S-ar putea să vă placă și

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe la EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryEvaluare: 3.5 din 5 stele3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De la EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Evaluare: 4.5 din 5 stele4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDe la EverandGrit: The Power of Passion and PerseveranceEvaluare: 4 din 5 stele4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe la EverandNever Split the Difference: Negotiating As If Your Life Depended On ItEvaluare: 4.5 din 5 stele4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe la EverandThe Little Book of Hygge: Danish Secrets to Happy LivingEvaluare: 3.5 din 5 stele3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe la EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaEvaluare: 4.5 din 5 stele4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe la EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeEvaluare: 4 din 5 stele4/5 (5795)

- Her Body and Other Parties: StoriesDe la EverandHer Body and Other Parties: StoriesEvaluare: 4 din 5 stele4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe la EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreEvaluare: 4 din 5 stele4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe la EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyEvaluare: 3.5 din 5 stele3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe la EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersEvaluare: 4.5 din 5 stele4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDe la EverandShoe Dog: A Memoir by the Creator of NikeEvaluare: 4.5 din 5 stele4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe la EverandThe Emperor of All Maladies: A Biography of CancerEvaluare: 4.5 din 5 stele4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDe la EverandTeam of Rivals: The Political Genius of Abraham LincolnEvaluare: 4.5 din 5 stele4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe la EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceEvaluare: 4 din 5 stele4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe la EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureEvaluare: 4.5 din 5 stele4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe la EverandOn Fire: The (Burning) Case for a Green New DealEvaluare: 4 din 5 stele4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De la EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Evaluare: 4 din 5 stele4/5 (98)

- The Unwinding: An Inner History of the New AmericaDe la EverandThe Unwinding: An Inner History of the New AmericaEvaluare: 4 din 5 stele4/5 (45)

- 11 Deductions From Gross Income (Expenses in General, Interest Expense and Taxes)Document18 pagini11 Deductions From Gross Income (Expenses in General, Interest Expense and Taxes)Clarisse PelayoÎncă nu există evaluări

- Daniels Ib13 05Document20 paginiDaniels Ib13 05abhishekkumar2139Încă nu există evaluări

- Daniels Ib13 06Document24 paginiDaniels Ib13 06abhishekkumar2139Încă nu există evaluări

- Daniels Ib13 08Document28 paginiDaniels Ib13 08abhishekkumar2139Încă nu există evaluări

- Daniels Ib13 16Document20 paginiDaniels Ib13 16abhishekkumar2139100% (1)

- International Business Environments and Operations, 13/e Global EditionDocument15 paginiInternational Business Environments and Operations, 13/e Global Editionabhishekkumar2139Încă nu există evaluări

- Daniels Ib13 20Document18 paginiDaniels Ib13 20abhishekkumar2139Încă nu există evaluări

- International Business Environments and Operations, 13/e Global EditionDocument22 paginiInternational Business Environments and Operations, 13/e Global Editionabhishekkumar2139Încă nu există evaluări

- Project FinanceDocument3 paginiProject FinanceSonam GoyalÎncă nu există evaluări

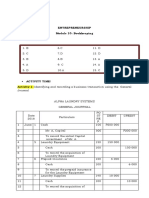

- Entrepreneurship Module 10: Bookkeeping What I KnowDocument23 paginiEntrepreneurship Module 10: Bookkeeping What I KnowDos DosÎncă nu există evaluări

- Turnover TransmittalDocument6 paginiTurnover TransmittalDarwin LasinÎncă nu există evaluări

- Guidance Note - ESOPDocument68 paginiGuidance Note - ESOPSandhya UpadhyayÎncă nu există evaluări

- Gic Housing Finance LTD.: GICHFL/SEC/2020 23 November, 2020 The BSE LTD.Document161 paginiGic Housing Finance LTD.: GICHFL/SEC/2020 23 November, 2020 The BSE LTD.gulafsha1Încă nu există evaluări

- MCQ Oppression - Mismanagement by CA Darshan Khare Sir 1 PDFDocument11 paginiMCQ Oppression - Mismanagement by CA Darshan Khare Sir 1 PDFAnand Pathak0% (1)

- Full Download Intermediate Accounting 10th Edition Spiceland Solutions ManualDocument35 paginiFull Download Intermediate Accounting 10th Edition Spiceland Solutions Manualdalikifukiauj100% (32)

- Pfm15e Im Ch11Document40 paginiPfm15e Im Ch11vdav hadhÎncă nu există evaluări

- Receivership Administration LiquidationDocument2 paginiReceivership Administration LiquidationjeblukÎncă nu există evaluări

- Jollibee Foods Corporation: Consolidated Statements of IncomeDocument9 paginiJollibee Foods Corporation: Consolidated Statements of Incomearvin cleinÎncă nu există evaluări

- ACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneDocument33 paginiACCT1A&B Reviewer Disadvantages: ABRAHAM, Daisy JaneGabriel L. CaringalÎncă nu există evaluări

- Annamalai University: Directorate of Distance EducationDocument449 paginiAnnamalai University: Directorate of Distance EducationKing AdvÎncă nu există evaluări

- Acc 1 Financial Statement Analysis (Part 2)Document27 paginiAcc 1 Financial Statement Analysis (Part 2)juthi rawnakÎncă nu există evaluări

- GoodwillDocument16 paginiGoodwillapoorva100% (1)

- Indian Companies ActDocument51 paginiIndian Companies ActvaibhavÎncă nu există evaluări

- Sem 4 Bcom Law NotesDocument12 paginiSem 4 Bcom Law NotestheunknowntimepassÎncă nu există evaluări

- Quiz Financial StatementsDocument7 paginiQuiz Financial StatementsEzer Cruz BarrantesÎncă nu există evaluări

- Industry Analysis: What Is The Objectives of Performing Industry Analysis?Document25 paginiIndustry Analysis: What Is The Objectives of Performing Industry Analysis?UDIT GUPTAÎncă nu există evaluări

- PTPPDocument155 paginiPTPPnaufalmuhammadÎncă nu există evaluări

- Initial Public Offerings: Updated StatisticsDocument75 paginiInitial Public Offerings: Updated StatisticsprasannakumarÎncă nu există evaluări

- Topic 3 - Revision Questions SolutionsDocument18 paginiTopic 3 - Revision Questions SolutionsPhan Thi Tuyet Nhung100% (1)

- DeutchbankDocument436 paginiDeutchbankCebotar AndreiÎncă nu există evaluări

- Aviva 2012 Annual ReportDocument280 paginiAviva 2012 Annual ReportAviva GroupÎncă nu există evaluări

- Accounting I December 2020Document5 paginiAccounting I December 2020faraz hassanÎncă nu există evaluări

- Ratio Analysis of Kohinoor ChemicalDocument13 paginiRatio Analysis of Kohinoor ChemicalShouvoRahamanÎncă nu există evaluări

- Business - Associations - by - Ssozi RajjabuDocument82 paginiBusiness - Associations - by - Ssozi RajjabuNAYIGA DEMITÎncă nu există evaluări

- dt7 PDFDocument215 paginidt7 PDFAnkitaÎncă nu există evaluări

- Exercise 1 - Practice For The Final: ABC Asset (Unlevered) Beta 0.70Document10 paginiExercise 1 - Practice For The Final: ABC Asset (Unlevered) Beta 0.70Mariale RamosÎncă nu există evaluări

- Audit of Cash and Financial InstrumentsDocument4 paginiAudit of Cash and Financial Instrumentsmrs leeÎncă nu există evaluări