S-ar putea să vă placă și

- Inventory Accounting: A Comprehensive GuideDe la EverandInventory Accounting: A Comprehensive GuideEvaluare: 5 din 5 stele5/5 (1)

- Internal Control of Fixed Assets: A Controller and Auditor's GuideDe la EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideEvaluare: 4 din 5 stele4/5 (1)

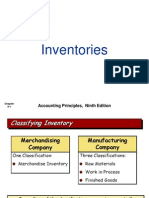

- Inventories: Accounting Principles, Ninth EditionDocument48 paginiInventories: Accounting Principles, Ninth Editionpiash246Încă nu există evaluări

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument66 paginiPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegenaeemakhtaracmaÎncă nu există evaluări

- CH 06Document65 paginiCH 06Chang Chan Chong0% (1)

- Chapter 06 - InventoriesDocument57 paginiChapter 06 - InventoriesDrake AdamÎncă nu există evaluări

- Accounting For InventoriesDocument12 paginiAccounting For InventoriesNoor AlSabbaghÎncă nu există evaluări

- Act 201 Chapter 6Document36 paginiAct 201 Chapter 6Amir HossainÎncă nu există evaluări

- Reporting and Analyzing Inventory: Financial Accounting, Fifth EditionDocument27 paginiReporting and Analyzing Inventory: Financial Accounting, Fifth EditionLinh NguyenÎncă nu există evaluări

- Weygandt Financial 8e PowerPoint Review Ch06Document17 paginiWeygandt Financial 8e PowerPoint Review Ch06Procrastinator OliurÎncă nu există evaluări

- Bab 6 Prinsip Akuntansi 1Document45 paginiBab 6 Prinsip Akuntansi 1Purnama Sari, S.E., M.Ak.Încă nu există evaluări

- Week 11 - 6/12/2010: Quiz 3 - 5 % - Chapter 5 & 6 Class Assignment - 5% - Chapter 6Document63 paginiWeek 11 - 6/12/2010: Quiz 3 - 5 % - Chapter 5 & 6 Class Assignment - 5% - Chapter 6Moath AlobaidyÎncă nu există evaluări

- ch06 - InventoriesDocument63 paginich06 - InventoriesJosua PranataÎncă nu există evaluări

- ch06, Accounting PrinciplesDocument66 paginich06, Accounting PrinciplesH.R. RobinÎncă nu există evaluări

- CH 06Document63 paginiCH 06nastassya ruhukailÎncă nu există evaluări

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument50 paginiPrepared by Coby Harmon University of California, Santa Barbara Westmont CollegeMD. Barkat ullah BijoyÎncă nu există evaluări

- Chapter 2 Accounting For InventoriesDocument51 paginiChapter 2 Accounting For InventoriesAlex HaymeÎncă nu există evaluări

- ACT 201 Chapter 6Document48 paginiACT 201 Chapter 6Sadia ShithyÎncă nu există evaluări

- A201 Ch6 Fall 2013Document44 paginiA201 Ch6 Fall 2013Set LuÎncă nu există evaluări

- Fundamentals of Accounting II, Chapter 1Document51 paginiFundamentals of Accounting II, Chapter 1negussie birieÎncă nu există evaluări

- ACCT 201: Reporting and Analyzing InventoryDocument22 paginiACCT 201: Reporting and Analyzing InventoryDuygu YılmazÎncă nu există evaluări

- Accounting For InventoriesDocument65 paginiAccounting For InventoriesRalph Ernest HulguinÎncă nu există evaluări

- Chapter 1 InventoryDocument50 paginiChapter 1 InventoryThea RothÎncă nu există evaluări

- Sesi Ke 10&11Document40 paginiSesi Ke 10&11Ahmad ZahirÎncă nu există evaluări

- Unit 1 InvetoryDocument53 paginiUnit 1 InvetoryHirut GetachewÎncă nu există evaluări

- Lecture 8 - InventoriesDocument23 paginiLecture 8 - InventoriesIsyraf Hatim Mohd TamizamÎncă nu există evaluări

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument29 paginiIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeBafesh RoyÎncă nu există evaluări

- CH 08Document54 paginiCH 08Stevan PknÎncă nu există evaluări

- Preview of Chapter 1: Financial AccountingDocument74 paginiPreview of Chapter 1: Financial AccountingLê Hồng NhungÎncă nu există evaluări

