S-ar putea să vă placă și

- Bin Card System Stock ControlDocument2 paginiBin Card System Stock ControlYobsanÎncă nu există evaluări

- Lecture 4 - Cost & Management Accounting - March 10, 209 - 3pm To 6pmDocument8 paginiLecture 4 - Cost & Management Accounting - March 10, 209 - 3pm To 6pmBhunesh KumarÎncă nu există evaluări

- Topic 3 Maintain Records of Stored GoodsDocument11 paginiTopic 3 Maintain Records of Stored GoodsFaith KemumaÎncă nu există evaluări

- Functions of StoresDocument3 paginiFunctions of StoresmacrossÎncă nu există evaluări

- AIS Chapter 13 Expenditure CycleDocument39 paginiAIS Chapter 13 Expenditure CycleShakuli YesrÎncă nu există evaluări

- Module II - (Materials)Document8 paginiModule II - (Materials)Nivedita GoswamiÎncă nu există evaluări

- Store Keeping and Clearing and ForwardingDocument10 paginiStore Keeping and Clearing and ForwardingSooraj PurushothamanÎncă nu există evaluări

- Direct Materials NotesDocument6 paginiDirect Materials NotesAizat HakimiÎncă nu există evaluări

- UntitledDocument131 paginiUntitledSebastian KudjoeÎncă nu există evaluări

- Store ResponsibilitiesDocument5 paginiStore ResponsibilitiesShahzadÎncă nu există evaluări

- Storemanagement Unit 5Document82 paginiStoremanagement Unit 5Shifali MandhaniaÎncă nu există evaluări

- Stock ControlDocument8 paginiStock ControlhossainmzÎncă nu există evaluări

- Inventory Management: Organization's Policies, Procedures and Practices May IncludeDocument6 paginiInventory Management: Organization's Policies, Procedures and Practices May IncludenigusÎncă nu există evaluări

- Materi Minggu 8Document89 paginiMateri Minggu 8Zihan AbdullahÎncă nu există evaluări

- Chapter 5 & 6 Editted StorageDocument12 paginiChapter 5 & 6 Editted StorageMOHAMMED KEDIRÎncă nu există evaluări

- Suggested Stocktaking Procedure OverviewDocument4 paginiSuggested Stocktaking Procedure OverviewayyazmÎncă nu există evaluări

- Inventory MemoDocument3 paginiInventory MemoBryan Ramos57% (7)

- Sadiq 3rdDocument79 paginiSadiq 3rdraufÎncă nu există evaluări

- CACS Restaurant Operation: Cost Control, Inventory Management and FraudDocument20 paginiCACS Restaurant Operation: Cost Control, Inventory Management and FraudTesda CACSÎncă nu există evaluări

- Sadiq FridayDocument72 paginiSadiq FridayraufÎncă nu există evaluări

- Agenda: ShrinkageDocument9 paginiAgenda: Shrinkagesohan0105Încă nu există evaluări

- SCM Exam BadagreDocument5 paginiSCM Exam BadagreJhecyl Ann BasagreÎncă nu există evaluări

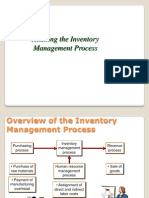

- Auditing The Inventory Management ProcessDocument15 paginiAuditing The Inventory Management ProcessGohar Mahmood100% (1)

- Business Intelligent: Unit 14: Unit TitleDocument8 paginiBusiness Intelligent: Unit 14: Unit TitlekevinÎncă nu există evaluări

- Inventory Audit-Importance and ProceduresDocument17 paginiInventory Audit-Importance and Procedurescriselda salazarÎncă nu există evaluări

- CC Unit 2 Lo1 Maintain Stock Levels & RecordsDocument7 paginiCC Unit 2 Lo1 Maintain Stock Levels & RecordsRogel SoÎncă nu există evaluări

- Store ManagementDocument40 paginiStore ManagementSashi RajÎncă nu există evaluări

