S-ar putea să vă placă și

- 1040 Exam Prep Module IV: Items Excluded from Gross IncomeDe la Everand1040 Exam Prep Module IV: Items Excluded from Gross IncomeÎncă nu există evaluări

- Revenue AdministrationDocument3 paginiRevenue AdministrationMontasir BalambagÎncă nu există evaluări

- III. Chapter 5 - School FundingDocument14 paginiIII. Chapter 5 - School FundingJennelyn PaduaÎncă nu există evaluări

- CIR v. DLSUDocument3 paginiCIR v. DLSUCarlyle Esquivias ChuaÎncă nu există evaluări

- Laws On Private SchoolDocument34 paginiLaws On Private Schoolslide_posh100% (1)

- CIR V DLSU 2009 DigestDocument5 paginiCIR V DLSU 2009 DigestCelina Marie Panaligan100% (1)

- Jesus Sacred Heart College vs. CirDocument2 paginiJesus Sacred Heart College vs. CirMC Quesada100% (2)

- Educational InstitutionsDocument7 paginiEducational InstitutionsmjpjoreÎncă nu există evaluări

- EDUC610Document6 paginiEDUC610SANTA ISABEL MERCADOÎncă nu există evaluări

- Financial Management in Education Institutions: Rosalie J. MacalosDocument32 paginiFinancial Management in Education Institutions: Rosalie J. MacalosJerome MonferoÎncă nu există evaluări

- Budget and Fund For Education Chapter 4Document21 paginiBudget and Fund For Education Chapter 4Patrick anthony ValesÎncă nu există evaluări

- Facts:: Lung Center of Philippines V. Quezon City, GR No. 144104, 2004-06-29Document8 paginiFacts:: Lung Center of Philippines V. Quezon City, GR No. 144104, 2004-06-29Ralph Ryan TooÎncă nu există evaluări

- Commissioner of Internal Revenue (Cir) V. de La Salle University, Inc. (DLSU)Document3 paginiCommissioner of Internal Revenue (Cir) V. de La Salle University, Inc. (DLSU)Violet Parker100% (1)

- Case StudyDocument13 paginiCase StudyPaula ConstantinoÎncă nu există evaluări

- RA 6655. Free Public Secondary Education Act. 1988Document2 paginiRA 6655. Free Public Secondary Education Act. 1988Jemaica TumulakÎncă nu există evaluări

- Written Report Consti 2Document11 paginiWritten Report Consti 2jamesleeMÎncă nu există evaluări

- Module 6 Teaching Prof First Sem 2021-22Document32 paginiModule 6 Teaching Prof First Sem 2021-22Maria ElizaÎncă nu există evaluări

- Ra 8545Document6 paginiRa 8545KFÎncă nu există evaluări

- Module 6 Teaching Prof First Sem 2021-22Document32 paginiModule 6 Teaching Prof First Sem 2021-22Manilyn FernandezÎncă nu există evaluări

- Ra 8545 FVRDocument12 paginiRa 8545 FVRKristine Salvador CayetanoÎncă nu există evaluări

- An Act Providing Goverment Assistance For Private SchoolDocument8 paginiAn Act Providing Goverment Assistance For Private SchoolELLEN B.SINAHONÎncă nu există evaluări

- Supreme CourtDocument10 paginiSupreme CourtJacqueline PaulinoÎncă nu există evaluări

- No. 8545Document10 paginiNo. 8545Girlie Harical GangawanÎncă nu există evaluări

- RA 6728-Government Assistance To Students and Teachers in Private Education ActDocument11 paginiRA 6728-Government Assistance To Students and Teachers in Private Education ActRosa GamaroÎncă nu există evaluări

- Tax CasesDocument11 paginiTax CasesJesse AlindoganÎncă nu există evaluări

- Free Education ActDocument3 paginiFree Education ActmaloudelaÎncă nu există evaluări

- Commission On Audit Cebu V Province of CebuDocument2 paginiCommission On Audit Cebu V Province of CebuIhna Alyssa Marie Santos100% (1)