- Financial Accounting Practice and Review InventoryDocument3 paginiFinancial Accounting Practice and Review Inventoryukandi rukmanaÎncă nu există evaluări

- Chapter 08 Solutions ManualDocument67 paginiChapter 08 Solutions ManualRabiaAjmalÎncă nu există evaluări

- Act512 - Assignment Chapter - 06Document9 paginiAct512 - Assignment Chapter - 06Rafin MahmudÎncă nu există evaluări

- Chapter 6Document28 paginiChapter 6duy blaÎncă nu există evaluări

- Ch6 Inventories BBDocument40 paginiCh6 Inventories BBmkrmashaqÎncă nu există evaluări

- Modified Wey - AP - 8e - Ch06 - RevisedDocument45 paginiModified Wey - AP - 8e - Ch06 - RevisedTanvirÎncă nu există evaluări

- CH 06 SMDocument94 paginiCH 06 SMapi-234680678Încă nu există evaluări

- Kelompok 6 Chapter 6Document11 paginiKelompok 6 Chapter 6leoni pannaÎncă nu există evaluări

- Ifrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument43 paginiIfrs Edition: Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeAhmed El KhateebÎncă nu există evaluări

- Valuation of Inventories: A Cost-Basis ApproachDocument36 paginiValuation of Inventories: A Cost-Basis ApproachjulsÎncă nu există evaluări

- Slide ACC101 Chapter 6 InventoriesDocument50 paginiSlide ACC101 Chapter 6 InventoriesLeojelaineIgcoyÎncă nu există evaluări

- Pengantar Akuntansi 1: SESI - 12Document18 paginiPengantar Akuntansi 1: SESI - 12Sophan SopyanÎncă nu există evaluări

- Learning Objectives: Valuation of Inventories: A Cost - Basis ApproachDocument7 paginiLearning Objectives: Valuation of Inventories: A Cost - Basis ApproachSuraj NamdeoÎncă nu există evaluări

- IFA-I ch-3 Investories NewDocument59 paginiIFA-I ch-3 Investories Newhasenabdi30Încă nu există evaluări

- PPAcct II InventoryDocument9 paginiPPAcct II InventoryNigussie BerhanuÎncă nu există evaluări

- CHAPTER Four NewDocument16 paginiCHAPTER Four NewHace AdisÎncă nu există evaluări

- Session 5 - InventoriesDocument45 paginiSession 5 - Inventoriessdgdfs sdfsfÎncă nu există evaluări

- Final Chapter 6Document8 paginiFinal Chapter 6Đặng Ngọc Thu HiềnÎncă nu există evaluări

- ACT 201 Chapter 6Document80 paginiACT 201 Chapter 6hubbardaudÎncă nu există evaluări

- Chapter 06Document31 paginiChapter 06Trang Quynh DinhÎncă nu există evaluări

- Determining The Monetary Amount of Inventory at Any Given Point in TimeDocument44 paginiDetermining The Monetary Amount of Inventory at Any Given Point in TimeParth R. ShahÎncă nu există evaluări

- Inventory ManagementDocument22 paginiInventory ManagementYolowii XanaÎncă nu există evaluări

- Intermediate I Chapter 8Document45 paginiIntermediate I Chapter 8Aarti JÎncă nu există evaluări

- Chapter 6Document68 paginiChapter 6Hasin EshrakÎncă nu există evaluări

- Inventory Valuation Methods: Treatment in Financial StatementDocument10 paginiInventory Valuation Methods: Treatment in Financial Statementneten_dkjÎncă nu există evaluări

- Inventory and Cost of Goods SoldDocument39 paginiInventory and Cost of Goods SoldIsabell Camillo75% (4)

- INVENTORYDocument5 paginiINVENTORYJenilyn CalaraÎncă nu există evaluări

- CH 06 - Inventories (PA)Document50 paginiCH 06 - Inventories (PA)faraaz360Încă nu există evaluări

- Session 8Document71 paginiSession 8Tram AnhhÎncă nu există evaluări

- Intermidet ch4Document90 paginiIntermidet ch4kqk07829Încă nu există evaluări

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDe la EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsEvaluare: 5 din 5 stele5/5 (1)

- NFRA Letter Regarding Instances of Non-Compliances With Ind AsDocument4 paginiNFRA Letter Regarding Instances of Non-Compliances With Ind AsvisshelpÎncă nu există evaluări