- United Methodist University GoodDocument13 paginiUnited Methodist University GoodWidimongar JarqueÎncă nu există evaluări

- Management of Stores: Prepared By:Abhinav SinghDocument36 paginiManagement of Stores: Prepared By:Abhinav SinghfikrhomeÎncă nu există evaluări

- Storing & Issuing ControlsDocument17 paginiStoring & Issuing ControlsSubas ShresthaÎncă nu există evaluări

- Mamo Unit 2 Task 9Document4 paginiMamo Unit 2 Task 9muhammad kaleemÎncă nu există evaluări

- Material Control: Prepared by Mr. Rahul BerryDocument31 paginiMaterial Control: Prepared by Mr. Rahul BerryAastha PanditÎncă nu există evaluări

- Inventory Management Technique in Pharma Industry..Document14 paginiInventory Management Technique in Pharma Industry..Ilayaraja BoopathyÎncă nu există evaluări

- One Person From The Finance Department This Will Give The Actual Inventory in Stores and Also Reconcile With TheDocument2 paginiOne Person From The Finance Department This Will Give The Actual Inventory in Stores and Also Reconcile With ThepowellarryÎncă nu există evaluări

- Course Name Course Code Assignment OnDocument11 paginiCourse Name Course Code Assignment OnMd.Amir hossain khanÎncă nu există evaluări

- Control & Order Stock: Sriram - Ramanathan@tafensw - Edu.auDocument20 paginiControl & Order Stock: Sriram - Ramanathan@tafensw - Edu.aumisrak admassuÎncă nu există evaluări

- SITXINV401 Control Stock - Student Guide WMDocument7 paginiSITXINV401 Control Stock - Student Guide WMOm LalchandaniÎncă nu există evaluări

- Warehouse Management Semis1 Warehouse Process From Replenishment To DispatchDocument9 paginiWarehouse Management Semis1 Warehouse Process From Replenishment To DispatchJay GalleroÎncă nu există evaluări

- Inventory ControlDocument23 paginiInventory ControlKomal RatraÎncă nu există evaluări

- Functions of InventoryDocument22 paginiFunctions of InventoryAshiqul Islam100% (4)

- Stock Verifications Part 2Document26 paginiStock Verifications Part 2Anand DubeyÎncă nu există evaluări

- Operations Research 2Document132 paginiOperations Research 2Cesar Amante TingÎncă nu există evaluări

- Module 2 Accounting For MaterialsDocument32 paginiModule 2 Accounting For MaterialsGhillian Mae GuiangÎncă nu există evaluări

- Material CostingDocument12 paginiMaterial CostingEniola OgunmonaÎncă nu există evaluări

- Periodic Inventory SystemDocument16 paginiPeriodic Inventory SystemSohel Bangi100% (1)

- SCM Module3 Questions and AnswersDocument21 paginiSCM Module3 Questions and AnswersibdiubuvÎncă nu există evaluări

- Aung Kyaw Moe-Task (9) - Unit (2) Warehouse and InventoryDocument5 paginiAung Kyaw Moe-Task (9) - Unit (2) Warehouse and InventoryAung Kyaw Moe100% (1)

- The Audit of InventoriesDocument6 paginiThe Audit of InventoriesIftekhar Ifte100% (3)

- 10.stores MaangementDocument21 pagini10.stores MaangementHeavy Gunner100% (1)

- 3-2 Inventory ManagementDocument20 pagini3-2 Inventory ManagementDwi Mulyanti DwimulyantishopÎncă nu există evaluări

- Warehouse Process From Replenishment To DispatchDocument9 paginiWarehouse Process From Replenishment To DispatchErika ApitaÎncă nu există evaluări

- Lesson 18-19-20!21!22 Inventory ManagementDocument4 paginiLesson 18-19-20!21!22 Inventory ManagementChaqib SultanÎncă nu există evaluări

- Stock ControlDocument28 paginiStock ControljohnkwashanaiÎncă nu există evaluări