- School Finance Module 2 - Winnie Claire EscobarDocument28 paginiSchool Finance Module 2 - Winnie Claire EscobarRaian DuranÎncă nu există evaluări

- Ra 6728Document36 paginiRa 6728VIA BAWINGANÎncă nu există evaluări

- G.R. No. 196596Document10 paginiG.R. No. 196596zelayneÎncă nu există evaluări

- Hand Out. RA 6655Document3 paginiHand Out. RA 6655Shema SheravieÎncă nu există evaluări

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument2 paginiBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledNikki MadriagaÎncă nu există evaluări

- Chapter 8 Financing Education As An Administrative FunctionDocument42 paginiChapter 8 Financing Education As An Administrative FunctionJeza Lyn Gibaga100% (1)

- Tax DigestDocument7 paginiTax DigestPhilip UlepÎncă nu există evaluări

- 20 CIR V Dlsu DigestDocument5 pagini20 CIR V Dlsu DigestARCHIE AJIASÎncă nu există evaluări

- GVC Finance EspinoDocument28 paginiGVC Finance EspinoVida Bianca Mercader - LausÎncă nu există evaluări

- Chapter-3 2 1Document23 paginiChapter-3 2 1Joyce Ann RamirezÎncă nu există evaluări

- Cir V. Dlsu: Tax RemediesDocument18 paginiCir V. Dlsu: Tax Remediesesmeralda de guzmanÎncă nu există evaluări

- Module 6 Teaching Prof First Sem 2021-22Document33 paginiModule 6 Teaching Prof First Sem 2021-22RoseÎncă nu există evaluări

- 1 Fundamental Principles of Taxation PART 3Document4 pagini1 Fundamental Principles of Taxation PART 3hunter kimÎncă nu există evaluări

- RR No. 3-2022Document4 paginiRR No. 3-2022try saguilotÎncă nu există evaluări

- Section 28 (3) Article VIDocument2 paginiSection 28 (3) Article VIMarzan MaraÎncă nu există evaluări

- Republic Act No. 6655Document22 paginiRepublic Act No. 6655Ma Carmel JaqueÎncă nu există evaluări

- PC 2Document3 paginiPC 2pepe.oblack13Încă nu există evaluări

- Republic Act No 6655Document28 paginiRepublic Act No 6655ashiyatokugawaÎncă nu există evaluări

- Tuition Fee SupplementsDocument2 paginiTuition Fee SupplementsMJ BautistaÎncă nu există evaluări

- Laws On Tuition FeesDocument55 paginiLaws On Tuition FeesKym Hernandez100% (1)

- Module 6 Teaching Prof First Sem 2022-23Document33 paginiModule 6 Teaching Prof First Sem 2022-23Merleah Faith Soriano DumaquitÎncă nu există evaluări

- G.R. No. 202792Document7 paginiG.R. No. 202792zelayneÎncă nu există evaluări

- Cir Vs Dlsu, GR No. 196596, November 9, 2016Document3 paginiCir Vs Dlsu, GR No. 196596, November 9, 2016Nathalie YapÎncă nu există evaluări

- Laws Affecting The Teaching ProfessionDocument31 paginiLaws Affecting The Teaching ProfessionDiane Navarrete100% (1)

- Prof. Ed. 101 SG6Document71 paginiProf. Ed. 101 SG6Allysa Shane Paningbatan RascoÎncă nu există evaluări

- Cir Vs Dlsu, GR No. 196596, November 9, 2016Document3 paginiCir Vs Dlsu, GR No. 196596, November 9, 2016I took her to my penthouse and i freaked itÎncă nu există evaluări

- Free High School - RA 6655Document3 paginiFree High School - RA 6655Allan Jr PanchoÎncă nu există evaluări

- CIR Vs DLSUDocument3 paginiCIR Vs DLSUHaniya Solaiman GuroÎncă nu există evaluări

- 000.000ra 8545Document12 pagini000.000ra 8545remy vegim tevesÎncă nu există evaluări

