S-ar putea să vă placă și

- PPH Pasal 26 EnglishDocument4 paginiPPH Pasal 26 Englishmarlina elisabethÎncă nu există evaluări

- Mock E Exam Pap ERDocument19 paginiMock E Exam Pap ERtim_rattanaÎncă nu există evaluări

- Practical Application of Taxation On CorporationsDocument5 paginiPractical Application of Taxation On CorporationsClaire BarbaÎncă nu există evaluări

- RR 12-2007 PDFDocument7 paginiRR 12-2007 PDFnaldsdomingoÎncă nu există evaluări

- WTAXESDocument31 paginiWTAXESlance757Încă nu există evaluări

- VAT Other Aspects - January 2024Document5 paginiVAT Other Aspects - January 2024Charisma CharlesÎncă nu există evaluări

- Cfab - Acc - LN - Chapter 9Document9 paginiCfab - Acc - LN - Chapter 9Huy NguyenÎncă nu există evaluări

- White Paper: Ministry of Finance, Trade and Economic PlanningDocument16 paginiWhite Paper: Ministry of Finance, Trade and Economic PlanningBonar StepanusÎncă nu există evaluări

- LESSON 13 Tax PAYMENT AND PROCEDURES and ASSESSEMTDocument14 paginiLESSON 13 Tax PAYMENT AND PROCEDURES and ASSESSEMTOctavius MuyungiÎncă nu există evaluări

- Topic 1: Accounting For Income TaxesDocument13 paginiTopic 1: Accounting For Income TaxesPillos Jr., ElimarÎncă nu există evaluări

- Taxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mDocument32 paginiTaxable Income: 20% 10000 200000/2 200000000 PIT 200000000 5% 10mnga vuÎncă nu există evaluări

- Interim Financial ReportingDocument17 paginiInterim Financial ReportingAlexa LeeÎncă nu există evaluări

- TDS & TCSDocument107 paginiTDS & TCSSANDEEP CHAUREÎncă nu există evaluări

- M7 - P1 Individual Income Taxation - Students'Document66 paginiM7 - P1 Individual Income Taxation - Students'micaella pasionÎncă nu există evaluări

- Additions To TaxDocument22 paginiAdditions To Taxstannis69420Încă nu există evaluări

- 2.0 Estimate Tax Payable - CompanyDocument3 pagini2.0 Estimate Tax Payable - CompanycarazamanÎncă nu există evaluări

- Taxation Mid TermDocument6 paginiTaxation Mid TermMuhammad AlfarrabieÎncă nu există evaluări

- TTM 12 - Income Tax Article 24 and 25Document18 paginiTTM 12 - Income Tax Article 24 and 25Ramdonidoni doniÎncă nu există evaluări

- Provisional Taxes 2023handoutDocument43 paginiProvisional Taxes 2023handoutv8ysqzd9pbÎncă nu există evaluări

- Tax Sample ComputationDocument9 paginiTax Sample ComputationErykaÎncă nu există evaluări

- Quarterly Income A5 EngDocument4 paginiQuarterly Income A5 EngKasendereÎncă nu există evaluări

- Indonesian Tax Treatment For Foreign Drilling Companies FDCDocument4 paginiIndonesian Tax Treatment For Foreign Drilling Companies FDCJoko ArifiantoÎncă nu există evaluări

- Iup 4 (Midterm)Document9 paginiIup 4 (Midterm)Wilkinson MardikaÎncă nu există evaluări

- Learn XtraDocument12 paginiLearn XtraKent WhiteÎncă nu există evaluări

- Tax Sample ComputationDocument10 paginiTax Sample ComputationEryka Jo MonatoÎncă nu există evaluări

- Tax Accounting Set ADocument4 paginiTax Accounting Set AGopti EmmanuelÎncă nu există evaluări

- MG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesDocument27 paginiMG 3027 TAXATION - Week 18 Payment of Income Tax, Interest and PenaltiesSyed SafdarÎncă nu există evaluări

- Annual Income Information Form For General Professional PartnershipsDocument2 paginiAnnual Income Information Form For General Professional PartnershipsAlvin Dela CruzÎncă nu există evaluări