- Inventory Management21Document76 paginiInventory Management21Sayem SadatÎncă nu există evaluări

- Direct and Indirect MaterialsDocument19 paginiDirect and Indirect MaterialsKraziegyrl LovesUtoomuch0% (1)

- Inventory ControlDocument11 paginiInventory Controlshamlee ramtekeÎncă nu există evaluări

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDe la EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsEvaluare: 5 din 5 stele5/5 (1)

- Surviving the Spare Parts Crisis: Maintenance Storeroom and Inventory ControlDe la EverandSurviving the Spare Parts Crisis: Maintenance Storeroom and Inventory ControlÎncă nu există evaluări

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursDe la EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursÎncă nu există evaluări

- The Inf Luence of Extra Regional Territories On The CaribbeanDocument13 paginiThe Inf Luence of Extra Regional Territories On The CaribbeanSash1693Încă nu există evaluări

- Caribbean - Global InteractionsDocument24 paginiCaribbean - Global InteractionsSash1693100% (1)

- SS (S.b.a.)Document16 paginiSS (S.b.a.)Sash1693Încă nu există evaluări

- Hall Application Form PDFDocument2 paginiHall Application Form PDFSash1693Încă nu există evaluări

- Social JusticeDocument24 paginiSocial JusticeSash1693Încă nu există evaluări

- Basic Facts About RealDocument35 paginiBasic Facts About RealSash1693Încă nu există evaluări

- QuestionaireDocument3 paginiQuestionaireSash1693Încă nu există evaluări

- An Example of An AutobiographyDocument1 paginăAn Example of An AutobiographySash1693Încă nu există evaluări

- Atmospheric Pollution NotesDocument23 paginiAtmospheric Pollution NotesSash1693Încă nu există evaluări

- Scan 0008Document1 paginăScan 0008Sash1693Încă nu există evaluări

- UV / Vis Spectroscopy: Mr. Z. ClarkeDocument41 paginiUV / Vis Spectroscopy: Mr. Z. ClarkeSash1693Încă nu există evaluări

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Cape Chemistry 2Document4 paginiCape Chemistry 2Sash16930% (2)

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Health and Safety ProceduresDocument10 paginiHealth and Safety ProceduresSash1693100% (1)

- Health and Safety ProceduresDocument10 paginiHealth and Safety ProceduresSash1693100% (1)

- Caribbean Studies QuestionsDocument1 paginăCaribbean Studies QuestionsSash1693Încă nu există evaluări

- Follow Health, Safety & Security ProceduresDocument31 paginiFollow Health, Safety & Security ProceduresSash1693Încă nu există evaluări

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Scan 0011Document1 paginăScan 0011Sash1693Încă nu există evaluări

- Caribbean StudiesDocument1 paginăCaribbean StudiesSash1693Încă nu există evaluări

- Cultural Differences: AmericansDocument3 paginiCultural Differences: AmericansSash1693Încă nu există evaluări

- Anger ManagementDocument2 paginiAnger ManagementSash1693Încă nu există evaluări

- Scan 0008Document1 paginăScan 0008Sash1693Încă nu există evaluări

- Volunteer SheetDocument3 paginiVolunteer SheetSash1693Încă nu există evaluări

- ChromatographyDocument33 paginiChromatographySash16930% (1)

- Scan 0010Document1 paginăScan 0010Sash1693Încă nu există evaluări

- Payment Plan 3-C-3Document2 paginiPayment Plan 3-C-3Zeeshan RasoolÎncă nu există evaluări

- Dreamfoil Creations & Nemeth DesignsDocument22 paginiDreamfoil Creations & Nemeth DesignsManoel ValentimÎncă nu există evaluări

- I.V. FluidDocument4 paginiI.V. FluidOdunlamiÎncă nu există evaluări

- Safety Inspection Checklist Project: Location: Inspector: DateDocument2 paginiSafety Inspection Checklist Project: Location: Inspector: Dateyono DaryonoÎncă nu există evaluări

