există evaluări

- Strategic Risk TakingDocument9 paginiStrategic Risk TakingDipock MondalÎncă nu există evaluări

- Cerm M1 1521 PDFDocument26 paginiCerm M1 1521 PDFMohiuddin69100% (1)

- Why Distributions Matter (16 Jan 2012)Document43 paginiWhy Distributions Matter (16 Jan 2012)Peter UrbaniÎncă nu există evaluări

- Market Risk Questions PDFDocument16 paginiMarket Risk Questions PDFbabubhagoud1983Încă nu există evaluări

- Algebra Test SolutionsDocument4 paginiAlgebra Test SolutionsJennifer Jai Eun HuhÎncă nu există evaluări

- Singular Spectrum Analysis Demo With VBADocument12 paginiSingular Spectrum Analysis Demo With VBAPeter UrbaniÎncă nu există evaluări

- Intra-Horizon VaR and Expected Shortfall Spreadsheet With VBADocument7 paginiIntra-Horizon VaR and Expected Shortfall Spreadsheet With VBAPeter Urbani0% (1)

- Nassim Nicholas Taleb Managing Risk A Probability ModelDocument4 paginiNassim Nicholas Taleb Managing Risk A Probability ModelA Roy100% (3)

- Probable Maximum LossDocument4 paginiProbable Maximum LossDiana MitroiÎncă nu există evaluări

- CPM PertDocument21 paginiCPM Pertkabina goleÎncă nu există evaluări

- Capital Asset Pricing Model: Make smart investment decisions to build a strong portfolioDe la EverandCapital Asset Pricing Model: Make smart investment decisions to build a strong portfolioEvaluare: 4.5 din 5 stele4.5/5 (3)

- 2006 Trial General Mathematics Year 12 Paper PDFDocument20 pagini2006 Trial General Mathematics Year 12 Paper PDFYon Seo YooÎncă nu există evaluări

- Kelloway, E. Kevin Using Mplus For Structural Equation Modeling A Researchers GuideDocument250 paginiKelloway, E. Kevin Using Mplus For Structural Equation Modeling A Researchers Guideintemperante100% (4)

- The Myth of Diversification S PageDocument2 paginiThe Myth of Diversification S PageGuido 125 LavespaÎncă nu există evaluări

- Quantitative Risk Management: A Practical Guide to Financial RiskDe la EverandQuantitative Risk Management: A Practical Guide to Financial RiskÎncă nu există evaluări

- P1.T1. Foundations of Risk Chapter 1. The Building Blocks of Risk Management Bionic Turtle FRM Study NotesDocument21 paginiP1.T1. Foundations of Risk Chapter 1. The Building Blocks of Risk Management Bionic Turtle FRM Study NotesChristian Rey MagtibayÎncă nu există evaluări

- T1-FRM-1-Ch1-Risk-Mgmt-v3.3 - Study NotesDocument21 paginiT1-FRM-1-Ch1-Risk-Mgmt-v3.3 - Study NotescristianoÎncă nu există evaluări

- Introduction To VaRDocument21 paginiIntroduction To VaRRanit BanerjeeÎncă nu există evaluări

- Risk Risk Concerns The Deviation of One or More Results of One or More Future Events From Their Expected Value. Technically, The Value ofDocument12 paginiRisk Risk Concerns The Deviation of One or More Results of One or More Future Events From Their Expected Value. Technically, The Value ofBangi Sunil KumarÎncă nu există evaluări

- Convexity Maven - A Guide For The PerplexedDocument11 paginiConvexity Maven - A Guide For The Perplexedbuckybad2Încă nu există evaluări

- 4 Risk ReturnDocument14 pagini4 Risk ReturnUtkarsh BhalodeÎncă nu există evaluări

- Chapter #2 (Part 1)Document17 paginiChapter #2 (Part 1)Consiko leeÎncă nu există evaluări

- Notite Part IIDocument4 paginiNotite Part IIAndrada TanaseÎncă nu există evaluări

- Risk ManagementDocument7 paginiRisk Managementbharti guptaÎncă nu există evaluări