- BIR ComputationsDocument10 paginiBIR Computationsbull jackÎncă nu există evaluări

- Accounting For Income TaxDocument4 paginiAccounting For Income TaxRed YuÎncă nu există evaluări

- Case Study - Chapter 1 2 3 4 - 2Document5 paginiCase Study - Chapter 1 2 3 4 - 2Lê Ngọc Vân NhiÎncă nu există evaluări

- Accounting Methods and Installment ReportingDocument40 paginiAccounting Methods and Installment ReportingKatherine EderosasÎncă nu există evaluări

- OSD and NOLCODocument2 paginiOSD and NOLCOAccounting FilesÎncă nu există evaluări

- Chapter 12 v2Document18 paginiChapter 12 v2Sheilamae Sernadilla GregorioÎncă nu există evaluări

- How To Compute Individual Income TaxDocument4 paginiHow To Compute Individual Income TaxberinguelajunahÎncă nu există evaluări

- 5.09 Analysis of Income TaxesDocument10 pagini5.09 Analysis of Income TaxesClaptrapjackÎncă nu există evaluări

- All Level Two Coc QuestionsDocument15 paginiAll Level Two Coc Questionsabelu habite neriÎncă nu există evaluări

- Taxation On IndividualsDocument10 paginiTaxation On IndividualsHERNANDO REYESÎncă nu există evaluări

- CORPORATE INCOME TAX (Answer Key)Document5 paginiCORPORATE INCOME TAX (Answer Key)Rujean Salar AltejarÎncă nu există evaluări

- Enc Encoded A0nNFhan9Jl78cAySc2AolaE2Yye0 HIgHbnr6loXue2yScW3KSbxZwM1pJvw6EDocument8 paginiEnc Encoded A0nNFhan9Jl78cAySc2AolaE2Yye0 HIgHbnr6loXue2yScW3KSbxZwM1pJvw6Eharwoko yokoÎncă nu există evaluări

- Reales Tax Rev Computation ExerciseDocument4 paginiReales Tax Rev Computation ExerciseJethroret RealesÎncă nu există evaluări

- Sec. 121Document1 paginăSec. 121tony tony chopperÎncă nu există evaluări

- Module 6 - Income Tax On Corporations - Part 2Document5 paginiModule 6 - Income Tax On Corporations - Part 2Never Letting GoÎncă nu există evaluări

- Taxation AssignmentDocument9 paginiTaxation AssignmentDhairyaÎncă nu există evaluări

- Adjustments (Part 2) : Subject-Descriptive Title Subject - CodeDocument11 paginiAdjustments (Part 2) : Subject-Descriptive Title Subject - CodeRose LaureanoÎncă nu există evaluări

- LMT School of Management, Thapar University Masters of Business AdministrationDocument9 paginiLMT School of Management, Thapar University Masters of Business Administrationtechnical sÎncă nu există evaluări

- BIR ComputationsDocument10 paginiBIR Computationsbull jack100% (1)

- Interim Financial Reporting-AssignmentDocument5 paginiInterim Financial Reporting-AssignmentLourdrandal AbellaÎncă nu există evaluări

- Quizzz Intac 3Document10 paginiQuizzz Intac 3lana del reyÎncă nu există evaluări

- Tax XXXXDocument60 paginiTax XXXXGerald Bowe ResuelloÎncă nu există evaluări

- Front - Maintain Training FacilitiesDocument5 paginiFront - Maintain Training FacilitiesRechie Gimang AlferezÎncă nu există evaluări

- CHAPTER 3 - Transfer and Business TaxDocument6 paginiCHAPTER 3 - Transfer and Business TaxKatKat Olarte0% (1)

- M6 - Deductions P2 Students'Document53 paginiM6 - Deductions P2 Students'micaella pasionÎncă nu există evaluări

- Tutorial 3 (Q)Document4 paginiTutorial 3 (Q)szh saÎncă nu există evaluări

- International TaxationDocument8 paginiInternational TaxationkinslinÎncă nu există evaluări

- Computation of Income TaxDocument10 paginiComputation of Income TaxPageduesca RouelÎncă nu există evaluări

- TaxDocument6 paginiTaxKhánh LinhÎncă nu există evaluări

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeDe la Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeEvaluare: 1 din 5 stele1/5 (1)

