S-ar putea să vă placă și

- Should Immediate Annuities Be a Tool in Your Retirement Planning Toolbox?De la EverandShould Immediate Annuities Be a Tool in Your Retirement Planning Toolbox?Încă nu există evaluări

- ch4 5Document37 paginich4 5BobÎncă nu există evaluări

- Presentation Nasim BegDocument19 paginiPresentation Nasim BegS. Emaad UddinÎncă nu există evaluări

- Chapter 6 - Social Insurance Social Security and Unemployment InsuranceDocument15 paginiChapter 6 - Social Insurance Social Security and Unemployment InsuranceMey MeyÎncă nu există evaluări

- Project On Pension Funds Submitted To: Ma Am Saadia Noureen: Submitted By: Shafaq Munir Iqra Mazhar Aamna ImtiazDocument16 paginiProject On Pension Funds Submitted To: Ma Am Saadia Noureen: Submitted By: Shafaq Munir Iqra Mazhar Aamna Imtiazaaminahsheikh92Încă nu există evaluări

- Effect of Pension Funds Characteristics On Financial Performance of Pension Administrators Chapter OneDocument39 paginiEffect of Pension Funds Characteristics On Financial Performance of Pension Administrators Chapter OneUmar FarouqÎncă nu există evaluări

- Case Studies in Retirement System ReformDocument60 paginiCase Studies in Retirement System ReformEdis ChÎncă nu există evaluări

- National Retirement: New Zealand and The United KingdomDocument37 paginiNational Retirement: New Zealand and The United KingdomNor Iskandar Md NorÎncă nu există evaluări

- National Pension System (Blackbook)Document86 paginiNational Pension System (Blackbook)chirag karara100% (2)

- Asc380 Topic 2 PDFDocument52 paginiAsc380 Topic 2 PDFZaffrin ShahÎncă nu există evaluări

- Learner Guide 242613Document59 paginiLearner Guide 242613palmalynchwatersÎncă nu există evaluări

- Hbs Case Fund Management Group 7: Erika 410636061 Nokwanda 410636064 Franklin 410532065Document21 paginiHbs Case Fund Management Group 7: Erika 410636061 Nokwanda 410636064 Franklin 410532065Martina InaÎncă nu există evaluări

- Foundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions ManualDocument8 paginiFoundations of Financial Markets and Institutions 4th Edition Fabozzi Solutions Manualfinificcodille6d3h100% (22)

- Retirement PlanningDocument104 paginiRetirement PlanningPartik Bansal100% (9)

- Untitled PresentationDocument21 paginiUntitled PresentationNeeraj DubeyÎncă nu există evaluări

- Health Insurance Unit - 4: Soumendra RoyDocument27 paginiHealth Insurance Unit - 4: Soumendra RoybapparoyÎncă nu există evaluări

- Chapter 1 Lecture Notes.2021Document18 paginiChapter 1 Lecture Notes.2021Hoyin SinÎncă nu există evaluări

- Insurance ProjectDocument16 paginiInsurance ProjectSomil ShahÎncă nu există evaluări

- Module 3Document48 paginiModule 3Ankit JajalÎncă nu există evaluări

- Pension Topic One and TwoDocument7 paginiPension Topic One and Twonogarap767Încă nu există evaluări

- MPSM609 Social Security in Ghana - Lecture-5Document56 paginiMPSM609 Social Security in Ghana - Lecture-5nanayaw asareÎncă nu există evaluări

- Act404 Slides 2Document14 paginiAct404 Slides 2SEIDU ISSAHAKUÎncă nu există evaluări

- Retirement Planning BasicsDocument24 paginiRetirement Planning BasicsJakeWillÎncă nu există evaluări

- Chapter 6: Pension Fund: Definition: A Pension Plan Is A Fund That Is EstablishedDocument11 paginiChapter 6: Pension Fund: Definition: A Pension Plan Is A Fund That Is EstablishedJahangir AlamÎncă nu există evaluări

- Broad-Based Growth VitalDocument3 paginiBroad-Based Growth VitalTithi jainÎncă nu există evaluări

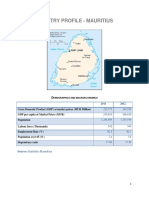

- Mauritius Pension System ProfileDocument9 paginiMauritius Pension System ProfileDarren OwenÎncă nu există evaluări

- Sept Briefing National Institute For Retirement SecurityDocument37 paginiSept Briefing National Institute For Retirement Securitypcapineri8399Încă nu există evaluări

- Wealth Management - PPTX 06-11-2019Document14 paginiWealth Management - PPTX 06-11-2019Sree LakshmyÎncă nu există evaluări

- Pension Funds Globally, in Asia and in PakistanDocument39 paginiPension Funds Globally, in Asia and in Pakistantayeba87Încă nu există evaluări

- Keywords:: Pension Pension Reform Workers Well-Being Error Correction ModelDocument14 paginiKeywords:: Pension Pension Reform Workers Well-Being Error Correction ModelrevolutionguyÎncă nu există evaluări

- Group 10 (Pension Funds) .Document18 paginiGroup 10 (Pension Funds) .Odunukwe ChiamakaÎncă nu există evaluări

