S-ar putea să vă placă și

- Secured transaction Complete Self-Assessment GuideDe la EverandSecured transaction Complete Self-Assessment GuideÎncă nu există evaluări

- Get a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.De la EverandGet a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.Încă nu există evaluări

- Copyright Law Complete Hyperlinked: Hyperlinked, #6De la EverandCopyright Law Complete Hyperlinked: Hyperlinked, #6Încă nu există evaluări

- Indian Contract Act 1872Document79 paginiIndian Contract Act 1872Ayush ThakkarÎncă nu există evaluări

- Negotiable Instruments ACT, 1881: Legal Aspects of BusinessDocument25 paginiNegotiable Instruments ACT, 1881: Legal Aspects of BusinessVipul BatraÎncă nu există evaluări

- Negotiable InstrumentsDocument9 paginiNegotiable InstrumentsAndrolf CaparasÎncă nu există evaluări

- Bankers Lien-Banking LawDocument14 paginiBankers Lien-Banking LawAarif Mohammad BilgramiÎncă nu există evaluări

- BANK ACT 1864 (Original) Common-Law RemedyDocument4 paginiBANK ACT 1864 (Original) Common-Law Remedyin1or100% (1)

- Earning Six Figures in Corporate America Without a DegreeDe la EverandEarning Six Figures in Corporate America Without a DegreeÎncă nu există evaluări

- The Registration Act 1908Document26 paginiThe Registration Act 1908Asif Masood RajaÎncă nu există evaluări

- Dishonour of Negotiable InstrumentsDocument35 paginiDishonour of Negotiable InstrumentsjpesÎncă nu există evaluări

- Money Facts: 169 Questions & Answers on MoneyDe la EverandMoney Facts: 169 Questions & Answers on MoneyÎncă nu există evaluări

- Debt's Dominion: A History of Bankruptcy Law in AmericaDe la EverandDebt's Dominion: A History of Bankruptcy Law in AmericaEvaluare: 3.5 din 5 stele3.5/5 (2)

- Bonds & DebentureDocument6 paginiBonds & DebentureHemant GaikwadÎncă nu există evaluări

- Unit 2 Sherman Antitrust Act of 1890Document15 paginiUnit 2 Sherman Antitrust Act of 1890Prachi Tripathi100% (1)

- The UCC and The Assignment ProcessDocument5 paginiThe UCC and The Assignment ProcessJohnGarzaÎncă nu există evaluări

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementDe la EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementÎncă nu există evaluări

- Out PDFDocument38 paginiOut PDFfelixmuyoveÎncă nu există evaluări

- The Industrial Organization and Regulation of the Securities IndustryDe la EverandThe Industrial Organization and Regulation of the Securities IndustryÎncă nu există evaluări

- Banking Law BookDocument179 paginiBanking Law Bookbhupendra barhatÎncă nu există evaluări

- The Richest Man in Babylon, 2nd Edition Gold Ahead with Financial Study Guide: 2nd Edition with Financial Study GuideDe la EverandThe Richest Man in Babylon, 2nd Edition Gold Ahead with Financial Study Guide: 2nd Edition with Financial Study GuideÎncă nu există evaluări

- Chapter 05 Negotiable Instruments Act 1881 1229869805849562 1Document11 paginiChapter 05 Negotiable Instruments Act 1881 1229869805849562 1अरुण शर्माÎncă nu există evaluări

- Bills of ExchangeDocument31 paginiBills of ExchangeViransh Coaching ClassesÎncă nu există evaluări

- Bill of ExchangeDocument9 paginiBill of ExchangeMariyam MalsaÎncă nu există evaluări

- Law of ContractsDocument15 paginiLaw of Contractskumarshashi004Încă nu există evaluări

- Chapter 3. Banker Customer RelationshipDocument38 paginiChapter 3. Banker Customer RelationshippadminiÎncă nu există evaluări

- Promissory NoteDocument10 paginiPromissory NoteIsh ChavanÎncă nu există evaluări

- Promissory NoteDocument4 paginiPromissory Noteapi-437528557Încă nu există evaluări

- Types of Commercial PaperDocument3 paginiTypes of Commercial PaperAjay SharmaÎncă nu există evaluări

- D-Negotiable Instrument ActDocument37 paginiD-Negotiable Instrument Actharsh100% (1)

- Bills of ExchangeDocument2 paginiBills of ExchangeSachin TiwariÎncă nu există evaluări