- Table of ContentDocument1 paginăTable of ContenttantriwidyasÎncă nu există evaluări

- Bab 1Document4 paginiBab 1tantriwidyasÎncă nu există evaluări

- Presta ShopDocument1 paginăPresta ShoptantriwidyasÎncă nu există evaluări

- 2.3 External Environment: 1. Natural Environment Regulation and Permi TDocument3 pagini2.3 External Environment: 1. Natural Environment Regulation and Permi TtantriwidyasÎncă nu există evaluări

- Chapter 12 SolutionsDocument9 paginiChapter 12 SolutionsKIKIKIKIREALLY4399Încă nu există evaluări

- Table of ContentDocument1 paginăTable of ContenttantriwidyasÎncă nu există evaluări

- Total Asset Turnover Ratio Measures How All Assets Owned by The Company Are Operated in Support of The CompanyDocument5 paginiTotal Asset Turnover Ratio Measures How All Assets Owned by The Company Are Operated in Support of The CompanytantriwidyasÎncă nu există evaluări

- Pos IndonesiaDocument42 paginiPos IndonesiatantriwidyasÎncă nu există evaluări

- Strategic Manager PosDocument7 paginiStrategic Manager PostantriwidyasÎncă nu există evaluări

- StrategicDocument2 paginiStrategictantriwidyasÎncă nu există evaluări

- 87031Document40 pagini87031tantriwidyasÎncă nu există evaluări

- Internal Environment 4.1 Corporate StructureDocument12 paginiInternal Environment 4.1 Corporate StructuretantriwidyasÎncă nu există evaluări

- Mahm8echapter09 140901033155 Phpapp02 - 2Document27 paginiMahm8echapter09 140901033155 Phpapp02 - 2tantriwidyasÎncă nu există evaluări

- Name: Tantri Widya S NIM: 125030207111100Document1 paginăName: Tantri Widya S NIM: 125030207111100tantriwidyasÎncă nu există evaluări

- Finance PT KAIDocument6 paginiFinance PT KAItantriwidyasÎncă nu există evaluări

- Strategy For Internationalisation: A. Harmonisation With The International Political SystemDocument1 paginăStrategy For Internationalisation: A. Harmonisation With The International Political SystemtantriwidyasÎncă nu există evaluări

- Natural EnvironmentDocument17 paginiNatural EnvironmenttantriwidyasÎncă nu există evaluări

- Task EnvironmentDocument5 paginiTask EnvironmenttantriwidyasÎncă nu există evaluări

- Evaluation and ControldddDocument15 paginiEvaluation and ControldddtantriwidyasÎncă nu există evaluări

- Task Environment RevisiDocument5 paginiTask Environment RevisitantriwidyasÎncă nu există evaluări

- Investment ProcessDocument2 paginiInvestment ProcesstantriwidyasÎncă nu există evaluări

- Bab2 Tantri&VikaDocument8 paginiBab2 Tantri&VikatantriwidyasÎncă nu există evaluări

- Uts MenisDocument1 paginăUts MenistantriwidyasÎncă nu există evaluări

- 4 (Corporate Structure, Culture, Resource)Document17 pagini4 (Corporate Structure, Culture, Resource)tantriwidyasÎncă nu există evaluări

- StaDocument21 paginiStadinesh_haiÎncă nu există evaluări

- AccDocument12 paginiAcctantriwidyasÎncă nu există evaluări

- Preferences and ContentDocument2 paginiPreferences and ContenttantriwidyasÎncă nu există evaluări

- Pak Hadak Bab 2Document1 paginăPak Hadak Bab 2tantriwidyasÎncă nu există evaluări

- Resume of Legal and Tax IssuesDocument4 paginiResume of Legal and Tax IssuestantriwidyasÎncă nu există evaluări

- Accounting For Receivables PDFDocument23 paginiAccounting For Receivables PDFjess calderonÎncă nu există evaluări

- Global Strategic Planning: ObjectivesDocument4 paginiGlobal Strategic Planning: ObjectivesHitesh GevariyaÎncă nu există evaluări

- Company SecretaryDocument22 paginiCompany SecretaryNikhil DeshpandeÎncă nu există evaluări