- HRA & Forensic AccountingDocument21 paginiHRA & Forensic Accountingharish0% (1)

- Rapicut Carbides LimitedDocument15 paginiRapicut Carbides LimitedSafwan mansuriÎncă nu există evaluări

- Accounting For Inventories: Key Terms and Concepts To KnowDocument23 paginiAccounting For Inventories: Key Terms and Concepts To KnowMuhammad Fahad NaeemÎncă nu există evaluări

- Fabm2 DlaDocument100 paginiFabm2 DlaCathlyn San LuisÎncă nu există evaluări

- Corporate Finance I176 Xid-3384732 1Document8 paginiCorporate Finance I176 Xid-3384732 1kashualÎncă nu există evaluări

- Gopal Namkeen by MDDocument80 paginiGopal Namkeen by MDmaulesh1982100% (2)

- 9706 s09 QP 4Document8 pagini9706 s09 QP 4roukaiya_peerkhanÎncă nu există evaluări

- 4 Balance SheetDocument2 pagini4 Balance Sheetapi-299265916Încă nu există evaluări

- Accounting For Lawyers by Solicitor KatuDocument45 paginiAccounting For Lawyers by Solicitor KatuFrancisco Hagai GeorgeÎncă nu există evaluări

- Farm Management Chap 2Document42 paginiFarm Management Chap 2gedisha katola100% (1)

- Nobs Business SuccessDocument8 paginiNobs Business SuccessUpdatest newsÎncă nu există evaluări

- AKMY 6e ch02 - SMDocument31 paginiAKMY 6e ch02 - SMshoaidaresÎncă nu există evaluări

- ch01 PDFDocument2 paginich01 PDFDanish BaigÎncă nu există evaluări

- Topic 1 Tutorial QuestionsDocument7 paginiTopic 1 Tutorial QuestionsAbigailÎncă nu există evaluări

- Eli Amir - Marco Ghitti - Financial Analysis of Mergers and Acquisitions - Understanding Financial Statements and Accounting Rules With Case Studies-Springer International Publishing (2021)Document392 paginiEli Amir - Marco Ghitti - Financial Analysis of Mergers and Acquisitions - Understanding Financial Statements and Accounting Rules With Case Studies-Springer International Publishing (2021)Carolina LucínÎncă nu există evaluări

- Intermediate Accounting Volume 2 Canadian 12th Edition Kieso Test BankDocument25 paginiIntermediate Accounting Volume 2 Canadian 12th Edition Kieso Test Bankluaguelottie834100% (13)

- Paper 2 Audit and AssuranceDocument479 paginiPaper 2 Audit and AssuranceAashish AdhikariÎncă nu există evaluări

- Solutions Images Bingham 11-02-2010Document46 paginiSolutions Images Bingham 11-02-2010Nicky 'Zing' Nguyen100% (7)

- Partnership FormationDocument13 paginiPartnership FormationAllen GonzagaÎncă nu există evaluări

- 1Q 2020 PORT Nusantara+Pelabuhan+Handal+Tbk PDFDocument88 pagini1Q 2020 PORT Nusantara+Pelabuhan+Handal+Tbk PDFTuýtuýÎncă nu există evaluări

- SAP Asset Accounting OverviewDocument17 paginiSAP Asset Accounting OverviewSubbireddy ChintapalliÎncă nu există evaluări

- Sunsystems - 6.4.x Financials AdministrationDocument400 paginiSunsystems - 6.4.x Financials Administrationeverboqaileh mohÎncă nu există evaluări

- Tally QuestionDocument59 paginiTally Questionkiranmayi 2705Încă nu există evaluări

- CFI Accountingfactsheet-1499721167572 PDFDocument1 paginăCFI Accountingfactsheet-1499721167572 PDFአረጋዊ ሐይለማርያምÎncă nu există evaluări

- Standard Valuation Personal PropertyDocument19 paginiStandard Valuation Personal PropertyHarryÎncă nu există evaluări

- Financial Analysis Training ReportDocument71 paginiFinancial Analysis Training ReportSaurav PariyarÎncă nu există evaluări

- CoDocument10 paginiCoSri KanthÎncă nu există evaluări

- Solution To P4-6Document4 paginiSolution To P4-6Andrew WhitfieldÎncă nu există evaluări

- Tiob SyllabusDocument134 paginiTiob SyllabusFred Raphael Ilomo83% (6)