- VisualisingDocument4 paginiVisualisingOssiamoroÎncă nu există evaluări

- Market Risk Measurement & Management PDFDocument19 paginiMarket Risk Measurement & Management PDFramsiva354Încă nu există evaluări

- Lesson 1: Basic Concepts of Risk Management: Week 1Document73 paginiLesson 1: Basic Concepts of Risk Management: Week 1Anna DerÎncă nu există evaluări

- FIN 440 Risk & Return Chapter Reference - CHP 6Document4 paginiFIN 440 Risk & Return Chapter Reference - CHP 6Syed Ataur RahmanÎncă nu există evaluări

- FIN 440 Risk & Return Chapter Reference - CHP 6Document4 paginiFIN 440 Risk & Return Chapter Reference - CHP 6Syed Ataur RahmanÎncă nu există evaluări

- Dealing With Dependent Risks: Claudia KL Uppelberg Robert StelzerDocument32 paginiDealing With Dependent Risks: Claudia KL Uppelberg Robert Stelzernikhilesh kumarÎncă nu există evaluări

- Risk Management G InsuranceDocument160 paginiRisk Management G InsurancePrasanta Ghosh100% (1)

- UntitledDocument42 paginiUntitledVivaan KothariÎncă nu există evaluări

- Dealing With UncertaintyDocument22 paginiDealing With UncertaintyMarielle CambaÎncă nu există evaluări

- Kaplan 1981 OnTheQuantitativeDefinitionofRiskDocument18 paginiKaplan 1981 OnTheQuantitativeDefinitionofRiskjen610iÎncă nu există evaluări

- Risk Management Models - What To Use, and Not To Use: Peter Luk - April 2008Document14 paginiRisk Management Models - What To Use, and Not To Use: Peter Luk - April 2008donttellyouÎncă nu există evaluări

- Risk+Return NTDocument43 paginiRisk+Return NTRana HaiderÎncă nu există evaluări

- RateLab VAR ZHDocument7 paginiRateLab VAR ZHZerohedgeÎncă nu există evaluări

- Study Notes The Building Blocks of Risk ManagementDocument19 paginiStudy Notes The Building Blocks of Risk Managementalok kundaliaÎncă nu există evaluări

- The Trouble With Risk MatricesDocument27 paginiThe Trouble With Risk MatricesJacekÎncă nu există evaluări

- Analysis of Risk and Return: TopicDocument9 paginiAnalysis of Risk and Return: TopicSatyam JaiswalÎncă nu există evaluări

- Risk &insuranceDocument138 paginiRisk &insurancesabit hussenÎncă nu există evaluări

- Madsen PedersenDocument23 paginiMadsen PedersenWong XianyangÎncă nu există evaluări

- LESSON 3 Business Ethics and Risk ManagementDocument4 paginiLESSON 3 Business Ethics and Risk ManagementEvelyn DamianÎncă nu există evaluări

- What Can Lead The Lead The Next Market CorrectionDocument4 paginiWhat Can Lead The Lead The Next Market Correctionmanindrag00Încă nu există evaluări

- The Comparative Risk and Performance Analysis of Hungarian and Romanian Exchange IndicesDocument12 paginiThe Comparative Risk and Performance Analysis of Hungarian and Romanian Exchange IndicesAnonymous 4gOYyVfdfÎncă nu există evaluări

- CHAPTER 5 - Portfolio TheoryDocument58 paginiCHAPTER 5 - Portfolio TheoryKabutu ChuungaÎncă nu există evaluări

- Risk MatrixDocument3 paginiRisk MatrixSagar KulkarniÎncă nu există evaluări

- Lecture2 2010 CourseworksDocument41 paginiLecture2 2010 CourseworksJack Hyunsoo KimÎncă nu există evaluări

- What Is Risk Management?: U.S. Treasury Derivatives Options FuturesDocument5 paginiWhat Is Risk Management?: U.S. Treasury Derivatives Options FuturesabcdÎncă nu există evaluări

- Capital Market TheoryDocument14 paginiCapital Market TheorySaiyan VegetaÎncă nu există evaluări