- Comparative Pensions Systems in Africa PresentationDocument30 paginiComparative Pensions Systems in Africa Presentationnanayaw asareÎncă nu există evaluări

- Lic 1234Document19 paginiLic 1234deva_41Încă nu există evaluări

- Dynamics of Population Ageing by Tarun DasDocument18 paginiDynamics of Population Ageing by Tarun DasProfessor Tarun DasÎncă nu există evaluări

- Module10 Posarac PDFDocument79 paginiModule10 Posarac PDFÁlvaro DíazÎncă nu există evaluări

- Social Policy, Society and Change - 2015 - 6Document69 paginiSocial Policy, Society and Change - 2015 - 6Ellen MaharaniÎncă nu există evaluări

- 4% Withdrawal RateDocument12 pagini4% Withdrawal RatesantoshÎncă nu există evaluări

- Social Security - Odt - 1Document1 paginăSocial Security - Odt - 1jolÎncă nu există evaluări

- IAS Group1Document7 paginiIAS Group1Carol PhaswanaÎncă nu există evaluări

- Pension Reform in India - A Social Security Need (D. Swarup, Chairman, PFRDA)Document16 paginiPension Reform in India - A Social Security Need (D. Swarup, Chairman, PFRDA)Andre NoortÎncă nu există evaluări

- How To "Pensionize" Any IRA or 401 (K) PlanDocument19 paginiHow To "Pensionize" Any IRA or 401 (K) PlanPhil PhillipsÎncă nu există evaluări

- Fim ProjectDocument31 paginiFim Projectaaminahsheikh92Încă nu există evaluări

- By Jeffrey A. Miron: The Arguments For Government Intervention in Private Savings DecisionsDocument4 paginiBy Jeffrey A. Miron: The Arguments For Government Intervention in Private Savings DecisionsEfe YıldızÎncă nu există evaluări

- E.Types of Retirement Plans-1Document13 paginiE.Types of Retirement Plans-1Madhu dollyÎncă nu există evaluări

- Final Chapter 1 N 2Document30 paginiFinal Chapter 1 N 2Musariri TalentÎncă nu există evaluări

- The National Health Insurance Act R.A. No. 7875 As Amended by R.A. 9241Document24 paginiThe National Health Insurance Act R.A. No. 7875 As Amended by R.A. 9241Alexis Erica Bansuan OvaloÎncă nu există evaluări

- Hedge Yourself From The Financial Adversities Due To COVID-19Document12 paginiHedge Yourself From The Financial Adversities Due To COVID-19Deepak G100% (1)

- Literature Review of Pension FundDocument8 paginiLiterature Review of Pension Funddhjiiorif100% (1)

- 01 SynopsisDocument11 pagini01 SynopsisvadansukhvindersinghÎncă nu există evaluări

- Pension Chap 1 IntroductionDocument5 paginiPension Chap 1 IntroductionJoe KimÎncă nu există evaluări

- The Pensions Lifetime Allowance: Adviser GuideDocument7 paginiThe Pensions Lifetime Allowance: Adviser GuidesrowbothamÎncă nu există evaluări

- A Study On National Pension Schemes in IndiaDocument59 paginiA Study On National Pension Schemes in IndiaRajesh BathulaÎncă nu există evaluări

- How To "Pensionize" Any IRA or 401 (K) PlanDocument22 paginiHow To "Pensionize" Any IRA or 401 (K) PlanLuis PereiraÎncă nu există evaluări

- Retirement Planning Basics: (Page 1 of 24)Document24 paginiRetirement Planning Basics: (Page 1 of 24)Goutam ReddyÎncă nu există evaluări

- quot Saving" Social Security Is Not Enough, Cato Social Security Choice Paper No. 20Document10 paginiquot Saving" Social Security Is Not Enough, Cato Social Security Choice Paper No. 20Cato InstituteÎncă nu există evaluări

- Module 10 - Medical BillingDocument15 paginiModule 10 - Medical BillingSusan FÎncă nu există evaluări

- Retirement PlanDocument96 paginiRetirement PlanAmrin ChaudharyÎncă nu există evaluări

- Government Accountability Office - Ensuring Income Throughout Retirement Requires Difficult ChoicesDocument79 paginiGovernment Accountability Office - Ensuring Income Throughout Retirement Requires Difficult ChoicesEphraim DavisÎncă nu există evaluări

- Report On Organizational Behavior of NIB BankDocument23 paginiReport On Organizational Behavior of NIB Bankmishel26Încă nu există evaluări

- A Diamond Personality Case StudyDocument14 paginiA Diamond Personality Case Studyhotmale_taimour100% (2)

- Free Scale AnswersDocument4 paginiFree Scale Answersmishel26Încă nu există evaluări

- What Is Organizational Behavior?Document38 paginiWhat Is Organizational Behavior?Zeeshan_Haque_3826Încă nu există evaluări

- Shazia TehmasDocument2 paginiShazia Tehmasmishel26Încă nu există evaluări

- Elder Abuse Neglect ReportDocument31 paginiElder Abuse Neglect Reportmishel26100% (1)