- Batas Pambansa 232 (An Act Providing For The Establishment and Maintenance of An Integrated System of Education)Document36 paginiBatas Pambansa 232 (An Act Providing For The Establishment and Maintenance of An Integrated System of Education)Emily SalinasalÎncă nu există evaluări

- Tax Exemption For Nonprofit Schools: Artemio V. Panganiban @inquirerdotnetDocument3 paginiTax Exemption For Nonprofit Schools: Artemio V. Panganiban @inquirerdotnetKenneth Bryan Tegerero TegioÎncă nu există evaluări

- RMC 78-2022Document3 paginiRMC 78-2022Ian PalmaÎncă nu există evaluări

- Accounting of School FundDocument14 paginiAccounting of School FundQuel MadrigalÎncă nu există evaluări

- I.R.R. 9048Document6 paginiI.R.R. 9048Mary Ann Farcon VelascoÎncă nu există evaluări

- 2.4 SEC Opinion Re Power of The Board To Enter Into Suretyship Agreements and To Issue Corporate Guarantees PDFDocument3 pagini2.4 SEC Opinion Re Power of The Board To Enter Into Suretyship Agreements and To Issue Corporate Guarantees PDFAira Mae LayloÎncă nu există evaluări

- CMO-20-2008 Amended Guidelines in Computing Redemption ValueDocument3 paginiCMO-20-2008 Amended Guidelines in Computing Redemption ValueMary Ann Farcon VelascoÎncă nu există evaluări

- Blank Reception ContractDocument6 paginiBlank Reception ContractMary Ann Farcon VelascoÎncă nu există evaluări

- Energy Regulatory Commissi: Llocumt'Document18 paginiEnergy Regulatory Commissi: Llocumt'Mary Ann Farcon VelascoÎncă nu există evaluări

- DOJ Department Circular 05-2015Document8 paginiDOJ Department Circular 05-2015Liz ZubiriÎncă nu există evaluări

- RR No. 4-2018Document9 paginiRR No. 4-2018NewCovenantChurchÎncă nu există evaluări

- Event Space Rental Agreement and Contract 5aab99851723ddbd6a79429bDocument5 paginiEvent Space Rental Agreement and Contract 5aab99851723ddbd6a79429bMary Ann Farcon VelascoÎncă nu există evaluări

- RMO - 9-2014 - Request For Tax Rulings PDFDocument4 paginiRMO - 9-2014 - Request For Tax Rulings PDFMary Ann Farcon VelascoÎncă nu există evaluări

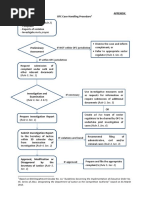

- APPENDIX - Case-Handling Procedure Flowchart PDFDocument1 paginăAPPENDIX - Case-Handling Procedure Flowchart PDFMary Ann Farcon VelascoÎncă nu există evaluări

- Legal EducationDocument25 paginiLegal EducationMary Ann Farcon VelascoÎncă nu există evaluări

- RMO No. 17-2016Document7 paginiRMO No. 17-2016leeÎncă nu există evaluări

- MindspcaeDocument512 paginiMindspcaeVaibhavÎncă nu există evaluări

- Demand Letter WiwiDocument1 paginăDemand Letter WiwiflippinturtleÎncă nu există evaluări

- BBM 301 Advanced Accounting Chapter 1, Section 2Document6 paginiBBM 301 Advanced Accounting Chapter 1, Section 2lil telÎncă nu există evaluări

- Polo Pantaleon V American ExpressDocument10 paginiPolo Pantaleon V American ExpressLyleThereseÎncă nu există evaluări

- PRESS RELEASE: Mohawk Council of Kahnawà:ke Signs MOU With Health CanadaDocument1 paginăPRESS RELEASE: Mohawk Council of Kahnawà:ke Signs MOU With Health CanadaReal Peoples MediaÎncă nu există evaluări

- Research ProposalDocument2 paginiResearch ProposalNina MateiÎncă nu există evaluări