- Risk and Other Dark Matters - by Marc M GrozDocument4 paginiRisk and Other Dark Matters - by Marc M Grozmarcgroz100% (2)

- SvarDocument4 paginiSvarGrupo CobercolÎncă nu există evaluări

- Taleb TestimonyDocument10 paginiTaleb TestimonyArmando MartinsÎncă nu există evaluări

- Report Res558 (PM, Sem2) PDFDocument10 paginiReport Res558 (PM, Sem2) PDFItsme MariaÎncă nu există evaluări

- Exley Mehta SmithDocument32 paginiExley Mehta SmithRohit GuptaÎncă nu există evaluări

- Visualising Your Risks Making Sense of Risks by LeDocument5 paginiVisualising Your Risks Making Sense of Risks by LeVictor VargasÎncă nu există evaluări

- LC Risk MGT CH 1Document7 paginiLC Risk MGT CH 1newaybeyene5Încă nu există evaluări

- Taleb - Against VaRDocument4 paginiTaleb - Against VaRShyamal VermaÎncă nu există evaluări

- Four Letter Word: by Rod FarrarDocument51 paginiFour Letter Word: by Rod FarrarMohd Zubaidi Bin OthmanÎncă nu există evaluări

- Unit 5 - 1 - Paper - CAPMDocument21 paginiUnit 5 - 1 - Paper - CAPMMaiNguyenÎncă nu există evaluări

- Acertasc PDFDocument9 paginiAcertasc PDFPablo SalcedoÎncă nu există evaluări

- Do You Have To Be Abnormal To Beat The MarketDocument3 paginiDo You Have To Be Abnormal To Beat The MarketPeter UrbaniÎncă nu există evaluări

- Random Forest in Excel and VBADocument24 paginiRandom Forest in Excel and VBAPeter UrbaniÎncă nu există evaluări

- Cholesky Versus SVDDocument4 paginiCholesky Versus SVDPeter UrbaniÎncă nu există evaluări

- Partial Correlation Network Graph VBA (DJINDI)Document463 paginiPartial Correlation Network Graph VBA (DJINDI)Peter UrbaniÎncă nu există evaluări

- Opalesque New Managers March 2012Document37 paginiOpalesque New Managers March 2012Peter UrbaniÎncă nu există evaluări

- Opalesque NewManagers July 2012Document45 paginiOpalesque NewManagers July 2012Peter UrbaniÎncă nu există evaluări

- Opalesque New Managers May 2012Document51 paginiOpalesque New Managers May 2012Peter Urbani0% (1)

- How Well Does Your Hedge Fund HedgeDocument2 paginiHow Well Does Your Hedge Fund HedgePeter UrbaniÎncă nu există evaluări

- Opalesque New Managers May 2012Document51 paginiOpalesque New Managers May 2012Peter Urbani0% (1)

- TLS Orthogonal Regression VBADocument16 paginiTLS Orthogonal Regression VBAPeter Urbani0% (1)

- Incremental and Marginal VaR Plus Infiniti 4 Moment Version No VBADocument14 paginiIncremental and Marginal VaR Plus Infiniti 4 Moment Version No VBAPeter UrbaniÎncă nu există evaluări

- Four Moment Risk Decomposition No VBADocument13 paginiFour Moment Risk Decomposition No VBAPeter UrbaniÎncă nu există evaluări

- Infiniti Capital Four Moment Risk DecompositionDocument19 paginiInfiniti Capital Four Moment Risk DecompositionPeter UrbaniÎncă nu există evaluări

- Liqudity VaR With Correct Time Scaling of Higher MomentsDocument113 paginiLiqudity VaR With Correct Time Scaling of Higher MomentsPeter UrbaniÎncă nu există evaluări

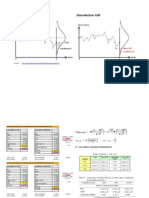

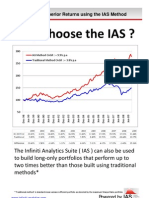

- Why Choose The IASDocument6 paginiWhy Choose The IASPeter UrbaniÎncă nu există evaluări