- Discharge of ContractDocument16 paginiDischarge of ContractBarun GuptaÎncă nu există evaluări

- Promissory NoteDocument20 paginiPromissory NoteAswaraj PandeyÎncă nu există evaluări

- Banker and CustomerDocument4 paginiBanker and CustomerLloyd J. PereiraÎncă nu există evaluări

- Doctrine of SuborgrationDocument9 paginiDoctrine of Suborgrationsadhvi singh100% (1)

- Am. Jur. 2d Cumulative Summary of Contents (2021)Document11 paginiAm. Jur. 2d Cumulative Summary of Contents (2021)MinisterÎncă nu există evaluări

- Affidavit of Thomas Adams For US Bank V CongressDocument9 paginiAffidavit of Thomas Adams For US Bank V CongressJohn StupÎncă nu există evaluări

- CFPB - TILA RESPA Integrated Disclosure - Frequently Asked QuestionsDocument27 paginiCFPB - TILA RESPA Integrated Disclosure - Frequently Asked Questionsclash clansÎncă nu există evaluări

- Rules On IndorsementDocument3 paginiRules On IndorsementBle Garay100% (1)

- The Negotiable Instruments Act 1881Document16 paginiThe Negotiable Instruments Act 1881vivekÎncă nu există evaluări

- Letters of Credit Q and ADocument5 paginiLetters of Credit Q and ARose Ann VeloriaÎncă nu există evaluări

- How To Complete Certified DocumentsDocument1 paginăHow To Complete Certified DocumentsDeannaÎncă nu există evaluări

- Bill of Lading (B/L) : What Is Bill of Exchange and State Its Essentials ?Document4 paginiBill of Lading (B/L) : What Is Bill of Exchange and State Its Essentials ?Dhananjay KumarÎncă nu există evaluări

- The Negotiable Instruments Act 1881Document91 paginiThe Negotiable Instruments Act 1881jerijose1987Încă nu există evaluări

- Bankers AcceptancesDocument36 paginiBankers AcceptancesAlexhCreditorÎncă nu există evaluări

- Discharge of ContractDocument10 paginiDischarge of ContractAkash SharmaÎncă nu există evaluări

- Negotiable Instruments Act, 1881Document24 paginiNegotiable Instruments Act, 1881vikramjeet_22100% (1)

- Non-Citizen Guidance 063011Document62 paginiNon-Citizen Guidance 063011bwidjaja73Încă nu există evaluări

- Negotiable Instruments Act of IndiaDocument164 paginiNegotiable Instruments Act of IndiaShome BhattacharjeeÎncă nu există evaluări

- BY: 37 MBA 09 43 MBA 09: Venika Saini Anuj GuptaDocument31 paginiBY: 37 MBA 09 43 MBA 09: Venika Saini Anuj GuptaaditibakshiÎncă nu există evaluări

- The Credit River Money OpinionDocument9 paginiThe Credit River Money OpinionJason Henry0% (2)

- Institute of Engineering and Technology, Alwar, Rajasthan: Wireless Keypad Controlled RobotDocument44 paginiInstitute of Engineering and Technology, Alwar, Rajasthan: Wireless Keypad Controlled RobotTwinkle SinghÎncă nu există evaluări

- Credit Report Prism CementDocument14 paginiCredit Report Prism CementTwinkle SinghÎncă nu există evaluări

- PT - Igate Patni DealDocument6 paginiPT - Igate Patni DealTwinkle SinghÎncă nu există evaluări

- UK Stewardship Code 2012Document22 paginiUK Stewardship Code 2012Twinkle SinghÎncă nu există evaluări

- UK Stewardship Code 2012Document22 paginiUK Stewardship Code 2012Twinkle SinghÎncă nu există evaluări

- AgencyDocument21 paginiAgencyTwinkle SinghÎncă nu există evaluări

- Legal FinalDocument24 paginiLegal FinalTwinkle SinghÎncă nu există evaluări

- OB AssignmentDocument3 paginiOB AssignmentTwinkle SinghÎncă nu există evaluări

- Research MethodologyDocument25 paginiResearch MethodologyTwinkle SinghÎncă nu există evaluări

- Bank FraudDocument8 paginiBank FraudHuman Being50% (2)

- AIS Chapter 5Document12 paginiAIS Chapter 5Krishtelle Anndrhei SalazarÎncă nu există evaluări