- Deep Sea Electronics PLC: DSE103 MKII Speed Switch PC Configuration Suite LiteDocument14 paginiDeep Sea Electronics PLC: DSE103 MKII Speed Switch PC Configuration Suite LiteMostafa ShannaÎncă nu există evaluări

- Helsingborg EngDocument8 paginiHelsingborg EngMassaCoÎncă nu există evaluări

- 14 DETEMINANTS & MATRICES PART 3 of 6 PDFDocument10 pagini14 DETEMINANTS & MATRICES PART 3 of 6 PDFsabhari_ramÎncă nu există evaluări

- Engineering Materials-Istanbul .Technical UniversityDocument40 paginiEngineering Materials-Istanbul .Technical UniversitybuggrraaÎncă nu există evaluări

- Adding Print PDF To Custom ModuleDocument3 paginiAdding Print PDF To Custom ModuleNguyễn Vương AnhÎncă nu există evaluări

- Digest of Ganila Vs CADocument1 paginăDigest of Ganila Vs CAJohn Lester LantinÎncă nu există evaluări

- CERES News Digest - Week 11, Vol.4, March 31-April 4Document6 paginiCERES News Digest - Week 11, Vol.4, March 31-April 4Center for Eurasian, Russian and East European StudiesÎncă nu există evaluări

- FC2060Document10 paginiFC2060esnÎncă nu există evaluări

- ASTM A586-04aDocument6 paginiASTM A586-04aNadhiraÎncă nu există evaluări

- RS485 ManualDocument7 paginiRS485 Manualndtruc100% (2)

- Scout Activities On The Indian Railways - Original Order: MC No. SubjectDocument4 paginiScout Activities On The Indian Railways - Original Order: MC No. SubjectVikasvijay SinghÎncă nu există evaluări

- Q3 Week 1 Homeroom Guidance JGRDocument9 paginiQ3 Week 1 Homeroom Guidance JGRJasmin Goot Rayos50% (4)

- An Analytical Study On Impact of Credit Rating Agencies in India 'S DevelopmentDocument14 paginiAn Analytical Study On Impact of Credit Rating Agencies in India 'S DevelopmentRamneet kaur (Rizzy)Încă nu există evaluări

- Pfmar SampleDocument15 paginiPfmar SampleJustin Briggs86% (7)

- Curriculum Vitae H R VijayDocument8 paginiCurriculum Vitae H R VijayvijaygowdabdvtÎncă nu există evaluări

- CPI As A KPIDocument13 paginiCPI As A KPIKS LimÎncă nu există evaluări

- Instructions For The Safe Use Of: Web LashingsDocument2 paginiInstructions For The Safe Use Of: Web LashingsVij Vaibhav VermaÎncă nu există evaluări

- DenmarkDocument4 paginiDenmarkFalcon KingdomÎncă nu există evaluări

- Leadership Style SurveyDocument3 paginiLeadership Style SurveyJanelle BergÎncă nu există evaluări

- Quiz1 2, PrelimDocument14 paginiQuiz1 2, PrelimKyla Mae MurphyÎncă nu există evaluări

- Legal Environment of Business 7th Edition Kubasek Solutions Manual Full Chapter PDFDocument34 paginiLegal Environment of Business 7th Edition Kubasek Solutions Manual Full Chapter PDFlongchadudz100% (12)

- X606 PDFDocument1 paginăX606 PDFDany OrioliÎncă nu există evaluări

- PT Shri Krishna Sejahtera: Jalan Pintu Air Raya No. 56H, Pasar Baru Jakarta Pusat 10710 Jakarta - IndonesiaDocument16 paginiPT Shri Krishna Sejahtera: Jalan Pintu Air Raya No. 56H, Pasar Baru Jakarta Pusat 10710 Jakarta - IndonesiaihsanlaidiÎncă nu există evaluări

- Biotechnology WebquestDocument2 paginiBiotechnology Webquestapi-353567032Încă nu există evaluări

- Assignment 03 Investments in Debt SecuritiesDocument4 paginiAssignment 03 Investments in Debt SecuritiesJella Mae YcalinaÎncă nu există evaluări

- Firmware Upgrade To SP3 From SP2: 1. Download Necessary Drivers For The OMNIKEY 5427 CKDocument6 paginiFirmware Upgrade To SP3 From SP2: 1. Download Necessary Drivers For The OMNIKEY 5427 CKFilip Andru MorÎncă nu există evaluări

- Azure Subscription and Service Limits, Quotas, and ConstraintsDocument54 paginiAzure Subscription and Service Limits, Quotas, and ConstraintsSorinÎncă nu există evaluări

- LG+32LX330C Ga LG5CBDocument55 paginiLG+32LX330C Ga LG5CBjampcarlosÎncă nu există evaluări

- A Case Study From The: PhilippinesDocument2 paginiA Case Study From The: PhilippinesNimÎncă nu există evaluări

- Lecture 3 - Marriage and Marriage PaymentsDocument11 paginiLecture 3 - Marriage and Marriage PaymentsGrace MguniÎncă nu există evaluări