- C++-Institute Certkiller CPA v2017-09-20 by Mark 105qDocument96 paginiC++-Institute Certkiller CPA v2017-09-20 by Mark 105qعبدالله أبوشاويشÎncă nu există evaluări

- Prediction of Airline Ticket Price: Motivation Models DiagnosticsDocument1 paginăPrediction of Airline Ticket Price: Motivation Models DiagnosticsQa SimÎncă nu există evaluări

- Array PseudocodeDocument6 paginiArray PseudocodeMehabunnisaaÎncă nu există evaluări

- Workshop 5 2D Axisymmetric Impact: Introduction To ANSYS Explicit STRDocument20 paginiWorkshop 5 2D Axisymmetric Impact: Introduction To ANSYS Explicit STRCosmin ConduracheÎncă nu există evaluări

- A. Permutation of N Different Objects, Taken All or Some of ThemDocument8 paginiA. Permutation of N Different Objects, Taken All or Some of ThemChristina Corazon GoÎncă nu există evaluări

- Phil 26 Perpetual Motion MachinesDocument21 paginiPhil 26 Perpetual Motion MachinesMos CraciunÎncă nu există evaluări

- Pipeline ProjectDocument7 paginiPipeline Projectapi-317217482Încă nu există evaluări

- Alexander Graham - Kronecker Products and Matrix Calculus With ApplicationsDocument129 paginiAlexander Graham - Kronecker Products and Matrix Calculus With ApplicationsErik ZamoraÎncă nu există evaluări

- NMF 8.3 - Pupil BookDocument256 paginiNMF 8.3 - Pupil BookKhaled DaoudÎncă nu există evaluări

- Presentation of DataDocument18 paginiPresentation of DataMohit AlamÎncă nu există evaluări

- Allowable Spandepth Ratio For High Strength Concrete BeamsDocument10 paginiAllowable Spandepth Ratio For High Strength Concrete BeamsyunuswsaÎncă nu există evaluări

- Math Dynamic TireDocument19 paginiMath Dynamic TiresiritapeÎncă nu există evaluări

- B.Tech Physics Course NIT Jalandhar Electrostatics Lecture 4Document30 paginiB.Tech Physics Course NIT Jalandhar Electrostatics Lecture 4Jaspreet Singh SidhuÎncă nu există evaluări

- Qualitative Data Analysis A Compendium of Techniques and A PDFDocument24 paginiQualitative Data Analysis A Compendium of Techniques and A PDFMARIAÎncă nu există evaluări

- Force and MotionDocument7 paginiForce and MotionAIFAA NADHIRAH BINTI AMIR WARDIÎncă nu există evaluări

- Research Paper - 1Document18 paginiResearch Paper - 1Sunanda VinodÎncă nu există evaluări

- 2016 DR Gks Scholarship Application FormDocument25 pagini2016 DR Gks Scholarship Application FormChhaylySrengÎncă nu există evaluări

- Qdoc - Tips - Solution Manual Kinematics and Dynamics of MachineDocument9 paginiQdoc - Tips - Solution Manual Kinematics and Dynamics of MachineLi Yi MoÎncă nu există evaluări

- Aberrations of TelescopeDocument14 paginiAberrations of Telescopelighttec21Încă nu există evaluări

- K Air Conditioning M1Document82 paginiK Air Conditioning M1bhalchandrapatilÎncă nu există evaluări

- Thermodynamics NotesDocument41 paginiThermodynamics NotesAbel NetoÎncă nu există evaluări

- The Cresent High School Dina .: Total Marks: 60 Marks Obt: - Physics S.S.C Part IDocument2 paginiThe Cresent High School Dina .: Total Marks: 60 Marks Obt: - Physics S.S.C Part ICh M Sami JuttÎncă nu există evaluări

- Basics of Electrical MeasurementDocument98 paginiBasics of Electrical MeasurementAshesh B VigneshÎncă nu există evaluări

- Inference and Errors in Surveys - GrovesDocument17 paginiInference and Errors in Surveys - GrovesChinda EleonuÎncă nu există evaluări