S-ar putea să vă placă și

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (119)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- 1 Om PPT M-1Document89 pagini1 Om PPT M-1K P RUTHWIKÎncă nu există evaluări

- Solutions To Chapter 2Document9 paginiSolutions To Chapter 2Alma Delos SantosÎncă nu există evaluări

- Report Financial Management PM & WMDocument28 paginiReport Financial Management PM & WMCy PenolÎncă nu există evaluări

- How To Succeed As An Independent Marketing ConsultantDocument147 paginiHow To Succeed As An Independent Marketing Consultantdade872Încă nu există evaluări

- Alliance, Acquisitions, Joint Ventures, Strat FormulationDocument16 paginiAlliance, Acquisitions, Joint Ventures, Strat FormulationMilbert John LlenaÎncă nu există evaluări

- Ch08 PricingDocument69 paginiCh08 PricingDaniel KangÎncă nu există evaluări

- Financial Management Cash Flow AnalysisDocument6 paginiFinancial Management Cash Flow Analysismax zeneÎncă nu există evaluări

- Paper4 CmaDocument9 paginiPaper4 CmaRon Weasley100% (1)

- Lecture 4 Pharmaceutical Marketing PlanDocument35 paginiLecture 4 Pharmaceutical Marketing PlanOla Gamal50% (2)

- Audi and BMW Operational Strategies to Gain Market ShareDocument6 paginiAudi and BMW Operational Strategies to Gain Market ShareNazmus SaifÎncă nu există evaluări

- Chapter 6 (Standard Cost)Document98 paginiChapter 6 (Standard Cost)annur azalillahÎncă nu există evaluări

- Lecture 4 North Country Auto Case Performance MeasurementDocument5 paginiLecture 4 North Country Auto Case Performance MeasurementAprican ApriÎncă nu există evaluări

- Chapter 15 - Mergers and AcquisitionsDocument63 paginiChapter 15 - Mergers and AcquisitionsBahzad BalochÎncă nu există evaluări

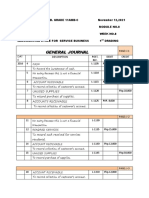

- Accounting Cycle for a Service BusinessDocument5 paginiAccounting Cycle for a Service BusinessKristel Mae PayotÎncă nu există evaluări

- Acctg201 Support Cost Department AllocationDocument3 paginiAcctg201 Support Cost Department AllocationEab RondinaÎncă nu există evaluări

- Bản Sao Của DOWNYDocument50 paginiBản Sao Của DOWNYDuy AnhÎncă nu există evaluări

- Case Study on Marketing Forces Faced by Kamdar GroupDocument9 paginiCase Study on Marketing Forces Faced by Kamdar GroupNatasya SyafinaÎncă nu există evaluări

- CV - Georges Edouard DIASDocument7 paginiCV - Georges Edouard DIASMohamed Ben fadhelÎncă nu există evaluări

- OPTIMIZE CUSTOMER RELATIONSHIPS WITH CRMDocument30 paginiOPTIMIZE CUSTOMER RELATIONSHIPS WITH CRMAVINASH JAINÎncă nu există evaluări

- SB Feed MillsDocument8 paginiSB Feed Millsanum8991100% (1)

- Entrepreneurship Quarter 1 - Module 2 - Lesson 1: The Potential Market and The Market NeedsDocument8 paginiEntrepreneurship Quarter 1 - Module 2 - Lesson 1: The Potential Market and The Market NeedsJason Banay0% (1)

- N5 Financial Accounting November 2016Document10 paginiN5 Financial Accounting November 2016TsholofeloÎncă nu există evaluări

- Group Assignment 1 - Group 5Document9 paginiGroup Assignment 1 - Group 5Suhaimi SuffianÎncă nu există evaluări

- Dari MoochDocument17 paginiDari MoochMírŽʌ TʌłhʌÎncă nu există evaluări

- Rekening Koran Desember Februari 2023Document3 paginiRekening Koran Desember Februari 2023Panji PrakosoÎncă nu există evaluări

- Unit 1 Material Financial AccountingDocument88 paginiUnit 1 Material Financial AccountingKeerthanaÎncă nu există evaluări

- 审计年报2011315Document67 pagini审计年报2011315yf zÎncă nu există evaluări

- Tally Shortcut Keys GuideDocument2 paginiTally Shortcut Keys Guideradha ramaswamyÎncă nu există evaluări

- EbayDocument81 paginiEbayJohnny ChanÎncă nu există evaluări

- VOC To CTQ Conversion SampleDocument5 paginiVOC To CTQ Conversion SampleshivaprasadmvitÎncă nu există evaluări