- 2009 BIR-RMC ContentsDocument56 pagini2009 BIR-RMC ContentsMary Grace Caguioa AgasÎncă nu există evaluări

- Chapter - Money Creation & Framwork of Monetary Policy1Document6 paginiChapter - Money Creation & Framwork of Monetary Policy1Nahidul Islam IUÎncă nu există evaluări

- Contemporary Issues of GlobalizationDocument22 paginiContemporary Issues of GlobalizationAyman MotenÎncă nu există evaluări

- 33611B SUV & Light Truck Manufacturing in The US Industry ReportDocument38 pagini33611B SUV & Light Truck Manufacturing in The US Industry ReportSubhash BabuÎncă nu există evaluări

- Brochure (Eng) - 2021 Oda KoreaDocument9 paginiBrochure (Eng) - 2021 Oda Koreasunjung kimÎncă nu există evaluări

- Quiz 7Document3 paginiQuiz 7朱潇妤Încă nu există evaluări

- Suarez, Francis - FORM 1 - 2009 PDFDocument3 paginiSuarez, Francis - FORM 1 - 2009 PDFal_crespoÎncă nu există evaluări

- Problems and Prospects of Organic Horticultural Farming in BangladeshDocument10 paginiProblems and Prospects of Organic Horticultural Farming in BangladeshMahamud Hasan PrinceÎncă nu există evaluări

- Chapter 2.0Document22 paginiChapter 2.0MOHAMAD ASHRAF BIN MOHAMAD TAJARI MoeÎncă nu există evaluări

- VAT Registration CertificateDocument1 paginăVAT Registration Certificatelucas.saleixo88Încă nu există evaluări

- Process Planning and Cost EstimationDocument13 paginiProcess Planning and Cost EstimationsanthoshjoysÎncă nu există evaluări

- mt4 IndicatorDocument4 paginimt4 IndicatorNikhil Pillay100% (1)

- RSAW Review of The Year 2021Document14 paginiRSAW Review of The Year 2021Prasamsa PÎncă nu există evaluări

- Real Estate Player in BangaloreDocument20 paginiReal Estate Player in BangaloreAnkit GoelÎncă nu există evaluări

- MGT AC - Prob-NewDocument276 paginiMGT AC - Prob-Newrandom122Încă nu există evaluări

- KFC Offer T&C: SL - No Outlet Name CityDocument16 paginiKFC Offer T&C: SL - No Outlet Name Cityanita rajenÎncă nu există evaluări

- ID Pembentukan Portofolio Optimal Dengan MoDocument9 paginiID Pembentukan Portofolio Optimal Dengan MoIlham AlfianÎncă nu există evaluări

- Law University SynopsisDocument3 paginiLaw University Synopsistinabhuvan50% (2)

- September October LD Debate Kritik (Neg)Document5 paginiSeptember October LD Debate Kritik (Neg)RhuiedianÎncă nu există evaluări

- ItcDocument10 paginiItcPrabhav ChauhanÎncă nu există evaluări

- Kultura NG TsinaDocument5 paginiKultura NG TsinaJeaniel amponÎncă nu există evaluări

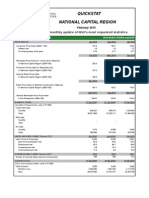

- Quickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDocument3 paginiQuickstat National Capital Region: A Monthly Update of NSO's Most Requested StatisticsDaniel John Cañares LegaspiÎncă nu există evaluări

- How To Start A Travel and Tour BusinessDocument3 paginiHow To Start A Travel and Tour BusinessGrace LeonardoÎncă nu există evaluări

- Value ChainDocument31 paginiValue ChainNodiey YanaÎncă nu există evaluări

- Social Integration Approaches and Issues, UNRISD Publication (1994)Document16 paginiSocial Integration Approaches and Issues, UNRISD Publication (1994)United Nations Research Institute for Social DevelopmentÎncă nu există evaluări

- Leizel C. AmidoDocument2 paginiLeizel C. AmidoAmido Capagngan LeizelÎncă nu există evaluări

- TC2014 15 NirdDocument124 paginiTC2014 15 Nirdssvs1234Încă nu există evaluări