- VANTAGE 850dda ManualDocument32 paginiVANTAGE 850dda ManualRob SeamanÎncă nu există evaluări

- Dancing Queen Chord F PDFDocument27 paginiDancing Queen Chord F PDFyouedanÎncă nu există evaluări

- Information Assurance Security 11Document18 paginiInformation Assurance Security 11laloÎncă nu există evaluări

- Notes On Qawaid FiqhiyaDocument2 paginiNotes On Qawaid FiqhiyatariqsoasÎncă nu există evaluări

- Celebration of International Day For Street ChildrenDocument3 paginiCelebration of International Day For Street ChildrenGhanaWeb EditorialÎncă nu există evaluări

- TNPSC Group 1,2,4,8 VAO Preparation 1Document5 paginiTNPSC Group 1,2,4,8 VAO Preparation 1SakthiÎncă nu există evaluări

- New Income Slab Rates CalculationsDocument6 paginiNew Income Slab Rates Calculationsphani raja kumarÎncă nu există evaluări

- SinDocument26 paginiSinAJÎncă nu există evaluări

- Parts of A DecisionDocument3 paginiParts of A DecisionChristine-Thine Malaga CuliliÎncă nu există evaluări

- John Lewis Snead v. W. Frank Smyth, JR., Superintendent of The Virginia State Penitentiary, 273 F.2d 838, 4th Cir. (1959)Document6 paginiJohn Lewis Snead v. W. Frank Smyth, JR., Superintendent of The Virginia State Penitentiary, 273 F.2d 838, 4th Cir. (1959)Scribd Government DocsÎncă nu există evaluări

- AEC - 12 - Q1 - 0401 - SS2 Reinforcement - Investments, Interest Rate, and Rental Concerns of Filipino EntrepreneursDocument5 paginiAEC - 12 - Q1 - 0401 - SS2 Reinforcement - Investments, Interest Rate, and Rental Concerns of Filipino EntrepreneursVanessa Fampula FaigaoÎncă nu există evaluări

- Retainer Contract - Atty. AtoDocument2 paginiRetainer Contract - Atty. AtoClemente PanganduyonÎncă nu există evaluări

- Untitled DocumentDocument16 paginiUntitled DocumentJolina CabardoÎncă nu există evaluări

- How Jesus Transforms The 10 CommandmentsDocument24 paginiHow Jesus Transforms The 10 CommandmentsJohn JiangÎncă nu există evaluări

- 2.7 Industrial and Employee RelationDocument65 pagini2.7 Industrial and Employee RelationadhityakinnoÎncă nu există evaluări

- MSDS - Dispersant SP-27001 - 20200224Document4 paginiMSDS - Dispersant SP-27001 - 20200224pratikbuttepatil52Încă nu există evaluări

- GodsBag Invoice PDFDocument1 paginăGodsBag Invoice PDFambarsinghÎncă nu există evaluări

- The Marriage of King Arthur and Queen GuinevereDocument12 paginiThe Marriage of King Arthur and Queen GuinevereYamila Sosa RodriguezÎncă nu există evaluări

- IEEE Guide For Power System Protection TestingDocument124 paginiIEEE Guide For Power System Protection TestingStedroy Roache100% (15)

- NEW GL Archiving of Totals and DocumentsDocument5 paginiNEW GL Archiving of Totals and Documentsantonio xavierÎncă nu există evaluări

- Background To The Arbitration and Conciliation Act, 1996Document2 paginiBackground To The Arbitration and Conciliation Act, 1996HimanshuÎncă nu există evaluări

- Arthur Andersen Case PDFDocument12 paginiArthur Andersen Case PDFwindow805Încă nu există evaluări

- Labour and Industrial Law: Multiple Choice QuestionsDocument130 paginiLabour and Industrial Law: Multiple Choice QuestionsShubham SaneÎncă nu există evaluări

- COM670 Chapter 5Document19 paginiCOM670 Chapter 5aakapsÎncă nu există evaluări