- T3TLC - Letters of CreditDocument181 paginiT3TLC - Letters of CreditZia Uz Zahideen50% (2)

- EOS Accounts and Budget Support Level IIIDocument93 paginiEOS Accounts and Budget Support Level IIIKass habtemariam0% (1)

- Notice: Now You Can Pay Your Bill Online. For Online Payment Please Visit HTTPS://GMDWSB - Assam.gov - in orDocument1 paginăNotice: Now You Can Pay Your Bill Online. For Online Payment Please Visit HTTPS://GMDWSB - Assam.gov - in orGaryÎncă nu există evaluări

- Handbook On Accounting Procedures For RD InstitutionsDocument131 paginiHandbook On Accounting Procedures For RD InstitutionsLaldinliana VarteÎncă nu există evaluări

- RBI SBI Demand Draft Exchange RatesDocument11 paginiRBI SBI Demand Draft Exchange RatesJithin VijayanÎncă nu există evaluări

- ACE Nifty Futures Trading System User GuideDocument47 paginiACE Nifty Futures Trading System User Guideranith2787Încă nu există evaluări

- Tratado XXXDocument2 paginiTratado XXXELI AlavaradoÎncă nu există evaluări

- mPassBook XXXXXXXXXXX768Document2 paginimPassBook XXXXXXXXXXX768gurpreetsingh777000777Încă nu există evaluări

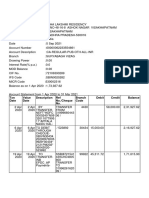

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument28 paginiTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancesv netÎncă nu există evaluări

- Bank Reconciliation StatementDocument10 paginiBank Reconciliation StatementmuniÎncă nu există evaluări

- CANON 1 - Moreno vs. AranetaDocument1 paginăCANON 1 - Moreno vs. AranetanaaguilarÎncă nu există evaluări

- CBD Business Banking GeneraltermsDocument43 paginiCBD Business Banking GeneraltermsSanthosh KumarÎncă nu există evaluări

- AL Habib Mahana Munafa Key FactDocument2 paginiAL Habib Mahana Munafa Key FactAmir Mehmood AbbasiÎncă nu există evaluări

- Revisionary Test Paper - Intermediate - Syllabus 2012 - Dec2013Document40 paginiRevisionary Test Paper - Intermediate - Syllabus 2012 - Dec2013sumit4up6rÎncă nu există evaluări

- Selective PagesDocument13 paginiSelective PagesQuality Assurance Manager0% (2)

- General Awareness Questions PDFDocument10 paginiGeneral Awareness Questions PDFRamu KÎncă nu există evaluări

- MCB Internship ReportDocument44 paginiMCB Internship Reportbbaahmad89100% (1)

- Special Penal Laws 2014Document16 paginiSpecial Penal Laws 2014Martin Martel50% (2)

- New Rules of Measurement 2 DecDocument2 paginiNew Rules of Measurement 2 DecKrish DoodnauthÎncă nu există evaluări

- BSD Frequently Asked Questions No 2 of 2020 eDocument17 paginiBSD Frequently Asked Questions No 2 of 2020 eAda DeranaÎncă nu există evaluări

- GPLocum BDocument2 paginiGPLocum BPatrickÎncă nu există evaluări

- Timeliness of Filing BP 22 CasesDocument2 paginiTimeliness of Filing BP 22 CasesConcepcion CejanoÎncă nu există evaluări

- Jodhpur Telecom District: Account SummaryDocument3 paginiJodhpur Telecom District: Account Summaryshantanu chaudharyÎncă nu există evaluări

- Bank Statement KotakDocument4 paginiBank Statement KotakRamPrasadÎncă nu există evaluări

- Capstone Project: On Daily Cash Flow ManagementDocument11 paginiCapstone Project: On Daily Cash Flow Managementloneheart007Încă nu există evaluări

- Cash and Cash EqDocument18 paginiCash and Cash EqElaine YapÎncă nu există evaluări

- KFS - Doc - Mon Sep 05 2022 19 - 03 - 51 GMT+0400 (Gulf Standard Time)Document3 paginiKFS - Doc - Mon Sep 05 2022 19 - 03 - 51 GMT+0400 (Gulf Standard Time)Abdul QadirÎncă nu există evaluări

- Receipts & Payments Rules, 1983Document37 paginiReceipts & Payments Rules, 1983gsiÎncă nu există evaluări