- SWOT AnalysisDocument6 paginiSWOT AnalysisSSPK_92Încă nu există evaluări

- Oasis 360 Overview 0710Document21 paginiOasis 360 Overview 0710mychar600% (1)

- Pyro ShieldDocument6 paginiPyro Shieldmunim87Încă nu există evaluări

- Developments in Prepress Technology (PDFDrive)Document62 paginiDevelopments in Prepress Technology (PDFDrive)Sur VelanÎncă nu există evaluări

- Sewing Machins Operations ManualDocument243 paginiSewing Machins Operations ManualjemalÎncă nu există evaluări

- Coursework For ResumeDocument7 paginiCoursework For Resumeafjwdxrctmsmwf100% (2)

- MG206 Chapter 3 Slides On Marketing Principles and StrategiesDocument33 paginiMG206 Chapter 3 Slides On Marketing Principles and StrategiesIsfundiyerTaungaÎncă nu există evaluări

- A.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdDocument6 paginiA.2 de - La - Victoria - v. - Commission - On - Elections20210424-12-18iwrdCharisse SarateÎncă nu există evaluări

- Part A Plan: Simple Calculater Using Switch CaseDocument7 paginiPart A Plan: Simple Calculater Using Switch CaseRahul B. FereÎncă nu există evaluări

- 1.6 Program AdministrationDocument56 pagini1.6 Program Administration'JeoffreyLaycoÎncă nu există evaluări

- Mutual Fund Insight Nov 2022Document214 paginiMutual Fund Insight Nov 2022Sonic LabelsÎncă nu există evaluări

- ADS Chapter 303 Grants and Cooperative Agreements Non USDocument81 paginiADS Chapter 303 Grants and Cooperative Agreements Non USMartin JcÎncă nu există evaluări

- Chapter03 - How To Retrieve Data From A Single TableDocument35 paginiChapter03 - How To Retrieve Data From A Single TableGML KillÎncă nu există evaluări

- Occupational Therapy in Mental HealthDocument16 paginiOccupational Therapy in Mental HealthjethasÎncă nu există evaluări

- Elb v2 ApiDocument180 paginiElb v2 ApikhalandharÎncă nu există evaluări

- Database Management System and SQL CommandsDocument3 paginiDatabase Management System and SQL Commandsdev guptaÎncă nu există evaluări

- Enumerator ResumeDocument1 paginăEnumerator Resumesaid mohamudÎncă nu există evaluări

- Seminar Report of Automatic Street Light: Presented byDocument14 paginiSeminar Report of Automatic Street Light: Presented byTeri Maa Ki100% (2)

- Introduction To Radar Warning ReceiverDocument23 paginiIntroduction To Radar Warning ReceiverPobitra Chele100% (1)

- Chap 06 Ans Part 2Document18 paginiChap 06 Ans Part 2Janelle Joyce MuhiÎncă nu există evaluări

- How To Unbrick Tp-Link Wifi Router Wr841Nd Using TFTP and WiresharkDocument13 paginiHow To Unbrick Tp-Link Wifi Router Wr841Nd Using TFTP and WiresharkdanielÎncă nu există evaluări

- MDC PT ChartDocument2 paginiMDC PT ChartKailas NimbalkarÎncă nu există evaluări

- Pradhan Mantri Gramin Digital Saksharta Abhiyan (PMGDISHA) Digital Literacy Programme For Rural CitizensDocument2 paginiPradhan Mantri Gramin Digital Saksharta Abhiyan (PMGDISHA) Digital Literacy Programme For Rural Citizenssairam namakkalÎncă nu există evaluări

- 14 CE Chapter 14 - Developing Pricing StrategiesDocument34 pagini14 CE Chapter 14 - Developing Pricing StrategiesAsha JaylalÎncă nu există evaluări

- Nasoya FoodsDocument2 paginiNasoya Foodsanamta100% (1)

- Installation Manual EnUS 2691840011Document4 paginiInstallation Manual EnUS 2691840011Patts MarcÎncă nu există evaluări